Concept explainers

Videos

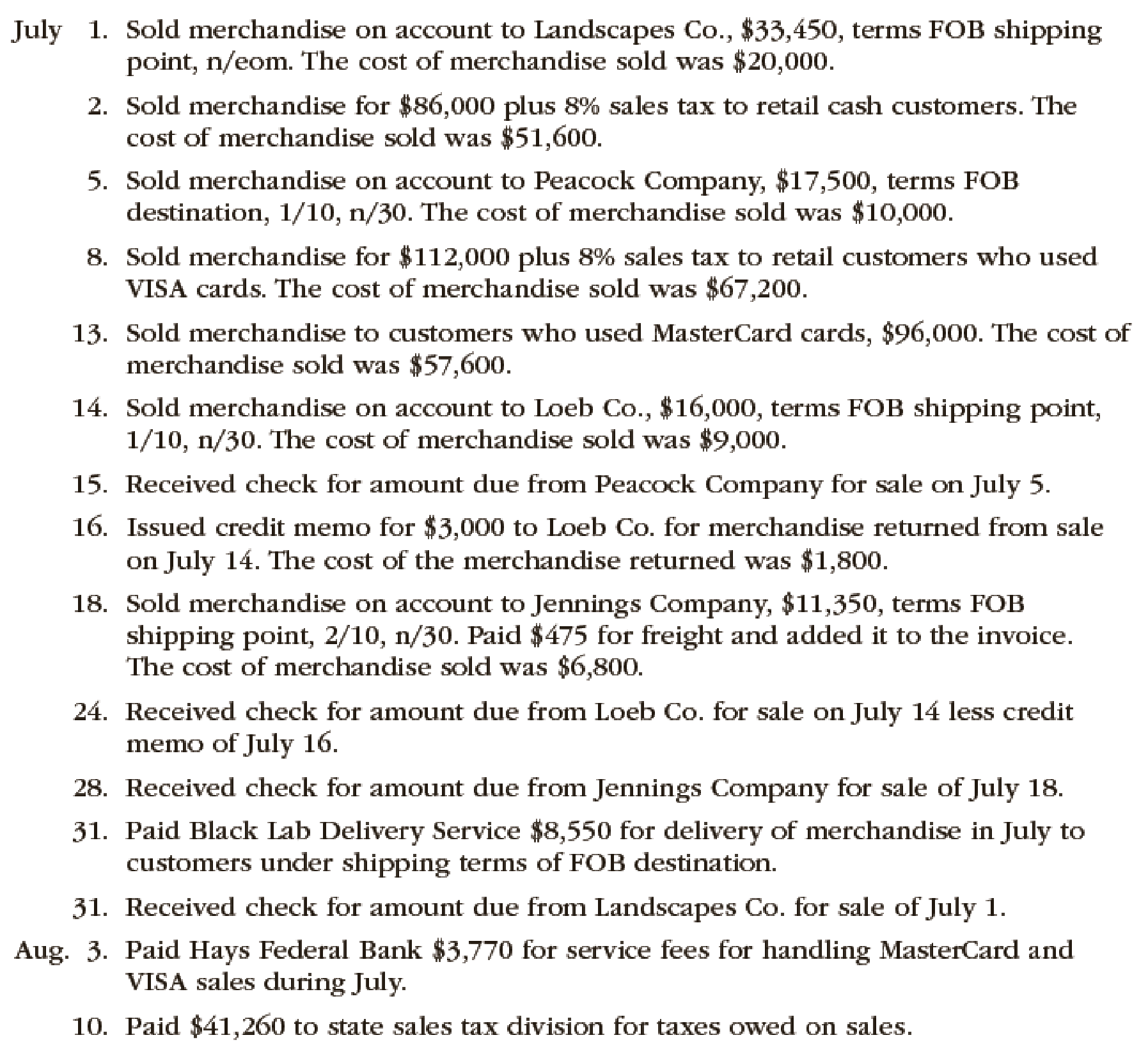

The following selected transactions were completed by Green Lawn Supplies Co., which sells irrigation supplies primarily to wholesalers and occasionally to retail customers:

Instructions

Record the sale transactions of the company.

Explanation of Solution

Sales is an activity of selling the merchandise inventory of a business.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Accounts receivable | 33,450 | |

| Sales Revenue | 33,450 | ||

| (To record the sale of inventory on account) |

Table (1)

- Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

- Sales revenue is revenue and it increases the value of equity by $33,450. Therefore, credit sales revenue with $33,450.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Cost of Merchandise Sold | 20,000 | |

| Merchandise Inventory | 20,000 | ||

| (To record the cost of goods sold) |

Table (2)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $20,000. Therefore, debit cost of merchandise sold account with $20,000.

- Merchandise Inventory is an asset and it is decreased by $20,000. Therefore, credit inventory account with $20,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cash | 92,880 (2) | |

| Sales Revenue | 86,000 | ||

| Sales Tax Payable | 6,880 (1) | ||

| (To record the sale of inventory for cash) |

Table (3)

- Cash is an asset and it is increased by $92,880. Therefore, debit cash account with $92,880.

- Sales revenue is revenue and it increases the value of equity by $86,000. Therefore, credit sales revenue with $86,000.

- Sales tax payable is a liability and it is increased by $6,880. Therefore, credit sales tax payable account with $6,880.

Working Note (1):

Calculate the amount of sales tax payable.

Sales revenue = $86,000

Sales tax percentage = 8%

Working Note (2):

Calculate the amount of cash received.

Sales revenue = $86,000

Sales tax payable = $6,880 (1)

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cost of Merchandise Sold | 51,600 | |

| Merchandise Inventory | 51,600 | ||

| (To record the cost of goods sold) |

Table (4)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $51,600. Therefore, debit cost of merchandise sold account with $51,600.

- Merchandise Inventory is an asset and it is decreased by $51,600. Therefore, credit inventory account with $51,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Accounts receivable | 17,325 (3) | |

| Sales Revenue | 17,325 | ||

| (To record the sale of inventory on account) |

Table (5)

- Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

- Sales revenue is revenue and it increases the value of equity by $17,325. Therefore, credit sales revenue with $17,325.

Working Note (3):

Calculate the amount of accounts receivable.

Sales = $17,500

Discount percentage = 1%

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Cost of Merchandise Sold | 10,000 | |

| Merchandise Inventory | 10,000 | ||

| (To record the cost of goods sold) |

Table (6)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $10,000. Therefore, debit cost of merchandise sold account with $10,000.

- Merchandise Inventory is an asset and it is decreased by $10,000. Therefore, credit inventory account with $10,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cash | 120,960 (5) | |

| Sales Revenue | 112,000 | ||

| Sales Tax Payable | 8,960 (4) | ||

| (To record the sale of inventory for cash) |

Table (7)

- Cash is an asset and it is increased by $120,960. Therefore, debit cash account with $120,960.

- Sales revenue is revenue and it increases the value of equity by $112,000. Therefore, credit sales revenue with $112,000.

- Sales tax payable is a liability and it is increased by $8,960. Therefore, credit sales tax payable account with $8,960.

Working Note (4):

Calculate the amount of sales tax payable.

Sales revenue = $112,000

Sales tax percentage = 8%

Working Note (5):

Calculate the amount of cash received.

Sales revenue = $112,000

Sales tax payable = $8,960 (4)

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cost of Merchandise Sold | 67,200 | |

| Merchandise Inventory | 67,200 | ||

| (To record the cost of goods sold) |

Table (8)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $67,200. Therefore, debit cost of merchandise sold account with $67,200.

- Merchandise Inventory is an asset and it is decreased by $67,200. Therefore, credit inventory account with $67,200.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cash | 96,000 | |

| Sales Revenue | 96,000 | ||

| (To record the sale of inventory for cash) |

Table (9)

- Cash is an asset and it is increased by $96,000. Therefore, debit cash account with $96,000.

- Sales revenue is revenue and it increases the value of equity by $96,000. Therefore, credit sales revenue with $96,000.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cost of Merchandise Sold | 57,600 | |

| Merchandise Inventory | 57,600 | ||

| (To record the cost of goods sold) |

Table (10)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $57,600. Therefore, debit cost of merchandise sold account with $57,600.

- Merchandise Inventory is an asset and it is decreased by $57,600. Therefore, credit inventory account with $57,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Accounts receivable | 15,840 (6) | |

| Sales Revenue | 15,840 | ||

| (To record the sale of inventory on account) |

Table (11)

- Accounts Receivable is an asset and it is increased by $15,840. Therefore, debit accounts receivable with $15,840.

- Sales revenue is revenue and it increases the value of equity by $15,840. Therefore, credit sales revenue with $15,840.

Working Note (6):

Calculate the amount of accounts receivable.

Sales = $16,000

Discount percentage = 1%

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Cost of Merchandise Sold | 9,000 | |

| Merchandise Inventory | 9,000 | ||

| (To record the cost of goods sold) |

Table (12)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $9,000. Therefore, debit cost of merchandise sold account with $9,000.

- Merchandise Inventory is an asset and it is decreased by $9,000. Therefore, credit inventory account with $9,000.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 15 | Cash | 17,325 | |

| Accounts Receivable | 17,325 | ||

| (To record the receipt of cash against accounts receivables) |

Table (13)

- Cash is an asset and it is increased by $17,325. Therefore, debit cash account with $17,325.

- Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

Record the journal entry for sales return.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 16 | Customer Refunds Payable | 2,970 (7) | ||

| Accounts Receivable | 2,970 | |||

| (To record sales returns) |

Table (14)

- Customer refunds payable is a liability account and it is decreased by $2,970. Therefore, debit customer refunds payable account with $2,970.

- Accounts Receivable is an asset and it is decreased by $2,970. Therefore, credit account receivable with $2,970.

Working Note (7):

Calculate the amount of refund owed to the customer.

Sales return = $3,000

Discount percentage = 1%

Record the journal entry for the return of the merchandise.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 16 | Merchandise Inventory | 1,800 | |

| Estimated Returns Inventory | 1,800 | ||

| (To record the return of the merchandise) |

Table (15)

- Merchandise Inventory is an asset and it is increased by $1,800. Therefore, debit inventory account with $1,800.

- Estimated retunrs inventory is an expense account and it increases the value of equity by $1,800. Therefore, credit estimated returns inventory account with $1,800.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Accounts receivable | 11,123 (8) | |

| Sales Revenue | 11,123 | ||

| (To record the sale of inventory on account) |

Table (16)

- Accounts Receivable is an asset and it is increased by $11,123. Therefore, debit accounts receivable with $11,123.

- Sales revenue is revenue and it increases the value of equity by $11,123. Therefore, credit sales revenue with $11,123.

Working Note (8):

Calculate the amount of accounts receivable.

Sales = $11,350

Discount percentage = 2%

- Accounts Receivable is an asset and it is increased by $475. Therefore, debit accounts receivable with $475.

- Cash is an asset and it is decreased by $475. Therefore, credit cash account with $475.

Record the journal entry for freight charges paid.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 18 | Accounts Receivable | 475 | ||

| Cash | 475 | |||

| (To record freight charges paid) |

Table (17)

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Cost of Merchandise Sold | 6,800 | |

| Merchandise Inventory | 6,800 | ||

| (To record the cost of goods sold) |

Table (18)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $6,800. Therefore, debit cost of merchandise sold account with $6,800.

- Merchandise Inventory is an asset and it is decreased by $6,800. Therefore, credit inventory account with $6,800.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 24 | Cash | 12,870 (9) | |

| Accounts Receivable | 12,870 | ||

| (To record the receipt of cash against accounts receivables) |

Table (19)

- Cash is an asset and it is increased by $12,870. Therefore, debit cash account with $12,870.

- Accounts Receivable is an asset and it is increased by $12,870. Therefore, debit accounts receivable with $12,870.

Working Note (9):

Calculate the amount of cash received.

Net accounts receivable = $15,840

Customer refunds payable = $2,970

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 28 | Cash | 11,598 (10) | |

| Accounts Receivable | 11,598 | ||

| (To record the receipt of cash against accounts receivables) |

Table (20)

- Cash is an asset and it is increased by $11,598. Therefore, debit cash account with $11,598.

- Accounts Receivable is an asset and it is increased by $11,598. Therefore, debit accounts receivable with $11,598.

Working Note (10):

Calculate the amount of cash received.

Net accounts receivable = $11,123

Freight charges = $475

Record the journal entry for delivery expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 31 | Delivery expense | 8,550 | |

| Cash | 8,550 | ||

| (To record the payment of delivery expenses) |

Table (21)

- Delivery expense is an expense account and it decreases the value of equity by $8,550. Therefore, debit delivery expense account with $8,550.

- Cash is an asset and it is decreased by $8,550. Therefore, credit cash account with $8,550.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 31 | Cash | 33,450 | |

| Accounts Receivable | 33,450 | ||

| (To record the receipt of cash against accounts receivables) |

Table (22)

- Cash is an asset and it is increased by $33,450. Therefore, debit cash account with $33,450.

- Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 3 | Credit card expense | 3,770 | |

| Cash | 3,770 | ||

| (To record the payment of credit card expenses) |

Table (23)

- Credit card expense is an expense account and it decreases the value of equity by $3,770. Therefore, debit credit card expense account with $3,770.

- Cash is an asset and it is decreased by $3,770. Therefore, credit cash account with $3,770.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 10 | Sales tax payable | 41,260 | |

| Cash | 41,260 | ||

| (To record the payment of credit card expenses) |

Table (24)

- Sales tax payable is a liability account and it is decreased by $41,260. Therefore, debit customer refunds payable account with $41,260.

- Cash is an asset and it is decreased by $41,260. Therefore, credit cash account with $41,260.

Want to see more full solutions like this?

Chapter 6 Solutions

FINANCIAL ACCOUNTING

- Record journal entries for the following sales transactions of Flower Company.arrow_forwardthe purchases and disbursements cycle usually begins when a. a user department request for acquisition of goods or services and submits purchase requisition to the purchasing department b. a check is issued to the vendor or supplier c. the warehouse is received the goods from the vendor or supplier d. the accounting posts the purchase transaction in the accounts payable ledgerarrow_forwardPrepare journal entries for the following transactions from Lumber Wholesale.arrow_forward

- Record journal entries for the following purchase transactions of Balloon Depot.arrow_forwardPrepare general journal entries for the following transactions of Valdez Services.arrow_forwardReview the following transactions for Dish Mart and record any required journal entries. Note that all purchase transactions are with the same supplier.arrow_forward

- The journal entry recorded for the sale of office equipment includes:arrow_forwardFor each of the following records, indicate the appropriate related file structure: master file, transaction file, reference file, or archive file.a. customer ledgersb. purchase ordersc. list of authorized vendorsd. records related to prior pay periodse. vendor ledgersf. hours each employee has worked during the current pay periodg. tax tablesh. sales orders that have been processed and recordedarrow_forwardSales-related transactions using perpetual inventory system The following selected transactions were completed by Green Lawn Supplies Co., which sells irrigation supplies primarily to other businesses and occasionally to retail customers: Instructions Journalize the entries to record the transactions of Green Lawn Supplies Co.arrow_forward

- The debits and credits from three related transactions are presented in the following customers account taken from the accounts receivable subsidiary ledger: Describe each transaction and identify the source of each posting.arrow_forwardA company indicates the condition of goods obtained onwhich of the following documents?a. Purchase requisitionb. Purchase orderc. Receiving reportd. Supplier invoicearrow_forwardRecord the following transactions for Redeker Co. in the general journal.arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub