Videos

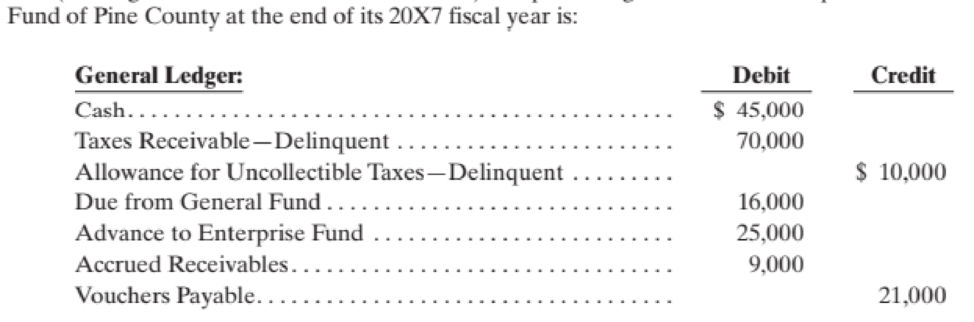

(Closing Entries and Financial Statements) The preclosing

The Advance to Enterprise Fund plus another $15,000 of the fund’s net assets are related to resources set aside for the purposes of the Special Revenue Fund at the discretion of the county’s management. The remainder comes from revenues restricted for the specific purpose for which the fund was established.

- a. Prepare the entry or entries to close the General Ledger and subsidiary ledger accounts at Required the end of the 20X7 fiscal year.

- b. Based on the preclosing trial balance, prepare the following, in good form, for the Pine County Special Revenue Fund:

- 1. A

balance sheet at the end of the 20X7 fiscal year. - 2. A statement of revenues, expenditures, and changes in fund balances for the 20X7 fiscal year.

- 1. A

Want to see the full answer?

Check out a sample textbook solution

Chapter 4 Solutions

Governmental and Nonprofit Accounting (11th Edition)

Additional Business Textbook Solutions

INTERMEDIATE ACCOUNTING

Fundamentals of Cost Accounting

Managerial Accounting

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Advanced Financial Accounting

- The City of Algonquin maintains its books to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: Deferred inflows of resources—property taxes of $73,500 at the end of the previous fiscal year were recognized as property tax revenue in the current year's Statement of Revenues, Expenditures, and Changes in Fund Balance. The City levied property taxes for the current fiscal year in the amount of $13,789,400. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $309,200 is thought to be uncollectible, $365,000 would likely be collected during the 60-day period after the end of the fiscal year, and $52,800 would be collected after that time. The City had recognized the maximum of property taxes allowable under modified accrual accounting. In addition to the expenditures…arrow_forward. A pre-closing trial balance included the following account balances for Simpli City: Due from other funds $ 3,500 Fund balance - unassigned 14,000 Estimated revenues 20,000 Revenues 22,000 Appropriations 18,000 Expenditures - current year 19,000 Expenditures - prior year 1,500 Other Financing Source - Nonreciprocal transfer in 1,000 Required: Prepare the necessary closing entries for the General Fund.arrow_forwardRequired information [The following information applies to the questions displayed below.] The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2024, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Debits Adjustments: $ 29,400 53,000 VILLAGE OF SEASIDE PINES ENTERPRISE FUND Reconciliation of Operating Income to Net Cash Provided by Operating Activities For the year ended December 31, 2024 722,000 98,000 504,000 51,000 17,700 40,900 19,700 $ 1,535,700 Credits $ 112,000 32,600 51,000…arrow_forward

- The City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: 1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance. 2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…arrow_forwardThe City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: 1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance. 2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…arrow_forward4. The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2020, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Debits $32,000 47,000 712,000 89,000 479,000 45,000 17,000 40,000 18,000 $1,479,000 Credits $ 96,000 28,000 45,000 12,000 550,000 4,000 119,000 625,000 $1,479,000 Required: a. Prepare the closing entries for December 31. b. Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ended December 31. c. Prepare the Net Position section of the…arrow_forward

- The Principal City prepared the Trial Balance of the corporate-type fund as of December 31, 20X1. The enterprise fund was established this year through a transfer from the general fund. After having studied the Trial Balance of the company and the required resources of this module: 1.Prepare the fund's closing entries as of December 31, 20X1.2.Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ending December 31.arrow_forwardActivities of a county recreation center are reported in an enterprise fund. During 2019, $5,000,000 is spent on equipment and bonds are issued for $3,000,000. How are these two transactions reported on the enterprise fund’s operating statement? a. No effect b. Revenues, $3,000,000; expenditures, $5,000,000 c. Other financing sources, $3,000,000 d. Other financing sources, $3,000,000; expenditures, $5,000,000arrow_forwardThe City of Jonesboro engaged in the following transactions during the fiscal year ended September 30, 2018. Record the following transactions related to interfund transfers. Be sure to indicate in which fund the entry is being made. a. The city transferred $400,000 from the general fund to a debt service fund to make the interest payments due during the fiscal year. The payments due during the fiscal year were paid. The city also transferred $200,000 from the general fund to a debt service fund to advance-fund the $200,000 interest payment due October 15, 2019. b. The city transferred $75,000 from the Air Operations Special Revenue Fund to the general fund to close out the operations of that fund. c. The city transferred $150,000 from the general fund to the city’s Electric Utility Enterprise Fund to pay for the utilities used by the general and administrative offices during the year. d. The city transferred the required pension contribution of $2 million from the general fund to the…arrow_forward

- Prepare entries in general journal form to record the following transactions in the Roadway Fund general ledger accounts for City of Kettering for the fiscal year 2018. Use modified accrual accounting. At the beginning of the fiscal year, the fund $1,360,000 was offset by the assigned fund balance in the same amount. The city was awarded $4,200,000 for road inspections and repairs during the year. The award requires reimbursement for expenditures, not an allotment upfront. Work contracted for the year amounted to $4,175,000. Invoices received for the work performed totaled $4,150,000. $3,980,000 of that amount was paid in cash as of year-end. The state reimbursed the city $4,000,000 for the completed work before year-end. Prepare a statement of Revenues, Expenditures, and Changes in Fund Balance for the Roadway Fund.arrow_forwardThe City of Grinders Switch Maintains its books in a manner that facilitates the preparation of fund accounting statements and uses worksheet adjustments to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations. General fixed assets as of the beginning of the year, which had not recorded, were as follows: Land $ 7,554,000 Buildings $33,355,000 Improvements Other Than Buildings $14,820,000 Equipment $11,690,000 Accumulated Depreciation, Capital Assets $25,800,000 2. During the year, expenditures for Capital outlays amounted to $7,500,000. Of that amount $4,800,000 was for buildings; the remainder was for improvements other than buildings. 3. The Capital…arrow_forwardAssume that the County of Katerah maintains its books and records in a manner that facilitates preparation of the fund financial statements. The county formally integrates the budget into the accounting system and uses the encumbrance system. All appropriations lapse at year-end. At the beginning of the fiscal year, the county had the following balances in its accounts. All amounts are in thousands. Prepare the necessary entries for the current fiscal year. Cash $200 Fund balance unassigned 50 Reserve for encumbrances (committed or assigned) 150 (a) The county made the appropriate entry to restore the prior-year purchase commitments. (b) The county board approved a budget with revenues estimated to be $800 and expenditures of $750. (c) The county received the items that had been ordered in the prior year at an actual cost of $135. (d) The county ordered supplies at an estimated cost of $50 and equipment at an estimated cost of $70. (e) The county incurred salaries and other operating…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education