Concept explainers

Videos

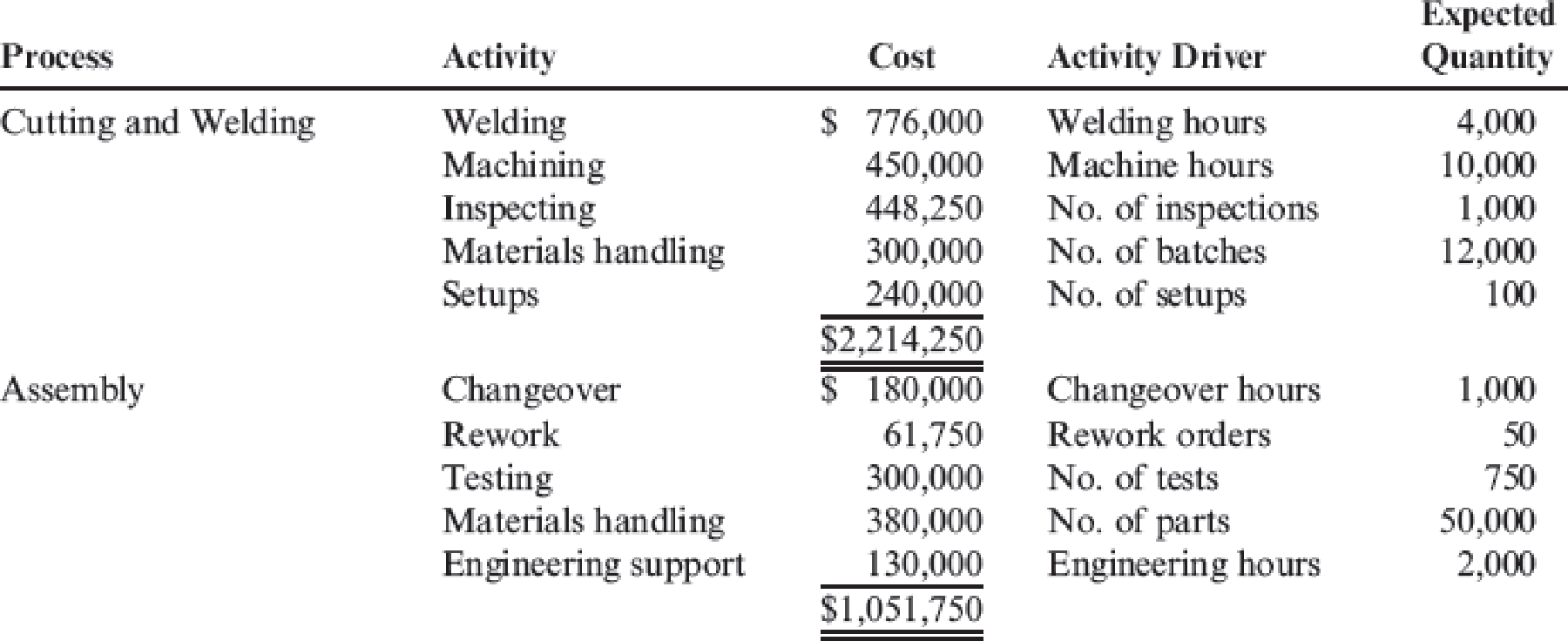

Reducir, Inc., produces two different types of hydraulic cylinders. Reducir produces a major subassembly for the cylinders in the Cutting and Welding Department. Other parts and the subassembly are then assembled in the Assembly Department. The activities, expected costs, and drivers associated with these two manufacturing processes are given below.

Note: In the assembly process, the materials-handling activity is a function of product characteristics rather than batch activity.

Other

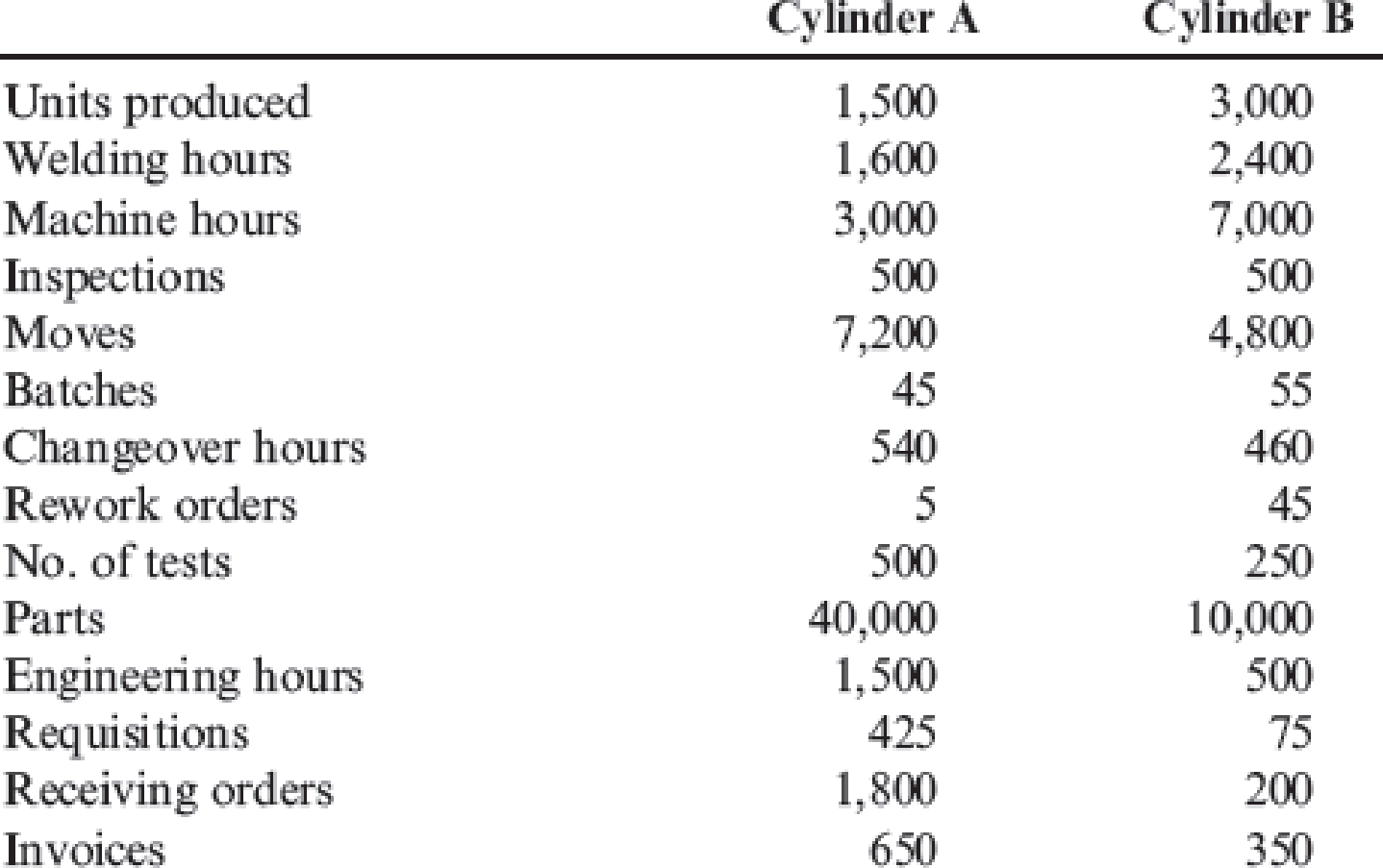

Other production information concerning the two hydraulic cylinders is also provided:

Required:

- 1. Using a plantwide rate based on machine hours, calculate the total overhead cost assigned to each product and the unit overhead cost.

- 2. Using activity rates, calculate the total overhead cost assigned to each product and the unit overhead cost. Comment on the accuracy of the plantwide rate.

- 3. Calculate the global consumption ratios.

- 4. Calculate the consumption ratios for welding and materials handling (Assembly) and show that two drivers, welding hours and number of parts, can be used to achieve the same ABC product costs calculated in Requirement 2. Explain the value of this simplification.

- 5. Calculate the consumption ratios for inspection and engineering, and show that the drivers for these two activities also duplicate the ABC product costs calculated in Requirement 2.

1.

Compute the total overhead cost assigned to each product and the unit overhead cost using a plantwide rate based on machine hours for incorporation R.

Explanation of Solution

Plantwide overhead rate: Plantwide overhead rate is the rate a company uses to allocate its manufacturing overhead costs to products and cost centres.

Step 1: Calculate plantwide overhead rate based on machine hours.

Step 2: Determine the total overhead cost assigned to each product and the unit overhead cost.

For cylinder A,

Therefore, the total overhead cost assigned and unit overhead cost for cylinder A is $1,200,000 and $800 respectively.

For cylinder B,

Therefore, the total overhead cost assigned and unit overhead cost for cylinder B is $2,800,000 and $933.33 respectively.

2.

Determine the total overhead cost assigned to each product and the unit overhead cost using an activity rate for incorporation R and provide comment on the accuracy of the plantwide rate.

Explanation of Solution

Activity rates: Activity rates are calculated by dividing the budgeted activity costs by the amount of activity output as measured by the activity driver.

Step 1: Calculate activity rates.

| Particulars | |

| Cost of welding | $ 776,000 |

| Divide: Welding hours | 4,000 hours |

| Activity rate | $194.00 per welding hour |

| Cost of machining | $ 450,000 |

| Divide: Machine hours | 10,000 hours |

| Activity rate | $45.00 per machine hour |

| Cost of inspecting | $ 448,250 |

| Divide: Number of inspections | 1,000 inspections |

| Activity rate | $448.25 per inspection |

| Cost of materials handling | $ 300,000 |

| Divide: Number of batches | 12,000 |

| Activity rate | $25.00 per move |

| Cost of setups | $ 240,000 |

| Divide: Number of setups | 100 |

| Activity rate | $2,400.00 per batch |

| Cost of changeover | $ 180,000 |

| Divide: change over hours | 1,000 change over hours |

| Activity rate | $180.00 per changeover hour |

| Cost of rework | $ 61,750 |

| Divide: Rework orders | 50 rework orders |

| Activity rate | $1,235.00 per rework order |

| Cost of testing | $ 300,000 |

| Divide: Number of tests | 750 tests |

| Activity rate | $400.00 per test |

| Cost of materials handling | $ 380,000 |

| Divide: Number of parts | 50,000 parts |

| Activity rate | $7.60 per part |

| Cost of engineering support | $ 130,000 |

| Divide: Engineering hours | 2,000 hours |

| Activity rate | $65.00 per engineering hour |

| Cost of purchasing | $ 135,000 |

| Divide: Purchase requisitions | 500 requisitions |

| Activity rate | $270.00 per requisition |

| Cost of receiving | $ 274,000 |

| Divide: Receiving orders | 2,000 receiving orders |

| Activity rate | $137.00 per receiving order |

| Cost of paying suppliers | $ 225,000 |

| Divide: Number of invoices | 1,000 invoices |

| Activity rate | $225.00 per invoice |

| Cost of providing space and utilities | $ 100,000 |

| Divide: Machine hours | 10,000 machine hours |

| Activity rate | $10.00 per machine hour |

Table (1)

Step 2: calculate the total overhead cost assigned to each product.

| Particulars | Cylinder A ($) | Cylinder B ($) |

| Welding | ||

| Activity rate × welding hours | ||

| $194 × 1,600 welding hours | $ 310,400 | |

| $194 × 2,400 welding hours | $ 465,600 | |

| Machining | ||

| Activity rate × machine hours | ||

| $45 × 3,000 machine hours | $ 135,000 | |

| $45 * 7,000 machine hours | $ 315,000 | |

| Inspecting | ||

| Activity rate × number of inspections | ||

| $448.25 × 500 inspections | $ 224,125 | |

| $448.25 × 500 inspections | $ 224,125 | |

| Materials handling | ||

| Activity rate × number of moves | ||

| $25 × 7,200 moves | $ 180,000 | |

| $25 × 4,800 moves | $ 120,000 | |

| Setups | ||

| Activity rate × number of batches | ||

| $2,400 × 45 batches | $ 108,000 | |

| $2,400 × 55 batches | $ 132,000 | |

| Change over | ||

| Activity rate × change over hours | ||

| $180 × 540 change over hours | $ 97,200 | |

| $180 × 460 change over hours | $ 82,800 | |

| Rework | ||

| Activity rate × rework orders | ||

| $1,235 × 5 rework orders | $ 6,175 | |

| $1,235 × 45 rework orders | $ 55,575 | |

| Testing | ||

| Activity rate × number of tests | ||

| $400 × 500 tests | $2,00,000 | |

| $400 × 250 tests | $1,00,000 | |

| Materials handling | ||

| Activity rate × number of tests | ||

| $7.60 × 40,000 parts | $ 304,000 | |

| $7.60 × 10,000 parts | $ 76,000 | |

| Engineering support | ||

| Activity rate × Engineering hours | ||

| $65 × 1,500 engineering hours | $ 97,500 | |

| $65 × 500 engineering hours | $ 32,500 | |

| Purchasing | ||

| Activity rate × number of purchase requisitions | ||

| $270 × 425 requisitions | $ 114,750 | |

| $270 × 75 requisitions | $ 20,250 | |

| Receiving | ||

| Activity rate × number of receiving orders | ||

| $137 × 1,800 receiving orders | $ 246,600 | |

| $137 × 200 receiving orders | $ 27,400 | |

| Paying suppliers | ||

| Activity rate × number of invoices | ||

| $225 × 650 invoices | $ 146,250 | |

| $225 × 350 invoices | $ 78,750 | |

| Providing space and utilities | ||

| Activity rate × machine hours | ||

| $10 × 3,000 machine hours | $ 30,000 | |

| $10 × 7,000 machine hours | $ 70,000 | |

| Total overhead costs | $ 2,200,000 | $ 1,800,000 |

| Divide: Units produced | 1,500 units | 3,000 units |

| Overhead per unit | $ 1,467 | $ 600 |

Table (2)

Thus, the overhead per unit for cylinder A and cylinder B is $1,467 and $600 respectively.

The overhead consumption patterns better than the machine hour pattern of the plantwide rate because, Cylinder B is overcosted, and Cylinder A is undercosted. The activity assignments obtain the cause-and-effect relationships.

3.

Compute global consumption ratio.

Explanation of Solution

Global consumption ratio: The global consumption ratio is the proportion of the total activity costs absorbed by a provided product or cost object.

Calculate global consumption ratio:

For Cylinder A:

For Cylinder B:

Therefore, the global consumption ratio for Cylinder A and Cylinder B is 0.55 and 0.45 respectively.

4.

Determine the consumption ratios for materials handling (Assembly) and welding and justify that two drivers, welding hours and several parts, can be used to achieve the same ABC product costs. Explain the value of this simplification.

Explanation of Solution

Overhead consumption ratio: The overhead consumption ratios simply estimate the proportion of each activity used by individual products. The overhead consumption ratio is mainly suitable to allocate the costs of a shared resource.

Compute the consumption ratios for materials handling (Assembly) and welding:

For Welding:

For Material handling (parts):

Set up two equations, where W’s represent the allocation rates:

Multiply second equation by -4:

By solving:

And thus,

Cost pools:

Activity rates:

Assign overhead for the two products:

| Particulars | Cylinder A | Cylinder B |

| Welding | ||

| Activity rate × welding hours | ||

| $625 × 1,600 welding hours | $ 1,000,000 | |

| $625 × 2,400 welding hours | $ 1,500,000 | |

| Material handling | ||

| Activity rate × Number of parts | ||

| $30 × 40,000 parts | $ 1,200,000 | |

| $30 × 10,000 parts | $ 300,000 | |

| Total overhead costs | $ 2,200,000 | $ 1,800,000 |

| Divide: Units produced | 1,500 units | 3,000 units |

| Overhead per unit | $1,467 (rounded) | $ 600 |

Table (3)

We can take a 14-driver system and decrease it to a two-driver system and obtain the same overhead cost assignments as the more complex system. This After-the-fact simplification has two major benefits:

(1) It assists nonfinancial managers to more easily read, understands, and interpret product cost reports

(2) The actual values only need to be obtained for two drivers instead of 14, producing considerable cost savings.

5.

Ascertain the consumption ratios for inspection and engineering, and prove that the drivers for these two activities also duplicate the ABC product costs.

Explanation of Solution

Compute the consumption ratios for inspection and engineering:

Construct two equations (w’s represent the allocation rates):

Subtract the second equation from the first:

And thus,

Cost pools:

Calculate the activity rates:

Therefore, the activity rate for inspection and engineering is $3,200 per inspection and $400 per hour respectively.

Assign the overhead for cylinder A and cylinder B:

| Particulars | Cylinder A | Cylinder B |

| Inspection | ||

| Activity rate × Number of inspections | ||

| $3,200 × 500 inspections | $ 1,600,000 | |

| $3,200 × 500inspections | $ 1,600,000 | |

| Engineering | ||

| Activity rate × Engineering hours | ||

| $400 × 1,500 engineering hours | $ 600,000 | |

| $400 × 500 engineering hours | $ 200,000 | |

| Total overhead costs | $ 2,200,000 | $ 1,800,000 |

| Divide: Units produced | 1,500 units | 3,000 units |

| Overhead per unit | $1,467.67 (rounded) | $ 600.00 |

Thus, the overhead per unit for Cylinder A and Cylinder B is $1,467.67 and $600 respectively.

Want to see more full solutions like this?

Chapter 4 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Lacy, Inc., produces a subassembly used in the production of hydraulic cylinders. The subassemblies are produced in three departments: Plate Cutting, Rod Cutting, and Welding. Materials are added at the beginning of the process. Overhead is applied using the following drivers and activity rates: Other data for the Plate Cutting Department are as follows: Required: 1. Prepare a physical flow schedule. 2. Calculate equivalent units of production for: a. Direct materials b. Conversion costs 3. Calculate unit costs for: a. Direct materials b. Conversion costs c. Total manufacturing 4. Provide the following information: a. The total cost of units transferred out b. The journal entry for transferring costs from Plate Cutting to Welding c. The cost assigned to units in ending inventoryarrow_forwardLarsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forwardWojtek Nakowski has prepared the following list of statements about process cost accounting. Identify each statement as true or false. 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. Process cost systems are used to apply costs to similar products that are mass-produced in a continuous fashion. A process cost system is used when each finished unit is indistinguishable from another. Companies that produce soft drinks, motion pictures, and computer chips would all use process cost accounting. In a process cost system, costs are tracked by individual jobs. Job-order costing and process costing track different manufacturing cost components. Both job-order costing and process costing account for direct materials, direct labour, and manufacturing overhead. Costs flow through the accounts in the same basic way for both job-order costing and process costing. In a process cost system, only one work in process inventory account is used. In a process cost system, costs are summarized in a job cost sheet. In a…arrow_forward

- Perez Industries produces two electronic decoders, P and Q. Decoder P is more sophisticated and requires more programming and testing than does Decoder Q. Because of these product differences, the company wants to use activity-based costing to allocate overhead costs. It has identified four activity pools. Relevant information follows: b. Determine the overhead cost allocated to each product.arrow_forwardIn highly automated manufacturing, the most appropriate base for factory overhead application is: a. machine hours b. physical output c. direct materials cost d. direct labor hoursarrow_forwardGladden Dock Company manufactures boat docks on an assembly line. Its costing system uses two cost categories, direct materials and conversion costs. Each product must pass through the Assembly Department and the Finishing Department. This problem focuses on the Assembly Department. Direct materials are added at the beginning of the production process. Conversion costs are allocated evenly throughout production. The firm uses FIFO method and the controller prepared the following (correct) equivalent unit calculation. Unitscompleted Physical Units Direct Materials Conversion WIP, beginning 70 0 52.5 Started and completed 30 30 30 WIP, ending 10 10 5 Totals 110 40 87.5 Cost per Equiv Unit $4,000 $16,000 Work in process, beginning inventory: Current Costs:Direct materials $140,000 Direct materials $ 160,000Conversion costs $260,000 Conversion…arrow_forward

- In a manufacturing company, overhead allocations are made for three reasons: (1) to determine the full cost of a product; (2) to encourage efficient resource usage; and (3) to compare alternative courses of action for management purposes. 1. Why must overhead be considered a product cost under generally accepted accounting principles? 2. Ayam Company makes plastic dog carriers. The manufacturing process is highly automated and the machine time needed to make any size crate is approximately the same. Ayam’s management decides to begin producing plastic lawn furniture and, to do so, two additional pieces of automated equipment are acquired. Annual depreciation on the new pieces of equipment is P38,000. Should the new overhead cost be allocated over all products manufactured by Ayam? Explain.arrow_forwardNobel Ltd adopts process costing rather than job costing. Which of the following statement could explain why? a. Nobel Ltd produces units according to customer specifications. b. Nobel Ltd wants to track the cost of material, labour and overhead to specific customers. c. Nobel Ltd wants to assign overhead using machine hours as the allocation base. d. Nobel Ltd manufactures virtually identical products using a series of continuous processes.arrow_forwardZwahlen Corporation has an activity-based costing system with three activity cost pools-Processing, Setting Up, and Other. Costs in the Processing cost pool are assigned to products based on machine-hours (MHS) and costs in the Setting Up cost pool are assigned to products based on the number of batches. Costs in the Other cost pool are not assigned to products. Data concerning the two products and the company's costs and activity-based costing system appear below: Activity Cost Pools Processing Setting Up Other Product D7 Product HO Total Sales (total) Direct materials (total) Direct labor (total) $ 59,800 $ 18,700 $ 30,500 MHS 10,000 14,000 24,000 Batches 1,200 1,800 3,000 Activity Rate per MH per batch Product D7 $225,300 $ 74,600 $ 106,600 Product HO $ 311,100 $ 147,200 $ 98,200 Required: a. Calculate activity rates for each activity cost pool using activity-based costing. b. Determine the amount of overhead cost that would be assigned to each product using activity-based costing.…arrow_forward

- Unit-based product costing assigns direct labor, direct materials, and overhead to products. Direct materials and direct labor are assigned using direct tracing. Assignment of overhead costs, however, relies on driver tracing and perhaps allocation. Unit-based costing first assigns overhead costs to a functional unit, creating plant or departmental cost pools. Next these pooled costs are assigned to products using predetermined overhead rates based on unit-level drivers. Unit-level drivers measure the demands placed on ........?.......Unit-level activities are those that are performed each and every time:......?........ . From the dropdown below, select all unit-level drivers:.........?........... Goodmark Company produces two products: scented and regular birthday cards. Goodmark uses a plantwide rate based on direct labor hours. The estimated and actual data for the coming year are provided below: estimated overhead $720,000 Expected activity(direct labor hours) 180,000 actual…arrow_forwardAresco Corporation manufactures two products: Product G51B and Product E48X. The company uses a plantwide overhead rate based on direct labor-hours. It is considering implementing an activity-based costing (ABC) system that allocates all of its manufacturing overhead to four cost pools. The following additional information is available for the company as a whole and for Products G51B and E48X. Activity Cost Pool Machining Machine setups Product design Order size Activity Measure Machine-hours Number of setups Number of products Direct labor-hours Activity Measure Machine-hours Number of setups Number of products Direct labor-hours Product G51B 2,180 252 1 3,180 Total Cost $ 104,500 $ 304,500 $ 84,500 $ 381,500 Product E48X 2,820 248 1 6,820 Total Activity 5,000 MHS 500 setups 2 products 10,000 DLHS Required: a. Using the plantwide overhead rate, what percentage of the total overhead cost is allocated to Product G51B? b. Using the plantwide overhead rate, what percentage of the total…arrow_forwardIf Power Products uses process costing, which of the follow-ing are likely to be true: a. The production processes are high volume.b. The products use different amounts of direct labor.c. The products are created with repetitive processes.d. The products are created to customer specifications.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning