Concept explainers

Videos

Consolidated

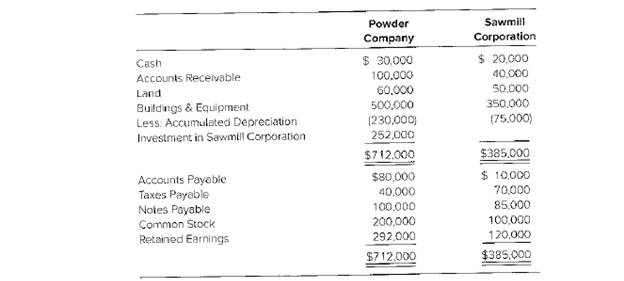

Powder Company spent $240,000 to acquire all of Sawmill Corporation’s stock on January 1,20X2. The balance sheets of the two companies on December 31, 20X3, showed the following amounts:

Sawmill reported retained earnings of $100,000 at the date of acquisition. The difference between the acquisition price and underlying book value is assigned to buildings and equipmentwith a remaining economic life of 10 years from the date of acquisition. Assume Sawmill’s

Required

a. Give the appropriate consolidation entry or entries needed to prepare a consolidated balancesheet as of December 31, 20X3.

b. Prepare a consolidated balance sheet worksheet as of December 31, 20X3.

Want to see the full answer?

Check out a sample textbook solution

Chapter 4 Solutions

Advanced Financial Accounting

- ABC Corporation acquired 70 percent of XYZ Corporation on August 1 for P420,000. On that date, XYZ Corporation had the following book values and market values. What is the amount of purchase differential recognized on the acquisition date consolidated balance sheet with respect to plant assets. *In good accounting form, please. Thank you!arrow_forwardConstructing the Consolidated Balance Sheet at Acquisition On January 1 of the current year, Healy Company purchased all of the common shares of Miller Company for $500,000 cash. Balance sheets of the two firms immediately after the acquisition follow: During purchase negotiations, Miller's plant assets were appraised at $425,000 and all of its remaining assets and liabilities were appraised at values approximating their book values. Healy also concluded that an additional $85,000 (for goodwill) demanded by Miller's shareholders was warranted because Miller's earning power was better than the industry average. Prepare the consolidating adjustments and the consolidated balance sheet at acquisition. Use negative signs with consolidating adjustment answers, when appropriate. Current assets Investment in Miller Healy Miller Consolidating Consolidated Company Company Adjustments Balance Sheet $1,400,000 $80,000 $ 500,000 3,000,000 410,000 Plant assets, net Goodwill Total assets $4,900,000…arrow_forwardPutin Company acquired the assets and assumed the liabilities of Joni Company on January 1, 2018, paying OMR 4,500,000 cash. Immediately prior to the acquisition, Joni Company's balance sheet was as follows: BOOK VALUE FAIR VALUE Accounts receivable 240,000 220,000 Inventory 290,000 320,000 Land 960,000 1,508,000 Buildings 1,020,000 1,392,000 Total 2,510,000 3,440,000 Accounts payable 270,000 270,000 Note payable 600,000 600,000 Common stock, $5 par 420,000 Other contributed capital…arrow_forward

- Professor Corporation acquired 70 percent of Scholar Corporation's common stock on December 31, 20X4, for $102,200. The fair value of the noncontrolling interest at that date was determined to be $43,800. Data from the balance sheets of the two companies included the following amounts as of the date of acquisition: Item Cash Accounts Receivable Inventory Land Buildings & Equipment Less: Accumulated Depreciation Investment in Scholar Corporation Total Assets Accounts Payable Mortgage Payable Common Stock Retained Earnings Total Liabilities & Stockholders' Equity Assets Cash Professor Scholar Corporation Corporation $50,300 Accounts receivable Inventory Land Buildings and equipment Less: Accumulated depreciation Investment in Scholar Corporation Total Assets Liabilities & Equity Accounts payable Mortgage payable Common stock Retained earnings NCI in Net assets of Scholar Corporation Total Liabilities & Equity 90,000 130,000 60,000 410,000 (150,000) 102,200 $ 692,500 $152,500 250,000…arrow_forwardProfessor Corporation acquired 70 percent of Scholar Corporation's common stock on December 31, 20X4, fr $102,200. The fair value of the noncontrolling interest at that date was determined to be $43,800. Data from the balance sheets of the two companies Included the following amounts as of the date of acquisition: Item Cash Accounts Receivable Inventory Land Buildings & Equipment Less: Accumulated Depreciation. Investment in Scholar Corporation Total Assets Accounts Payable Mortgage Payable Common Stock Retained Earnings Total Liabilities & Stockholders' Equity Professor Corporation $ 50,300 90,000 Scholar Corporation $21,000 44,000 130,000 75,000 60,000 30,000 410,000 250,000 (150,000) (80,000) 102,200 $ 692,500 $340,000 $ 152,500 $ 35,000 250,000 180,000 80,000 40,000 210,000 85,000 $ 692,500 $340,000 At the date of the business combination, the book values of Scholar's assets and liabilities approximated fair value except for Inventory, which had a fair value of $81,000, and…arrow_forwardOn December 31, Year 1, P Company obtains control over the net assets of S Company by purchasing 100% of the ordinary shares of S Company. P Company paid for the purchase by issuing ordinary shares with a fair value of $44,000. In addition, P Company paid $1,000 for professional fees to facilitate the transaction. The following information has been assembled just prior to the acquisition date: Show Transcribed Text Goodwill Plant assets (net) Current assets Shareholders' equity Long-term debt Current liabilities Show Transcribed Text (i) the acquisition method (ii) the new-entity method Carrying Amount $ 80,000 50.000 $130,000 $ 75,000 25,000 30.000 3 $130,000 ü P Company 3 Fair Value $ 38,000 90,000 55,000 $ 183,000 $ 29,000 30,000 Carrying Amount $ 20.000 15,000 $35.000 $18,000 7,000 10,000 S Company $35,000 Fair Value $ 22,000 26,000 14.000 $ 62,000 $ 8,000 10,000 Required (a) Prepare a consolidated statement of financial position for P Company and calculate the debt-to-equity ratio…arrow_forward

- Arizona Corporation acquired the business Data Systems for $310,000 cash and assumed all liabilities at the date of purchase. Data's books showed tangible assets of $320,000, liabilities of $17,000, and stockholders' equity of $303,000. An appraiser assessed the fair market value of the tangible assets at $300,000 and liabilities at $17,000 at the date of acquisition. Arizona Corporation's financial condition just prior to the acquisition is shown in the following statements model. Balance Income Sheet Statement Assets Cash = + Liabilities + Tangible Assets ΝΑ + Stockholders Equity Goodwill Revenue Expenses = + ΝΑ = ΝΑ + Net Income 520,000 + Required 1.Compute the amount of goodwill acquired. 2.Record the acquisition in a financial statements model. Arizona Corporation's financial condition just prior to the acquisition is shown in the financial statements model. 3.Record the acquisition in general journal format. 520,000 NA Statement of Cash Flows ΝΑ = ΝΑ ΝΑarrow_forwardOn January 1, Year 1, Big Corporation acquired 40% interest in Small Company for $300,000. At the date of acquisition, Small Company's equity (net assets) had a book value of $550,000 and a fair value of $600,000. The difference between the book value and the fair value relates to equipment being depreciated over the remaining useful life of 10 years. During Year 1, Small Company had net income of $900,000 and paid a $40,000 dividend. Required: 1. Prepare the journal entries required in year 1 to account for the investment in Small Company. 2. Compute the asset fair value difference and goodwillarrow_forwardGIGİ Group completed an acquisition of an interest in another business, Venice Company, during the year and paid $300,000 in purchasing 25% interests in Venice. At the acquisition date, the acquisition-date fair value of the net assets of Venice was $800,000 while the net assets of Venice in the financial statements amounted to $600,000. At financial year end of GiGi, the net assets of Venice increased to $700,000. Determine the carrying amount of the investment in Venice at financial year end. Select one: a. $200,000 b. $275,000 c. $175,000 d. $325,000arrow_forward

- On January 1, 20X1 P Co acquired 70% ownership of S Ltd. On the acquisition date all identifiable assets and liabilities had book values equal to fair values. P uses the cost method to record its investment in S. For external reporting purposes consolidated statements are required. However, the purchase did result in the acquisition of goodwill of $55,000. During the past few years, a number of transactions have taken place: Inter-company downstream sales during 20X5 were 120,000. An unrealized profit of 17,000 still remains in the unsold ending inventory. The beginning inventory included an unrealized profit of 11,000 related to last year’s downstream inter-company sales. Inter-company upstream sales during 20X5 were 70,000. An unrealized profit of 8,000 remains in the unsold ending inventory. There were no inter-company upstream sales last year. On January 3, 20X3, P sold equipment to S for 88,000. The equipment had a net book value of $60,000 and a remaining useful life of 10…arrow_forwardDuring the current year, Brewer Company acquired all of the outstanding common stock of Miller Inc. paying $11,900,000 cash. The book values and fair values of Miller's assets and liabilities acquired are listed below: Book Value Fair Value Accounts receivable $ 1,750,000 $ 1,575,000 Inventories 2,600,000 3,900,000 Property, plant, and equipment 8,900,000 11,525,000 Accounts payable 2,900,000 2,900,000 Bonds payable 4,400,000 4,025,000 Prepare the journal entry to record the acquisition by Brewer Company.arrow_forwardPirate Corporation acquired 60 percent ownership of Ship Company on January 1, 20X8, at underlying book value. At that date, the fair value of the noncontrolling interest was equal to 40 percent of the book value of Ship Company. Accumulated depreciation on Buildings and Equipment was $75,000 on the acquisition date. Trial balance data at December 31, 20X8, for Pirate and Ship are as follows: Item Pirate Corporation Ship Company Debit Credit Debit Credit Cash $ 27,000 $8,000 Accounts Receivable 65,000 22,000 Inventory 40,000 30,000 Buildings and Equipment 500,000 235,000 Investment in Row Company 40,000 Investment in Ship Company 108,000 Cost of Goods Sold 150,000 110,000 Depreciation Expense 30,000 10,000 Interest Expense 8,000 3,000 Dividends Declared 24,000 15,000 Accumulated Depreciation $ 140,000 $ 85,000 Accounts Payable 63,000 20,000 Bonds Payable 100,000 50,000 Common Stock 200,000…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education