Videos

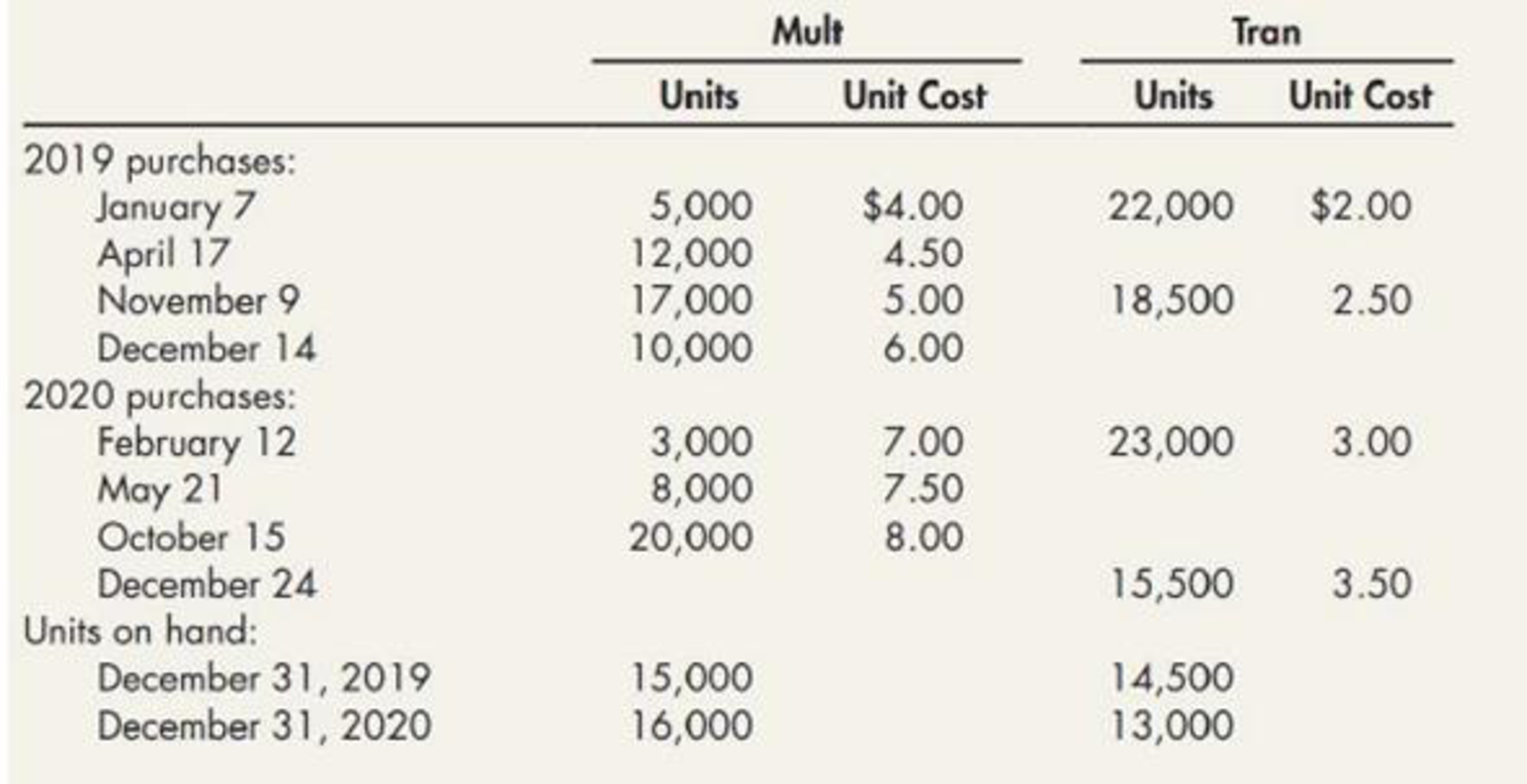

Kraft Manufacturing Company manufactures two products: Mult and Tran. At December 31, 2019, Kraft used the FIFO inventory method. Effective January 1, 2020, Kraft changed to the LIFO inventory method. The cumulative effect of this change is not determinable, and, as a result, the ending inventory of 2019, for which the FIFO method was used, is also the beginning inventory for 2020 for the LIFO method. Any layers added during 2020 should be costed by reference to the first acquisitions of 2020, and any layers liquidated during 2020 should be considered a permanent liquidation.

The following information was available from Kraft’s inventory records for the two most recent years:

Required:

Compute the effect on income before income taxes for the year ended December 31, 2020, resulting from the change from the FIFO to the LIFO inventory method.

Trending nowThis is a popular solution!

Chapter 22 Solutions

Intermediate Accounting: Reporting And Analysis

- Moore Company uses the LIFO cost flow assumption and carries Product A in inventory on December 31, 2019, at its unit cost of 9.50. Because of a sharp decline in demand for the product, the selling price was reduced to 10.00 per unit. Moores normal profit margin on Product A is 2.00, disposal costs are 1.00 per unit, and the replacement cost is 6.50. Under the lower of cost or market rule, Moores December 31, 2019, inventory of Product A should be valued at a unit cost of: a. 6.50 b. 9.00 c. 7.00 d. 9.50arrow_forwardSchmidt Company began operations on January 1, 2018, and used the LIFO inventory method for both financial reporting and income taxes. However, at the beginning of 2020, Schmidt decided to switch to the average cost inventory method for financial and income tax reporting. It had previously reported the following financial statement information for 2019: An analysis of the accounting records discloses the following cost of goods sold under the LIFO and average cost inventory methods: There are no indirect effects of the change in inventory method. Revenues for 2020 total 130,000; operating expenses for 2020 total 30,000. Schmidt is subject to a 21% income tax rate in all years; it pays all income taxes payable in the next quarter. Assume that any deferred tax liability was paid in the subsequent year. Schmidt had 10,000 shares of common stock outstanding during all years; it paid dividends of 1 per share in 2020. At the end of 2020, Schmidt had cash of 15,600, inventory of 34,000, other assets of 76,000, income taxes payable of 4,200, and accounts payable of 3,000. It desires to show financial statements for the current year and previous year in its 2020 annual report. Required: 1. Prepare the journal entry to reflect the change in method at the beginning of 2020. Show supporting calculations. 2. Prepare the 2020 financial statements. Notes to the financial statements are not necessary. Show supporting calculations.arrow_forwardKoopman Company began operations on January 1, 2018, and uses they FIFO inventory method for financial reporting and the average cost inventory method for income taxes. At the beginning of 2020, Koopman decided to switch to the average cost inventory method for financial reporting. It had previously reported the following financial statement information for 2019: An analysis of the accounting records discloses the following cost of goods sold under the FIFO and average cost inventory methods: There are no indirect effects of the change in inventory method. Revenues for 2020 total 130,000; operating expenses for 2020 total 30,000. Koopman is subject to a 21% income tax rate in all years; it pays the income taxes payable of a current year in the first quarter of the next year. Koopman had 10,000 shares of common stock outstanding during all years; it paid dividends of 1 per share in 2020. At the end of 2020, Koopman had cash of 10,000, inventory of 24,000, other assets of 70,800, accounts payable of 4,500, and income taxes payable of 6,000. It desires to show financial statements for the current year and previous year in its 2020 annual report. Required: 1. Prepare the journal entry to reflect the change in methods at the beginning of 2020. Show supporting calculations. 2. Prepare the 2020 financial statements. Notes to the financial statements are not necessary. Show supporting calculations.arrow_forward

- Refer to the information provided in RE8-4. If Paul Corporations inventory at January 1, 2019, had a cost and net realizable value of 300,000, prepare the journal entry to record the reductions to NRV for Paul Corporation assuming that Paul uses a periodic inventory system and the allowance method. Paul Corporation uses FIFO and reports the following inventory information: Assuming Paul uses a perpetual inventory system and the direct method, prepare the journal entry to record the write-down of inventory.arrow_forwardTelamark Company uses the moving weighted average method for Inventory costing. Required: The following Incomplete inventory sheet regarding Product W506 is avallable for the month of March 2020. Complete the Inventory sheet. (Use the value of the ending Inventory as your bese number and adjust the COGS $ amount to the requlred amount to make the Total Goods Avallable for Sale to the total of the Velue of the ending Inventory and the COGS total. Negative value should be Indicated with minus sign. Round your Intermediate and final answers to 2 decimal places.) Purchases/Transportation-In/ (PurchaseReturns/Discounts) Cost of Goods Sold/(Returns to Inventory) Balance in Inventory Units Avg Cost/Unit Date Units Cost/Unit Total $ Units Cost/Unit Total $ Total $ Mar. 1 Brought Forward 60 94.00 5,640.00 2 35 98.00 3 22 4 (2) 7 65 17 40 97.00 28 43 Totals Goods Available for Sale Goods Sold Ending Inventoryarrow_forwardThe Opal Company was incorporated and began operations on January 1, 2019. Opal used the weighted-average method for costing inventories. Effective January 1, 2020, Opal changed to FIFO for costing inventories and can justify the change. Information related to 2019 and 2020 inventory cost and net income is presented below: 2019 2020 Ending inventory, using: Weighted-average $650,000 $620,000 FIFO 680,000 630,000 Net income 700,000 750,000 (using average) (using FIFO) Opal's income tax rate is 30% for both 2019 and 2020. Required:Calculate the amount of the cumulative effect of the change on beginning retained earnings on January 1, 2020, that would appear on Opal's statement of retained earnings for the year ended December 31, 2020.arrow_forward

- Goddard Company has used the FIFO method of inventory valuation since it began operations in 2018. Goddard decided to change to the average cost method for determining inventory costs at the beginning of 2021. The following schedule shows year-end inventory balances under the FIFO and average cost methods: Year FIFO Average Cost 2018 $45,100 2019 78,300 2020 83,400 $54,200 71,100 78,300 Required: 1. Ignoring income taxes, prepare the 2021 journal entry to adjust the accounts to reflect the average cost method. 2. How much higher or lower would cost of goods sold be in the 2020 revised income statement? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Ignoring income taxes, prepare the 2021 journal entry to adjust the accounts to reflect the average cost method. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) View transaction list Journal entry worksheet Record the adjustment…arrow_forwardWildhorse Company began operations on January 1, 2020, and uses the FIFO method in costing its raw material inventory. Management is contemplating a change to the LIFO method and is interested in determining what effect such a change will have on net income. Accordingly, the following information has been developed: Final Inventory 2020 2021 FIFO $580000 $ 672000 LIFO 550000 656000 Net Income (computed under the FIFO method) 1080000 1310000 The company deems it impracticable to apply the retrospective approach. Based on the above information, a change to the LIFO method in 2021 would result in net income for 2021 of $1294000. $1280000. $1080000. $1310000.arrow_forwardWebster Products, Inc., adopted the dollar-value LIFO method of determining inventory costs for financial and income tax reporting on January 1, 2021. Webster continues to use the FIFO method for internal decision-making purposes. Webster's FIFO inventories at December 31, 2021, 2022, and 2023, were $300.000, $412.500, and $585,000, respectively. Internally generated cost indexes are used to convert FIFO inventory amounts to dollar-value LIFO amounts. Webster estimated these indexes as follows: 2021 2022 2823 1.00 1.25 1.50 Required: 1. Determine Webster's dollar-value LIFO inventory at December 31, 2022 and 2023. 2. Will Webster account for the change (a) retrospectively or (b) prospectively? 1. LIFO inventory at 2022 LIFO inventory at 2023 2. Webster account for the changearrow_forward

- Goddard Company has used the FIFO method of inventory valuation since it began operations in 2018. Goddard decided to change to the average cost method for determining inventory costs at the beginning of 2021. The following schedule shows year-end inventory balances under the FIFO and average cost methods: Year FIFO Average Cost 2018 $45,000 $54,000 2019 78,000 71,000 2020 83,000 78,000 Required:1. Ignoring income taxes, prepare the 2021 journal entry to adjust the accounts to reflect the average cost method.2. How much higher or lower would cost of goods sold be in the 2020 revised income statement?arrow_forwardSheridan Inc. has selected specific identification as its inventory costing method. At December 31, 2025, it has the following information for its finished goods: \table[[Replacement value,$5980arrow_forwardSplish Company began operations in 2019 and determined its ending inventory at cost and at lower-of-LIFO cost-or-market at December 31, 2019, and December 31, 2020. This information is presented below: 12/31/19 $378,170 435,650 12/31/20 Cost 12/31/19 (a) Prepare the journal entries required at December 31, 2019, and December 31, 2020, assuming that the inventory is recorded at market, and a perpetual inventory system (cost-of-goods-sold method) is used. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No entry" for the account titles and enter O for the amounts.) 12/31/20 Lower-of-Cost-or-Market Date Account Titles and Explanation $358,260 419,900 12/31/20 Date Account Titles and Explanation 12/31/19 (b) Prepare journal entries required at December 31, 2019, and December 31, 2020, assuming that the inventory is recorded at market under a perpetual system (loss method is used). (Credit account titles are…arrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning