Concept explainers

Videos

This problem is designed to enable you to apply the knowledge you have acquired in the preceding chapters. In accounting, the ultimate test is being able to handle data in real-life situations. This problem will give you valuable experience.

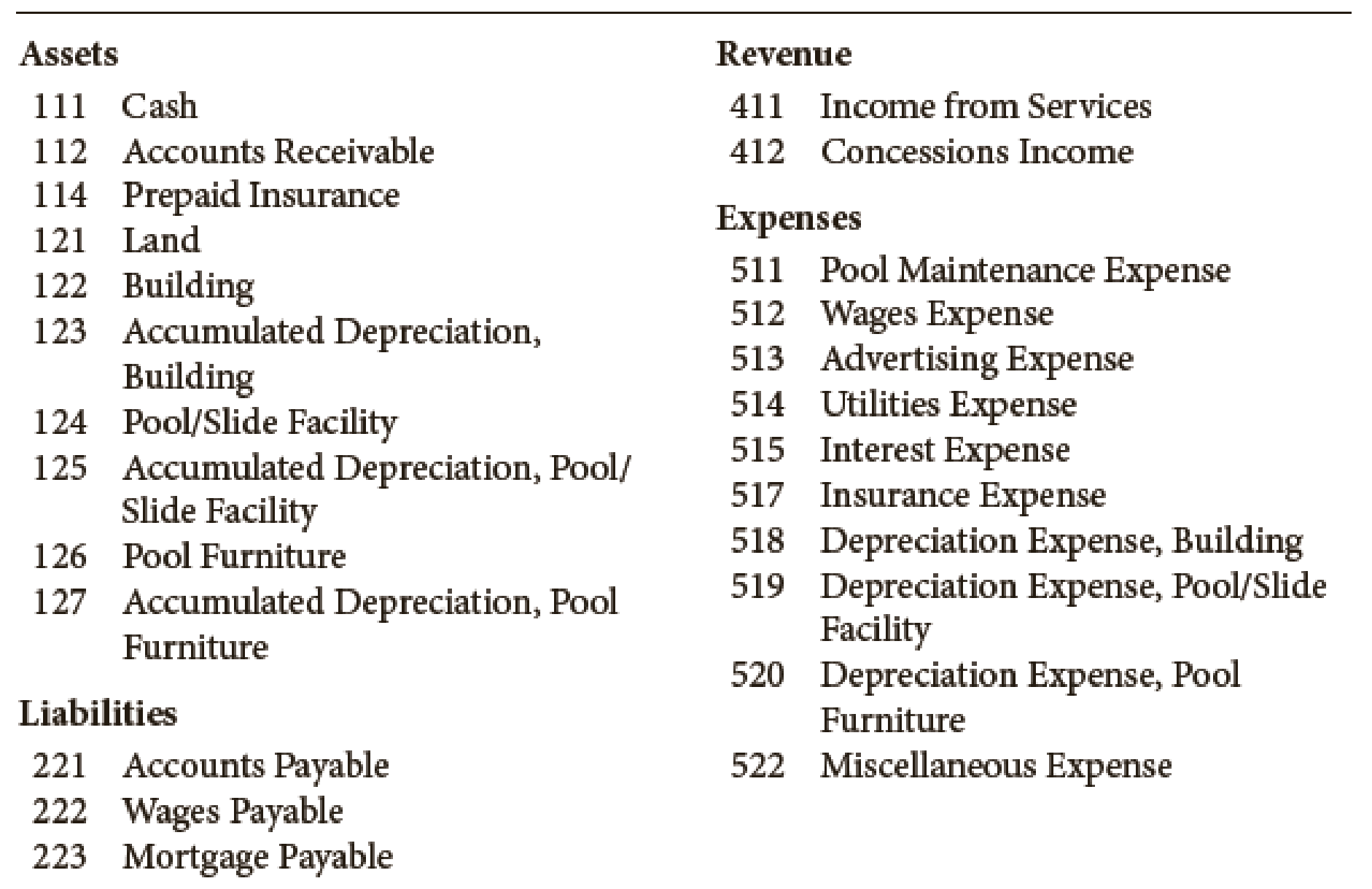

CHART OF ACCOUNTS

You are to record transactions in a two-column general journal. Assume that the fiscal period is one month. You will then be able to complete all of the steps in the accounting cycle.

When you are analyzing the transactions, think them through by visualizing the T accounts or by writing them down on scratch paper. For unfamiliar types of transactions, specific instructions for recording them are included. However, reason them out for yourself as well. Check off each transaction as it is recorded.

Required

- 1. Journalize the transactions. (Start on page 1 of the general journal if using Excel or Working Papers.)

- 2. Post the transactions to the ledger accounts. (Skip this step if using CLGL.)

- 3. Prepare a

trial balance . (If using a work sheet, use the first two columns.) - 4. Data for the adjustments are as follows:

- a. Insurance expired during the month, $1,020.

- b.

Depreciation of building for the month, $480. - c. Depreciation of pool/slide facility for the month, $675.

- d. Depreciation of pool furniture for the month, $220.

- e. Wages accrued at July 31, $920.

Your instructor may want you to use a work sheet for these adjustments.

- 5. Journalize

adjusting entries . - 6. Post adjusting entries to the ledger accounts. (Skip this step if using CLGL.)

- 7. Prepare an adjusted trial balance.

- 8. Prepare the income statement.

- 9. Prepare the statement of owner’s equity.

- 10. Prepare the

balance sheet . - 11. Journalize closing entries.

- 12.

Post closing entries to the ledger accounts. (Skip this step if using CLGL.) - 13. Prepare a post-closing trial balance.

Check Figure

Trial balance total, $601,941; net income, $16,293; post-closing trial balance total, $569,614

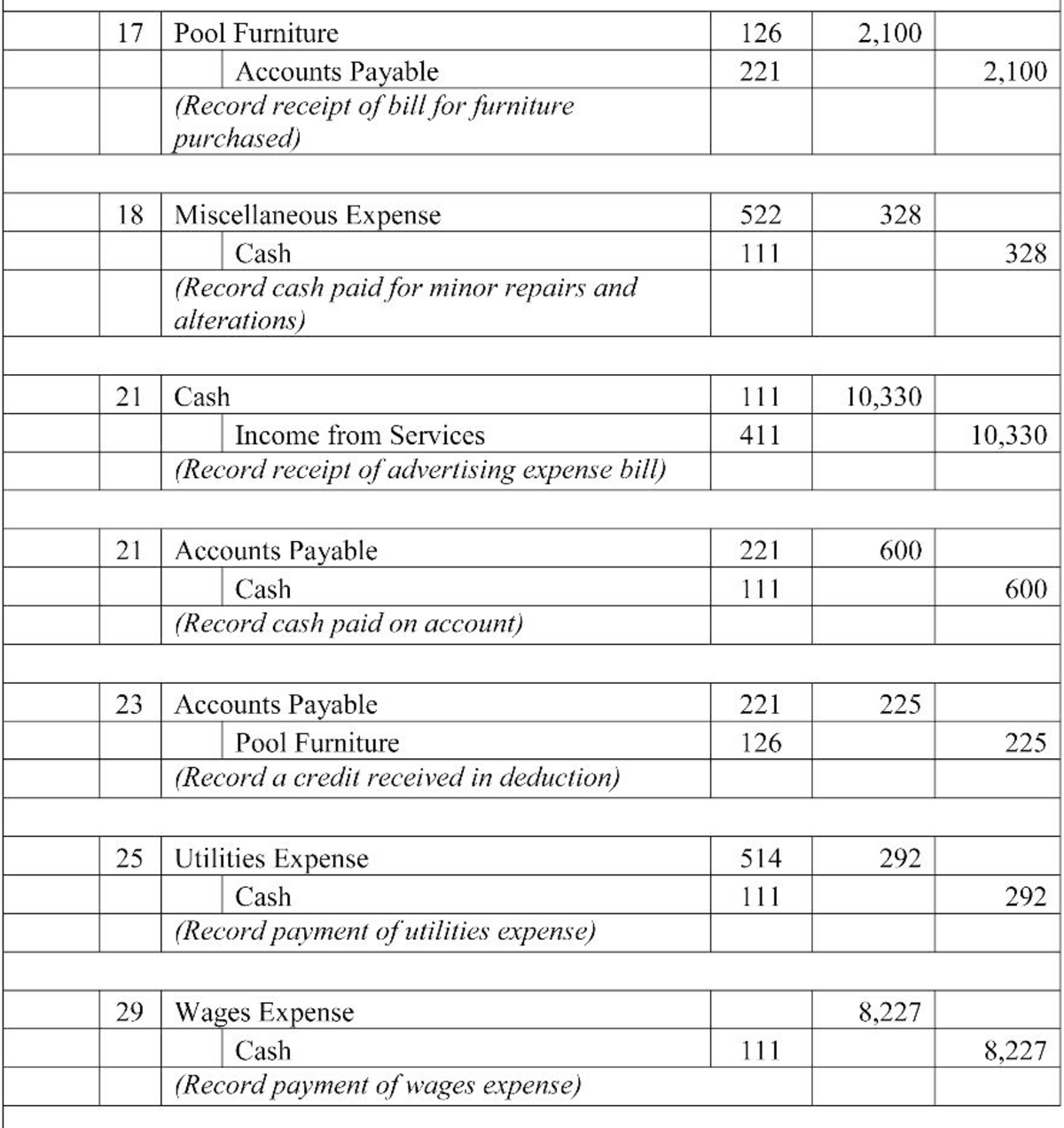

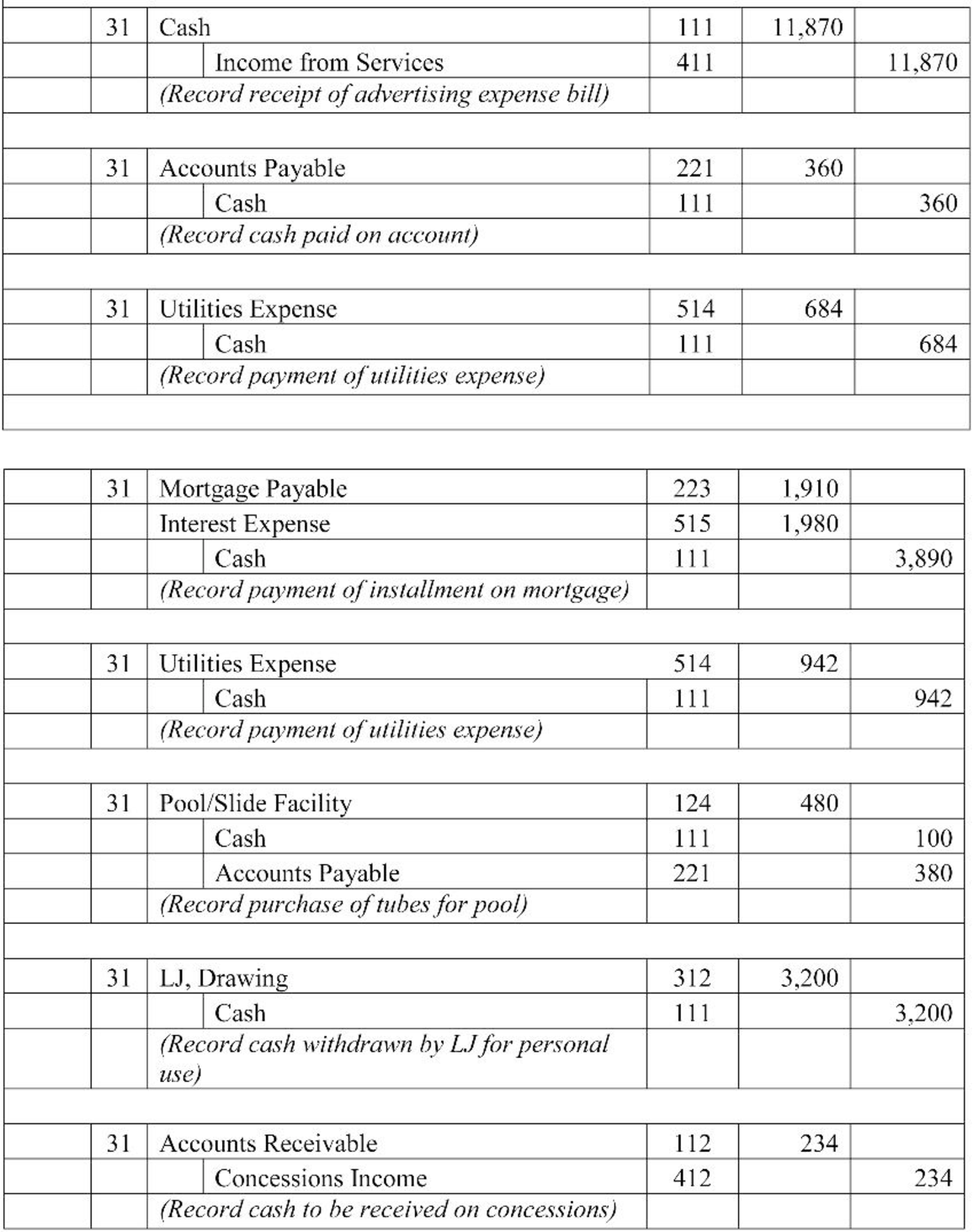

1.

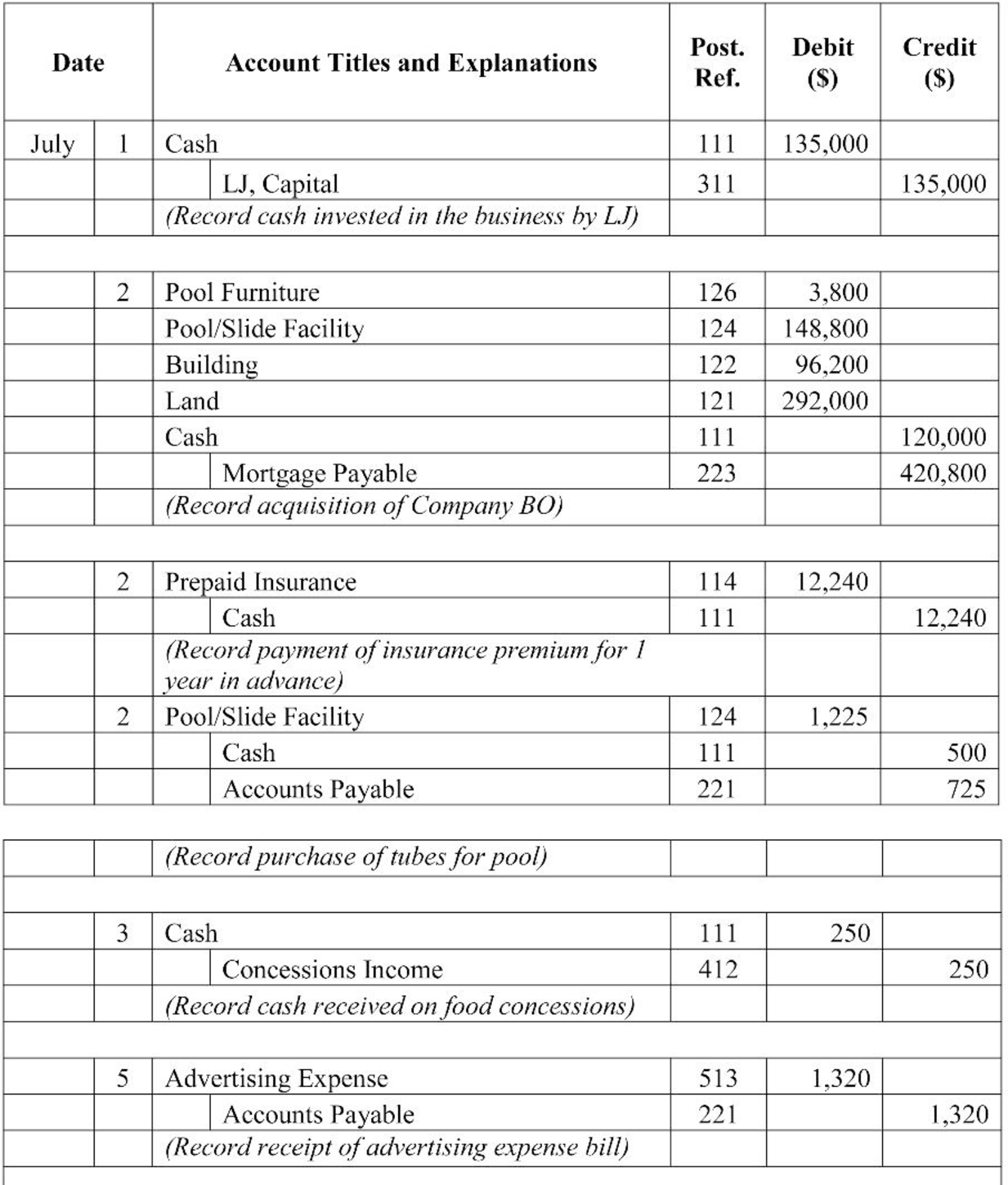

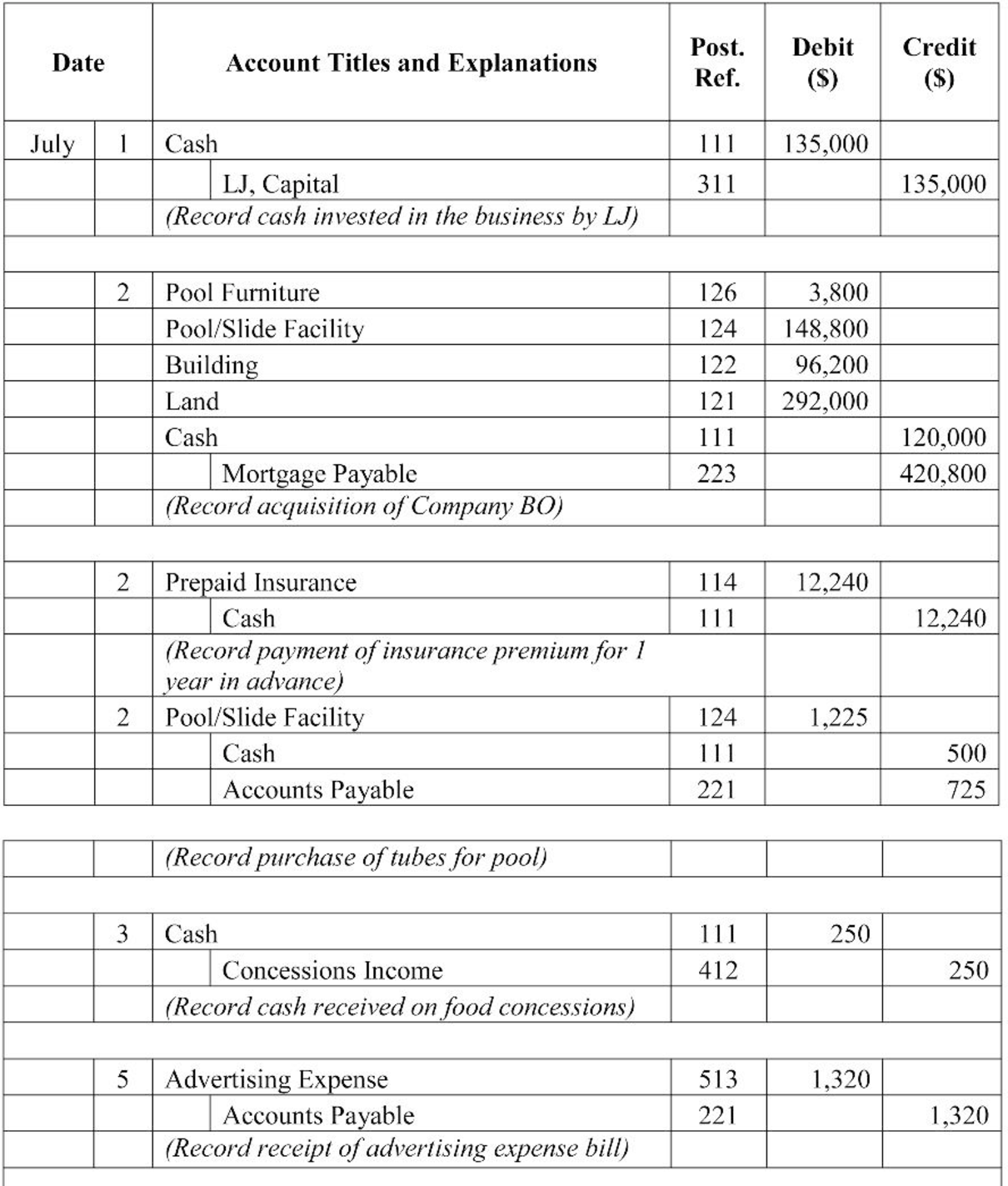

Prepare journal entries for the given transactions for Company BO.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entries for the given transactions for Company BO.

Table (1)

Table (2)

Table (3)

Table (4)

2.

Post the journalized transactions in the ledger accounts of the general ledger.

Explanation of Solution

Ledger: Ledger is a book in which the accounts are summarized and grouped from the transactions recorded in the journal.

Post the journalized transactions in the ledger accounts of the general ledger.

| ACCOUNT Cash ACCOUNT NO. 111 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 1 | 1 | 135,000 | 135,000 | |||

| 2 | 1 | 120,000 | 15,000 | ||||

| 2 | 1 | 12,240 | 2,760 | ||||

| 2 | 1 | 500 | 2,260 | ||||

| 3 | 1 | 250 | 2,510 | ||||

| 6 | 1 | 1,600 | 910 | ||||

| 6 | 2 | 128 | 782 | ||||

| 7 | 2 | 12,086 | 12,868 | ||||

| 14 | 2 | 10,445 | 23,313 | ||||

| 15 | 2 | 9,460 | 13,853 | ||||

| 16 | 2 | 1,150 | 12,703 | ||||

| 16 | 2 | 2,500 | 10,203 | ||||

| 18 | 3 | 328 | 9,875 | ||||

| 21 | 3 | 10,330 | 20,205 | ||||

| 21 | 3 | 600 | 19,605 | ||||

| 25 | 3 | 292 | 19,313 | ||||

| 29 | 3 | 8,227 | 11,086 | ||||

| 31 | 3 | 11,870 | 22,956 | ||||

| 31 | 3 | 360 | 22,596 | ||||

| 31 | 3 | 684 | 21,912 | ||||

| 31 | 4 | 3,890 | 18,022 | ||||

| 31 | 4 | 942 | 17,080 | ||||

| 31 | 4 | 100 | 16,980 | ||||

| 31 | 4 | 3,200 | 13,780 | ||||

Table (2)

| ACCOUNT Accounts Receivable ACCOUNT NO. 112 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 7 | 4 | 234 | 234 | |||

Table (3)

| ACCOUNT Prepaid Insurance ACCOUNT NO. 114 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 2 | 1 | 12,240 | 12,240 | |||

Table (4)

| ACCOUNT Land ACCOUNT NO. 121 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 2 | 1 | 292,000 | 292,000 | |||

Table (5)

| ACCOUNT Building ACCOUNT NO. 122 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 2 | 1 | 96,200 | 96,200 | |||

Table (6)

| ACCOUNT Pool/Slide Facility ACCOUNT NO. 124 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 2 | 1 | 148,800 | 148,800 | |||

| 2 | 1 | 1,225 | 150,025 | ||||

| 31 | 4 | 480 | 150,505 | ||||

Table (7)

| ACCOUNT Pool Furniture ACCOUNT NO. 126 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 2 | 1 | 148,800 | 148,800 | |||

| 2 | 1 | 1,225 | 150,025 | ||||

| 31 | 4 | 480 | 150,505 | ||||

Table (8)

| ACCOUNT Accounts Payable ACCOUNT NO. 221 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 2 | 1 | 725 | 725 | |||

| 5 | 1 | 1,320 | 2,045 | ||||

| 9 | 2 | 646 | 2,691 | ||||

| 16 | 2 | 1,150 | 1,541 | ||||

| 17 | 2 | 2,100 | 3,641 | ||||

| 21 | 3 | 600 | 3,041 | ||||

| 23 | 3 | 225 | 2,816 | ||||

| 31 | 3 | 360 | 2,456 | ||||

| 31 | 4 | 380 | 2,836 | ||||

Table (9)

| ACCOUNT Mortgage Payable ACCOUNT NO. 223 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 2 | 1 | 420,800 | 420,800 | |||

| 31 | 4 | 1,910 | 418,890 | ||||

Table (10)

| ACCOUNT LJ, Capital ACCOUNT NO. 311 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 1 | 1 | 135,000 | 135,000 | |||

Table (11)

| ACCOUNT LJ, Drawing ACCOUNT NO. 312 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 16 | 2 | 2,500 | 2,500 | |||

| 31 | 4 | 3,200 | 5,700 | ||||

Table (12)

| ACCOUNT Income from Services ACCOUNT NO. 411 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 7 | 2 | 12,086 | 12,086 | |||

| 14 | 2 | 10,445 | 22,531 | ||||

| 21 | 3 | 10,330 | 32,861 | ||||

| 31 | 3 | 11,870 | 44,731 | ||||

Table (13)

| ACCOUNT Concessions Income ACCOUNT NO. 412 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 3 | 2 | 250 | 250 | |||

| 31 | 2 | 234 | 484 | ||||

Table (14)

| ACCOUNT Pool Maintenance Expense ACCOUNT NO. 511 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 6 | 1 | 1,600 | 1,600 | |||

| 9 | 2 | 646 | 2,246 | ||||

Table (15)

| ACCOUNT Wages Expense ACCOUNT NO. 512 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 15 | 2 | 9,460 | 9,460 | |||

| 29 | 3 | 8,227 | 17,687 | ||||

Table (16)

| ACCOUNT Advertising Expense ACCOUNT NO. 513 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 5 | 2 | 1,320 | 1,320 | |||

Table (17)

| ACCOUNT Utilities Expense ACCOUNT NO. 514 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 25 | 3 | 292 | 292 | |||

| 31 | 3 | 684 | 976 | ||||

| 31 | 4 | 942 | 1,918 | ||||

Table (18)

| ACCOUNT Interest Expense ACCOUNT NO. 515 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | 4 | 1,980 | 1,980 | |||

Table (19)

| ACCOUNT Miscellaneous Expense ACCOUNT NO. 522 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 6 | 2 | 128 | 128 | |||

| 18 | 3 | 328 | 456 | ||||

Table (20)

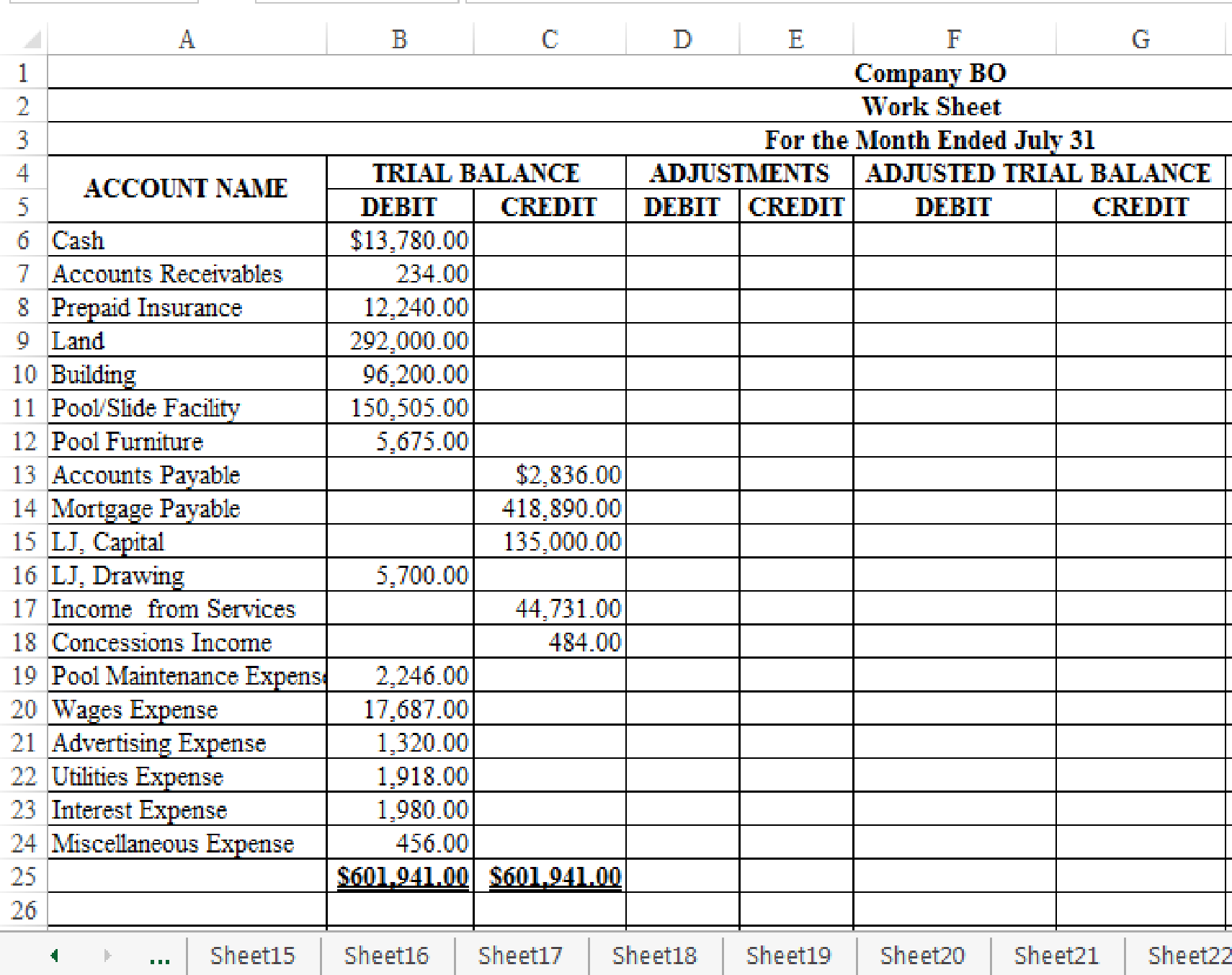

3.

Prepare trial balance on the work sheet, from the account balances in Part (2).

Explanation of Solution

Worksheet: Worksheet is an accounting tool that help accountants to record adjustments and up-date balances required to prepare financial statements. Worksheet is a central place where trial balance, adjustments, adjusted trial balance, income statement, and balance sheet are presented.

Trial balance: Trial balance is a summary of all the asset, liability, and equity accounts and their balances.

Prepare trial balance on the work sheet, from the account balances in Part (2).

Figure – (1)

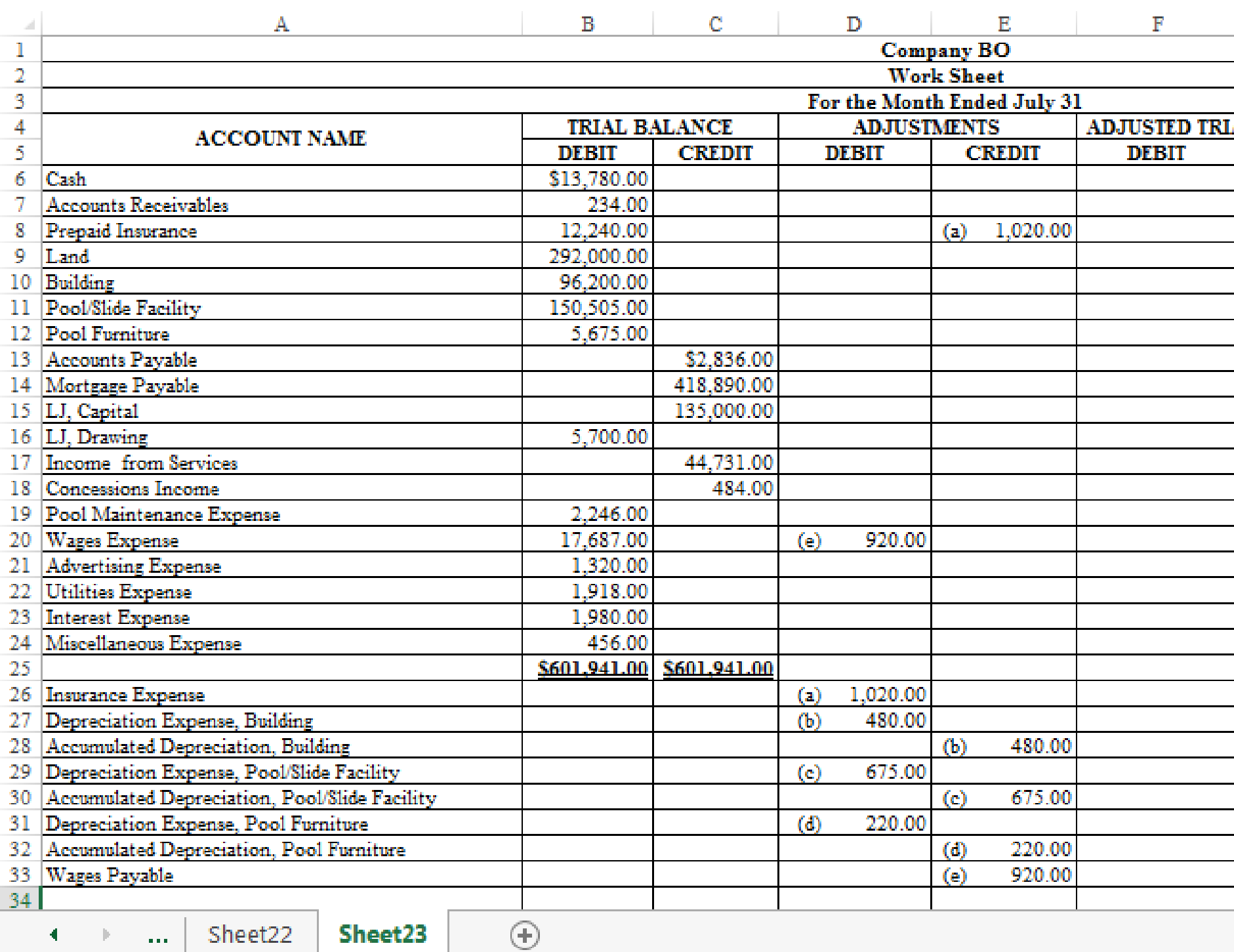

4.

Indicate the given adjustments on the worksheet for Company BO for the month ended July 31, 20--.

Explanation of Solution

Worksheet: Worksheet is an accounting tool that help accountants to record adjustments and up-date balances required to prepare financial statements. Worksheet is a central place where trial balance, adjustments, adjusted trial balance, income statement, and balance sheet are presented.

Indicate the given adjustments on the worksheet for Company BO for the month ended July 31, 20--.

Figure-(2)

5.

Prepare adjusting journal entries for Company BO.

Explanation of Solution

Adjusting entries: Adjusting entries are those entries which are recorded at the end of the year, to update the income statement accounts (revenue and expenses) and balance sheet accounts (assets, liabilities, and owners’ or stockholders’ equity) to maintain the records according to accrual basis principle and matching concept.

Prepare adjusting journal entries for Company BO.

Adjusting entry (a) for the prepaid insurance:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| July | 31 | Insurance Expense | 517 | 1,020 | ||

| Prepaid Insurance | 114 | 1,020 | ||||

| (Record part of prepaid insurance expired) | ||||||

Table (21)

Description:

- Insurance Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Prepaid Insurance is an asset account. Since amount of insurance is expired, asset account decreased, and a decrease in asset is credited.

Adjusting entry (b) for the depreciation expense for building:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| July | 31 | Depreciation Expense, Building | 518 | 480 | ||

| Accumulated Depreciation, Building | 123 | 480 | ||||

| (Record depreciation expense) | ||||||

Table (22)

Description:

- Depreciation Expense, Building is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Accumulated Depreciation, Building is a contra-asset account, and contra-asset accounts would have a normal credit balance, hence, the account is credited.

Adjusting entry (c) for the depreciation expense for pool/slide facility:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| July | 31 | Depreciation Expense, Pool/Slide Facility | 519 | 675 | ||

| Accumulated Depreciation, Pool/Slide Facility | 125 | 675 | ||||

| (Record depreciation expense) | ||||||

Table (23)

Description:

- Depreciation Expense, Pool/Slide Facility is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Accumulated Depreciation, Pool/Slide Facility is a contra-asset account, and contra-asset accounts would have a normal credit balance, hence, the account is credited.

Adjusting entry (d) for the depreciation expense for pool/slide facility:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| July | 31 | Depreciation Expense, Pool Furniture | 520 | 220 | ||

| Accumulated Depreciation, Pool Furniture | 127 | 220 | ||||

| (Record depreciation expense) | ||||||

Table (24)

Description:

- Depreciation Expense, Pool Furniture is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Accumulated Depreciation, Pool Furniture is a contra-asset account, and contra-asset accounts would have a normal credit balance, hence, the account is credited.

Adjusting entry (e) for the wages expense:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| July | 31 | Wages Expense | 512 | 920 | ||

| Wages Payable | 222 | 920 | ||||

| (Record accrued wages expenses) | ||||||

Table (25)

Description:

- Wages Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Wages Payable is a liability account. Since amount of payables has increased, liability decreased, and an increase in liability is credited.

6.

Post the adjusting entries journalized in Part (5) in the ledger accounts of general ledger.

Explanation of Solution

Post the adjusting entries journalized in Part (5) in the ledger accounts of general ledger.

| ACCOUNT Prepaid Insurance ACCOUNT NO. 114 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 2 | 1 | 12,240 | 12,240 | |||

| 31 | Adjusting | 1,020 | 11,220 | ||||

Table (26)

| ACCOUNT Accumulated Depreciation, Building ACCOUNT NO. 123 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 480 | 480 | |||

Table (27)

| ACCOUNT Accumulated Depreciation, Pool/Slide Facility ACCOUNT NO. 125 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 675 | 675 | |||

Table (28)

| ACCOUNT Accumulated Depreciation, Pool Furniture ACCOUNT NO. 127 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 220 | 220 | |||

Table (29)

| ACCOUNT Wages Payable ACCOUNT NO. 222 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 920 | 920 | |||

Table (30)

| ACCOUNT Wages Expense ACCOUNT NO. 512 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 15 | 2 | 9,460 | 9,460 | |||

| 29 | 3 | 8,227 | 17,687 | ||||

| 31 | Adjusting | 920 | 18,607 | ||||

Table (31)

| ACCOUNT Insurance Expense ACCOUNT NO. 517 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 2 | 1,020 | 1,020 | ||

Table (32)

| ACCOUNT Depreciation Expense, Building ACCOUNT NO. 518 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 480 | 480 | |||

Table (33)

| ACCOUNT Depreciation Expense, Pool/Slide Facility ACCOUNT NO. 519 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 675 | 675 | |||

Table (34)

| ACCOUNT Depreciation Expense, Pool Furniture ACCOUNT NO. 520 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 220 | 220 | |||

Table (35)

7.

Prepare an adjusted trial balance for Company BO as at July 31, 20--, based on the account balances derived in Parts (2) and (6).

Explanation of Solution

Adjusted trial balance: The trial balance which reflects the adjusting entries and incorporates the effect of all adjustments in the ledger accounts, is referred to as adjusted trial balance.

Prepare an adjusted trial balance for Company BO as at July 31, 20--, based on the account balances derived in Parts (2) and (6).

Figure - (3)

8.

Prepare an income statement of Company BO for the month ended July 31, based on the account balances derived in Parts (2) and (6).

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations, and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare an income statement of Company BO for the month ended July 31.

Figure - (4)

9.

Prepare a statement of owners’ equity of Company BO, based on the account balances derived in Parts (2) and (6), and net income computed in Part (8).

Explanation of Solution

Statement of owners’ equity: This statement reports the beginning owner’s equity and all the changes which led to ending owners’ equity. Additional capital, net income from income statement is added to, and drawings are deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Prepare a statement of owners’ equity for Company BO for the month ended July 31.

| Company BO | ||

| Statement of Owners’ Equity | ||

| For the Month Ended July 31, 20-- | ||

| LJ, Capital, July 1, 20-- | $0 | |

| Investments during July | $135,000 | |

| Net income for July | 16,293 | |

| 151,293 | ||

| Less: Withdrawals for July | 5,700 | |

| Increase in capital | 145,593 | |

| LJ, Capital, July 31, 20-- | $145,593 | |

Table (36)

10.

Prepare a balance sheet for Company BO, based on the account balances derived in Parts (2) and (6), and capital of the owner from the statement of owners’ equity prepared in Part (9).

Explanation of Solution

Balance sheet: This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and owners (owners’ equity) over those resources. The resources of the company are assets which include money contributed by owners and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and owners’ equity.

Prepare the balance sheet for Company BO as at July 31, 20--.

Table (37)

11.

Prepare closing entries numbering the entries 1 through 4.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to capital account are referred to as closing entries. The revenue, expense, and drawing accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Steps in closing procedure:

- 1. Close the revenue accounts to Income Summary account.

- 2. Close the expense accounts to Income Summary account.

- 3. Close the Income Summary account and transfer the net income or net loss balance to the Capital account.

- 4. Close the Drawing account to Capital account.

Prepare closing entries numbering the entries 1 through 4.

Entry 1:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| July | 31 | Income from Services | 411 | 44,731 | ||

| Concessions Income | 412 | 484 | ||||

| Income Summary | 313 | 45,215 | ||||

| (Record closing of revenue to Income Summary account) | ||||||

Table (38)

Description:

- Income from Services and Concessions Income are revenue accounts. Revenue account has a normal credit balance. Since revenue is closed to Income Summary account, the account is debited.

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. The account is credited to hold the transferred balance from revenue account.

Entry 2:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| July | 31 | Income Summary | 28,922 | |||

| Pool Maintenance Expense | 2,246 | |||||

| Wages Expense | 18,607 | |||||

| Advertising Expense | 1,320 | |||||

| Utilities Expense | 1,918 | |||||

| Interest Expense | 1,980 | |||||

| Insurance Expense | 1,020 | |||||

| Depreciation Expense, Building | 480 | |||||

| Depreciation Expense, Pool/Slide Facility | 675 | |||||

| Depreciation Expense, Pool Furniture | 220 | |||||

| Miscellaneous Expense | 456 | |||||

| (Record closing of expenses to Income Summary account) | ||||||

Table (39)

Description:

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. The account is debited to hold the transferred balance from expense accounts.

- All expense accounts have a normal debit balance. Since expenses are closed to Income Summary account, the accounts are credited.

Entry 3:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| July | 31 | Income Summary | 16,293 | |||

| LJ, Capital | 16,293 | |||||

| (Record closing of net income to capital account) | ||||||

Table (40)

Description:

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. Since net income is closed, the account is reversed, hence, the Income Summary account is debited.

- LJ, Capital is a capital account. Since net income is transferred to the account, the value increased, and an increase in capital is credited.

Entry 4:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| July | 31 | LJ, Capital | 5,700 | |||

| LJ, Drawing | 5,700 | |||||

| (Record closing of drawing to capital account) | ||||||

Table (41)

Description:

- LJ, Capital is a capital account. Since drawings is transferred to the account, the value decreased, and a decrease in capital is debited.

- LJ, Drawing is a capital account. Since drawings is transferred, the account is credited to reverse the previously debited effect.

12.

Post the closing entries to ledger accounts.

Explanation of Solution

Post the closing entries to ledger accounts.

| ACCOUNT LJ, Capital ACCOUNT NO. 311 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 1 | 1 | 135,000 | 135,000 | |||

| 31 | Closing | 16,293 | 151,293 | ||||

| 31 | Closing | 5,700 | 145,593 | ||||

Table (42)

| ACCOUNT LJ, Drawing ACCOUNT NO. 312 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 16 | 2 | 2,500 | 2,500 | |||

| 31 | 4 | 3,200 | 5,700 | ||||

| 31 | Closing | 5,700 | 0 | ||||

Table (43)

| ACCOUNT Income from Services ACCOUNT NO. 411 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 7 | 2 | 12,086 | 12,086 | |||

| 14 | 2 | 10,445 | 22,531 | ||||

| 21 | 3 | 10,330 | 32,861 | ||||

| 31 | 3 | 11,870 | 44,731 | ||||

| 31 | Closing | 44,731 | 0 | ||||

Table (44)

| ACCOUNT Concessions Income ACCOUNT NO. 412 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 3 | 2 | 250 | 250 | |||

| 31 | 2 | 234 | 484 | ||||

| 31 | Closing | 484 | 0 | ||||

Table (45)

| ACCOUNT Pool Maintenance Expense ACCOUNT NO. 511 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 6 | 1 | 1,600 | 1,600 | |||

| 9 | 2 | 646 | 2,246 | ||||

| 31 | Closing | 2,246 | 0 | ||||

Table (46)

| ACCOUNT Wages Expense ACCOUNT NO. 512 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 15 | 2 | 9,460 | 9,460 | |||

| 29 | 3 | 8,227 | 17,687 | ||||

| 31 | Closing | 17,687 | 0 | ||||

Table (47)

| ACCOUNT Advertising Expense ACCOUNT NO. 513 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 5 | 2 | 1,320 | 1,320 | |||

| 31 | Closing | 1,320 | 0 | ||||

Table (48)

| ACCOUNT Utilities Expense ACCOUNT NO. 514 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 25 | 3 | 292 | 292 | |||

| 31 | 3 | 684 | 976 | ||||

| 31 | 4 | 942 | 1,918 | ||||

| 31 | Closing | 1,918 | 0 | ||||

Table (49)

| ACCOUNT Interest Expense ACCOUNT NO. 515 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | 4 | 1,980 | 1,980 | |||

| 31 | Closing | 1,980 | 0 | ||||

Table (50)

| ACCOUNT Miscellaneous Expense ACCOUNT NO. 522 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 6 | 2 | 128 | 128 | |||

| 18 | 3 | 328 | 456 | ||||

| 31 | Closing | 456 | 0 | ||||

Table (51)

| ACCOUNT Wages Expense ACCOUNT NO. 512 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 15 | 2 | 9,460 | 9,460 | |||

| 29 | 3 | 8,227 | 17,687 | ||||

| 31 | Adjusting | 920 | 18,607 | ||||

| 31 | Closing | 18,607 | 0 | ||||

Table (52)

| ACCOUNT Insurance Expense ACCOUNT NO. 517 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 2 | 1,020 | 1,020 | ||

| 31 | Closing | 1,020 | 0 | ||||

Table (53)

| ACCOUNT Depreciation Expense, Building ACCOUNT NO. 518 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 480 | 480 | |||

| 31 | Closing | 480 | 0 | ||||

Table (54)

| ACCOUNT Depreciation Expense, Pool/Slide Facility ACCOUNT NO. 519 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 675 | 675 | |||

| 31 | Closing | 675 | 0 | ||||

Table (55)

| ACCOUNT Depreciation Expense, Pool Furniture ACCOUNT NO. 520 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Adjusting | 220 | 220 | |||

| 31 | Closing | 220 | 0 | ||||

Table (56)

| ACCOUNT Income Summary ACCOUNT NO. 313 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| July | 31 | Closing | 45,215 | 45,215 | |||

| 31 | Closing | 28,922 | 16,293 | ||||

| 31 | Closing | 16,293 | 0 | ||||

Table (57)

13.

Prepare a post-closing trial balance for Company BO as at July 31, 20--.

Explanation of Solution

Post-closing trial balance: Post-closing trial balance is a summary of all the asset, liability, and capital accounts and their balances, after the closing entries are prepared. So, post-closing trial balance reports the balances of permanent accounts only.

Prepare a post-closing trial balance for Company BO as at July 31, 20--.

| Company BO | ||

| Post-Closing Trial Balance | ||

| July 31, 20-- | ||

| Account Names | Debit ($) | Credit ($) |

| Cash | $13,780 | |

| Accounts Receivables | 234 | |

| Prepaid Insurance | 11,220 | |

| Land | 292,000 | |

| Building | 96,200 | |

| Accumulated Depreciation, Equipment | $480 | |

| Pool/Slide Facility | 150,505 | |

| Accumulated Depreciation, Pool/Slide Facility | 675 | |

| Pool Furniture | 5,675 | |

| Accumulated Depreciation, Pool Furniture | 220 | |

| Accounts Payable | 2,836 | |

| Wages Payable | 920 | |

| Mortgage Payable | 418,890 | |

| LJ, Capital | 145,593 | |

| $569,614 | $569,614 | |

Table (58)

Want to see more full solutions like this?

Chapter 5 Solutions

College Accounting: A Career Approach (with Quickbooks Online), Loose-leaf Version

Additional Business Textbook Solutions

Principles of Accounting Volume 1

Fundamentals Of Cost Accounting (6th Edition)

Financial Accounting: Information for Decisions

Financial Accounting

Managerial Accounting (4th Edition)

Auditing and Assurance Services (16th Edition)

- The general ledger of Jay Consulting shows the following balances at July 31: Jay has asked you to develop a worksheet that will serve as a trial balance (file name PTB). Use the data provided as input for your model. Review the Model-Building Problem Checklist on page 154 to ensure that your worksheet is complete. Print the worksheet when done. Check figure: Total debits, 17,731. To test your model, use the following balances at August 31: Print the worksheet when done. Check figure: Total debits, 18,810. CHART (optional) Using the test data worksheet, prepare a pie chart showing the percentage of each asset to total assets. Print the chart when done.arrow_forwardA table of data for a library is shown in the table. Normalize these data into the third normal form, preparing it for use in a relational database environment. The library’s computer is programmed to compute the due date to be 14 days after the checkout date. Document the steps necessary to normalize the data similar to the procedures found in the chapter. Index any fields necessary and show how the databases are related.arrow_forwardyou will find an article in a scholarly journal dealing with items from the reading of chapters 1 to 4 in the textbook. Topics may include Accounting Information Systems, Enterprise Systems, E-business, and understanding how accounting information systems works. Then, you will write a summary on this article, The student will post one thread of at least 1000 - 2000 wordsarrow_forward

- Be creative. You are a financial accountant for a small business and have been tasked with preparing a monograph for the company's financial statements. The monograph should include a list of economic events that have occurred over the course of one month, including: 1) receivables, 2) merchandising assets, 3) sales, 4) VAT, 5) prepaid expenses and revenues (these five categories have to be in your monograph as mandatory). Your list should include 15 economic events. For each economic event, you will need to create a general journal entry, post the entry to the general ledger, prepare a trial balance, and ultimately prepare the company's income statement and balance sheet. To complete this assignment, you will need to: 1. Create a list of at least 15 economic events that have occurred over the course of one month. Make sure to include the mandatory economic events mentioned above and any other important events that you can think of. 2. For each economic event, create a general journal…arrow_forwardWe have focused mainly on the financial statements and ratios this week. You decide to practice what you have learned by preparing your own personal balance sheet and income statement as of last month. What do you think you would be able to infer from your completed statements? Do you think you would appear to be liquid? Would your income statement reflect an adequate balance? How can this analysis help you in terms of spending?arrow_forwardAnswer each of the questions below. Due by Wednesday at 11:59 pm. What are a few of the main advantages of the use of special journals? Now that things are more computerized what happens to the special journal in a computerized accounting system that uses electronic forms? Do you feel that the computerized accounting system will soon take over the need for full time accountants?arrow_forward

- For the purpose of process analysis, which of the following measures would be considered an appropriate flow unit for analyzing the main operation of a local accountingfirm? Instructions: You may select more than one answer.a. Number of accountants working each weekb. Number of tax returns completed each weekc. Number of customers with past-due invoicesd. Number of reams of paper received from suppliersarrow_forward1. Choose three of the following five technologies/techniques and explain why you think it is helpful in accounting analytics based on your lab experience in this course. Use some examples in your explanation. Limit your answer to 500 words in total. A. XBRL B. Tableau C. VLOOKUP function D. Pivot table E. Regressionarrow_forwardYou are a financial accountant for a small business and have been tasked with preparing a monograph for the company's financial statements. The monograph should include a list of economic events that have occurred over the course of one month, including: 1) receivables, 2)merchandising assets, 3)sales, 4)VAT, 5) prepaid expenses and revenues (these five categories have to be in your monograph as mandatory). Your list should include 15 economic events. For each economic event, you will need to create a general journal entry, post the entry to the general ledger, prepare a trial balance, and ultimately prepare the company's income statement and balance sheet. To complete this assignment, you will need to: 1. Create a list of at least 15 economic events that have occurred over the course of one month. Make sure to include the mandatory economic events mentioned above and any other important events that you can think of. 2. For each economic event, create a general journal entry and post…arrow_forward

- You have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance.3.What is the ethical dilemma you face? What are the ethical considerations? Consider your options and responsibilities as assistant controller.4.Identify the key internal and external stakeholders. What are the negative impacts that can happen if you do not follow the instructions of your supervisor?5.What are the…arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning