Concept explainers

Videos

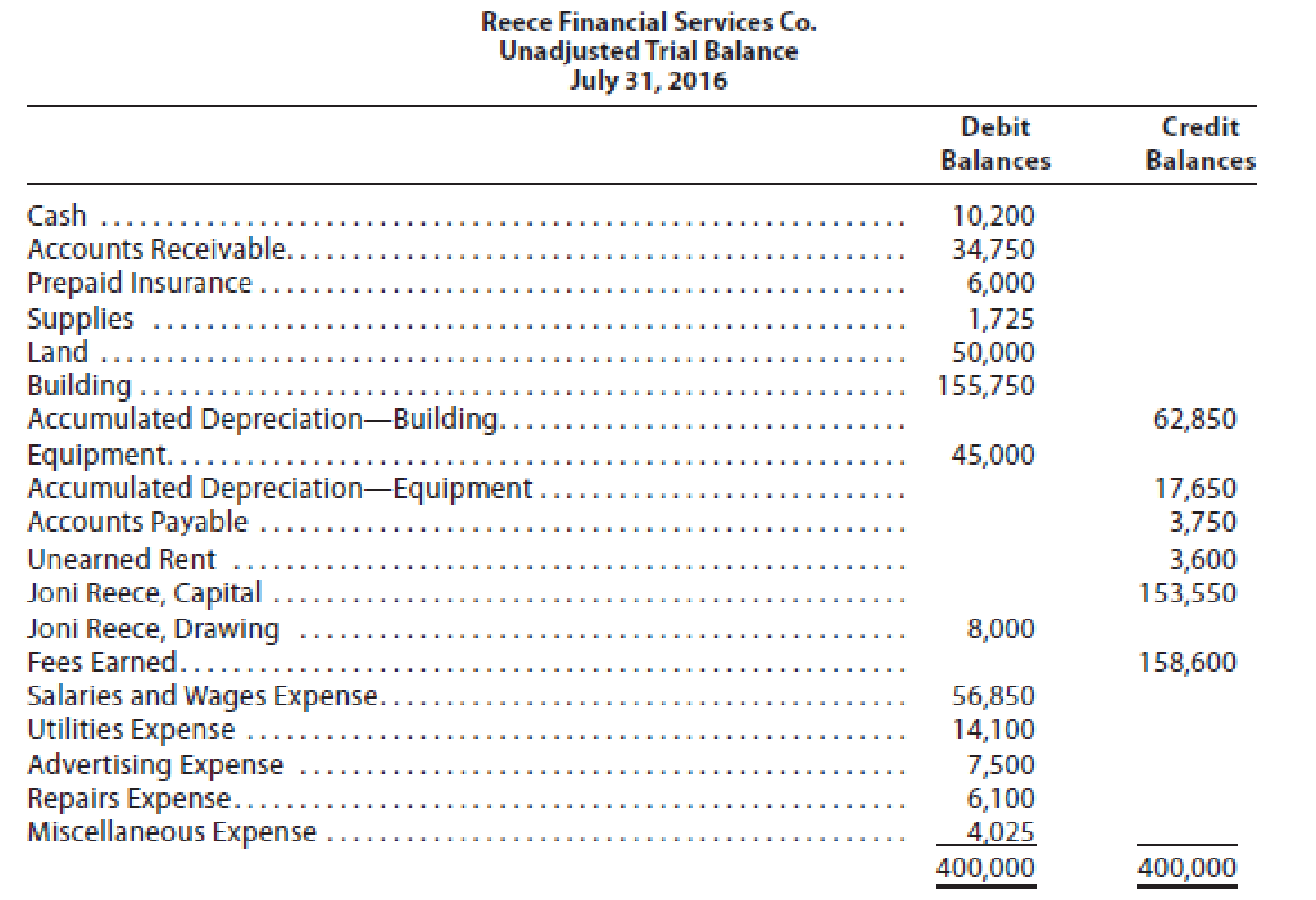

Reece Financial Services Co., which specializes in appliance repair services, is owned and operated by Joni Reece. Reece Financial Services Co.’s accounting clerk prepared the following unadjusted

The data needed to determine year-end adjustments are as follows:

- a.

Depreciation of building for the year, $6,400. - b. Depreciation of equipment for the year, $2,800.

- c. Accrued salaries and wages at July 31, $900.

- d. Unexpired insurance at July 31, $1,500.

- e. Fees earned but unbilled on July 31, $10,200.

- f. Supplies on hand at July 31, $615.

- g. Rent unearned at July 31, $300.

Instructions

- 1. Journalize the

adjusting entries using the following additional accounts: Salaries and Wages Payable; Rent Revenue; Insurance Expense; Depreciation Expense—Building; Depreciation Expense—Equipment; and Supplies Expense. - 2. Determine the balances of the accounts affected by the adjusting entries and preparean adjusted trial balance.

(1)

Record the adjusting entries on July 31, 2016 of Company RFS.

Explanation of Solution

Adjusting Entries

Adjusting entries indicates those entries, which are passed in the books of accounts at the end of one accounting period. These entries are passed in the books of accounts as per the revenue recognition principle and the expenses recognition principle to adjust the revenue, and the expenses of a business in the period of their occurrence.

Rule of Debit and Credit:

Debit - Increase in all assets, expenses & dividends, and decrease in all liabilities and stockholders’ equity.

Credit - Increase in all liabilities and stockholders’ equity, and decrease in all assets & expenses.

The adjusting entries of Company RFS are as follows:

Depreciation expense-Building

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| 2016 | Depreciation expense | 6,400 | |

| July, 31 | Accumulated Depreciation- building | 6,400 | |

| (To record the depreciation on building for the current year.) |

Table (1)

The impact on the accounting equation for the above referred adjusting entry is as follows:

- Depreciation expense is component of stockholders’ equity and decreased it, so debit depreciation expense by $6,400.

- Accumulated depreciation is a contra asset account, and it decreases the asset value by $6,400. So credit accumulated depreciation by $6,400.

Depreciation expense-Equipment

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| 2016 | Depreciation expense | 2,800 | |

| July, 31 | Accumulated Depreciation- equipment | 2,800 | |

| (To record the depreciation on equipment for the current year.) |

Table (2)

The impact on the accounting equation for the above referred adjusting entry is as follows:

- Depreciation expense is component of stockholders’ equity and decreased it, so debit depreciation expense by $2,800.

- Accumulated depreciation is a contra asset account, and it decreases the asset value by $2,800. So credit accumulated depreciation by $2,800.

Salary and wages expense:

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| 2016 | Salary and wages expense | 900 | |

| July, 31 | Wages Payable | 900 | |

| (To record the salary and wages accrued but not paid at the end of the accounting period.) |

Table (3)

The impact on the accounting equation for the above referred adjusting entry is as follows:

- Salary and wages expense is a component of Stockholders ‘equity, and it decreased it by $900. So debit wage expense by $900.

- Salary and wages payable is a liability, and it is increased by $900. So credit Salary and wages payable by $900.

Unexpired insurance:

| Date | Description |

Post. Ref |

Debit ($) |

Credit ($) |

| 2016 | Insurance expense (1) | 4,500 | ||

| July 31 | Prepaid insurance | 4,500 | ||

| (To record the insurance expense incurred at the end of the year) |

Table (4)

The impact on the accounting equation for the above referred adjusting entry is as follows:

Working note (1):

Calculate the value of insurance expense at the end of the year.

- Insurance expense is a component of owners’ equity, and decreased it by $4,500 hence debit the insurance expense for $4,500.

- Prepaid insurance is an asset, and it decreases the value of asset by $4,500, hence credit the prepaid insurance for $4,500.

Accrued fees unearned on July 31

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| 2016 | Accounts Receivable | 10,200 | |

| July 31 | Fees earned | 10,200 | |

| (To record the accounts receivable at the end of the year.) |

Table (5)

The impact on the accounting equation for the above referred adjusting entry is as follows:

- Accounts Receivable is an asset, and it is increased by $10,200. So debit Accounts receivable by $10,200.

- Fees earned are component of stockholders’ equity, and it increased it by $10,200. So credit fees earned by $10,200.

Supplies expenses on July 31

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| 2016 | Supplies Expense (2) | 1,110 | |

| July 31 | Supplies | 1,110 | |

| (To record the supplies expense at the end of the accounting period) |

Table (6)

The impact on the accounting equation for the above referred adjusting entry is as follows:

- Supplies expense is a component of stockholders’ equity, and it decreased the stockholders’ equity by $1,110. So debit supplies expense by $1,110.

- Supplies are an asset for the business, and it is decreased by $1,110. So credit supplies by $1,110.

Working Note (2):

Calculate Supplies expense for the accounting period.

Unearned Rent on July 31:

| Date | Account Titles and Explanation | Debit ($) | Credit ($) |

| 2016 | Unearned Rent | 3,300 | |

| July 31 | Rent revenue (3) | 3,300 | |

| (To record the Rent revenue from services at the end of the accounting period.) |

Table (7)

The impact on the accounting equation for the above referred adjusting entry is as follows:

- Unearned Rent is a liability, and it is decreased by $3,300. So debit unearned rent by $3,300.

- Rent revenue is a component of Stockholders’ equity, and it is increased by $3,300. So credit rent revenue by $3,300.

Working Note (3):

Calculation of Rent Revenue for the accounting period

(2)

Prepare the adjusted trial balance of the Company RFS on July 31, 2016.

Explanation of Solution

Adjusted Trial Balance

Adjusted trial balance is a trial balance prepared at the end of a financial period, after all the adjusting entries are journalized and posted. It is prepared to prove the equality of the total debit and credit balances.

The adjusted trial balance of the Company RFS is as follows:

| Company RFS | ||

| Trial Balance after Adjustments | ||

| July 31, 2016 | ||

| Particulars | Debit $ | Credit $ |

| Cash | 10,200 | |

| Accounts Receivable(8) | 44,950 | |

| Prepaid Insurance | 1,500 | |

| Supplies | 615 | |

| Land | 50,000 | |

| Building | 155,750 | |

| Accumulated Depreciation - Building(4) | 69,250 | |

| Equipment | 45,000 | |

| Accumulated Depreciation - Equipment(5) | 20,450 | |

| Accounts Payable | 3,750 | |

| Unearned Rent | 300 | |

| Salaries and Wages Payable | 900 | |

| Capital | 153,550 | |

| Drawing | 8,000 | |

| Fees earned | 168,800 | |

| Rent Revenue (10) | 3,300 | |

| Salaries and Wages Expense (6) | 57,750 | |

| Utilities Expense | 14,100 | |

| Advertising Expense | 7,500 | |

| Repairs Expense | 6,100 | |

| Depreciation Expense - building | 6,400 | |

| Depreciation Expense - equipment | 2,800 | |

| Insurance Expense (7) | 4,500 | |

| Supplies Expense (9) | 1,110 | |

| Miscellaneous Expense | 4,025 | |

| 420,300 | 420,300 | |

Table (8)

Working Note (4):

Calculate accumulated depreciation- building.

Working Note (5):

Calculate of accumulated depreciation- equipment.

Working Note (6):

Calculate Salaries and Wages expenses.

Working Note (7):

Calculate the value of insurance expense at the end of the year.

Working Note (8):

Calculate accounts receivable

Working Note (9):

Calculate Supplies expense for the accounting period.

Working Note (10):

Calculate rent revenue

Hence, the total of debit and credit column of the adjusted trial balance matches and they have a total balance of $420,300.

Want to see more full solutions like this?

Chapter 3 Solutions

Financial Accounting

- The following are independent errors: a. In January 2019, repair costs of 9,000 were debited to the Machinery account. At the beginning of 2019, the book value of the machinery was 100,000. No residual value is expected, the remaining estimated life is 10 years, and straight-line depreciation is used. b. All purchases of materials for construction contracts still in progress have been immediately expensed. It is discovered that the use of these materials was 10,000 during 2018 and 12,000 during 2019. c. Depreciation on manufacturing equipment has been excluded from manufacturing costs and treated as a period expense. During 2019, 40,000 of depreciation was accounted for in that manner. Production was 15,000 units during 2019, of which 3,000 remained in inventory at the end of the year. Assume there was no inventory at the beginning of 2019. Required: Prepare journal entries for the preceding errors discovered during 2020. Ignore income taxes.arrow_forwardThe information necessary for preparing the 2021 year-end adjusting entries for Winter Storage appears below. Winter's fiscal year-end is December 31.Depreciation on the equipment for the year is $7,000.Salaries earned by employees (but not paid to them) from December 16 through December 31, 2021, are $3,400.On March 1, 2021, Winter lends an employee $12,000 and a note is signed requiring principal and interest at 6% to be paid on February 28, 2022.On April 1, 2021, Winter pays an insurance company $15,000 for a one-year fire insurance policy. The entire $15,000 is debited to prepaid insurance at the time of the purchase.$1,500 of supplies are used in 2021.A customer pays Winter $4,200 on October 31, 2021, for six months of storage to begin November 1, 2021. Winter credits deferred revenue at the time of cash receipt.On December 1, 2021, $4,000 rent is paid to a local storage facility. The payment represents storage for December 2021 through March 2022, at $1,000 per month. Prepaid…arrow_forwardSheridan, Inc. owns equipment that cost $142,000 and has a useful life of 10 years with no salvage value. On January 1, 2017, Sheridan leases the equipment to Morgan Corporation for one year with one rental payment of $15,000 on January 1. Prepare Sheridan's 2017 journal entries. (Credit account titles are automatically Indented when amount is entered. Do not Indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts) Account Titles and Explanation Date January 1 December 31 (To record receipt of lease payment) (To record the recognition of the revenue each period) Debit Creditarrow_forward

- The information necessary for preparing the 2021 year-end adjusting entries for Bearcat Personal Training Academy appears below. Bearcat’s fiscal year-end is December 31. 1. Depreciation on the equipment for the year is $7,000. 2. Salaries earned (but not paid) from December 16 through December 31, 2021, are $4,000. 3. On March 1, 2021, Bearcat lends an employee $20,000. The employee signs a note requiring principal and interest at 9% to be paid on February 28, 2022. 4. On April 1, 2021, Bearcat pays an insurance company $13,200 for a two-year fire insurance policy. The entire $13,200 is debited to Prepaid Insurance at the time of the purchase. 5. Bearcat uses $1,700 of supplies in 2021. 6. A customer pays Bearcat $2,700 on October 31, 2021, for three months of personal training to begin November 1, 2021. Bearcat credits Deferred Revenue at the time of cash receipt.7. On December 1, 2021, Bearcat pays $6,000 rent to the owner of the building. The payment represents rent for December…arrow_forwardLeni Company had a balance of P820,000 in the professional fees expense account on December 31, 2020, before considering year-end adjustments relating to the following: ➢Consultants were hired for a special project at a total fee not to exceed P650,000.The entity had recorded P550,000 of these fees based on building for work performed in 2020. ➢The attorney’s letter requested by the auditor dated Jan. 31, 2021, indicated that legal fees of P60,000 were billed on Jan. 15, 2021 for worked performed in Nov.2020, and the unbilled fees for Dec. 31, 2020 were P70,000. What amount should be reported as professional fees expense for the year ended December 31, 2020?arrow_forwardEuphoria Company had a balance of P820,000 in the professional fees expense account on December 31, 2020, before considering year-end adjustments relating to the following:➢ Consultants were hired for a special project at a total fee not to exceed P650,000. The entity had recorded P550,000 of these fees based on building for work performed in 2020.➢ The attorney’s letter requested by the auditor dated Jan. 31, 2021, indicated that legal fees of P60,000 were billed on Jan. 15, 2021 for worked performed in Nov. 2020, and the unbilled fees for Dec. 31, 2020 were P70,000.What amount should be reported as professional fees expense for the year ended December 31, 2020?arrow_forward

- Below are three independent and unrelated errors. On December 31, 2017, Wolfe-Bache Corporation failed to accrue office supplies expense of $1,850. In January 2018, when it received the bill from its supplier, Wolfe-Bache made the following entry: Office supplies expense 1,850 Cash 1,850 On the last day of 2017, Midwest Importers received a $91,000 prepayment from a tenant for 2018 rent of a building. Midwest recorded the receipt as rent revenue. At the end of 2017, Dinkins-Lowery Corporation failed to accrue interest of $8,100 on a note receivable. At the beginning of 2018, when the company received the cash, it was recorded as interest revenue. Required:For each error:1. What would be the effect of each error on the income statement and the balance sheet in the 2017 financial statements?2. Prepare any journal entries each company should record in 2018 to correct the errors.arrow_forwardMagic Cleaning Services (MCS) has a fiscal year-end of December 31. It is the first year of operations. As of year-end, MCS has the following unadjusted trial balance: In addition, it has not adjusted for the following transactions: - All of the prepaid rent expired by the end of the year. - The building was purchased early this year and has a 30-year life with no residual value. Depreciation is to be recorded for a full year on a straight-line basis. - The company provided a portion of the services related to an advance collection on December 20. It performed one-half of the services to be performed in the current year. - Wages for the current year in the amount of $24,000 should be accrued and are set to be paid out to workers in January. Journalize the necessary adjusting journal entries, then prepare an adjusted trial balance as of Dec 31, 2022arrow_forwardOlney Cleaning Company had the following items that require adjustment at year end. For one cleaning contract, $11,100 cash was received in advance. The cash was credited to Unearned Service Revenue upon receipt. At year end, $260 of the service revenue was still unearned. For another cleaning contract, $8,700 cash was received in advance and credited to Unearned Service Revenue upon receipt. At year end, $3,000 of the services had been provided. Required: 1. Prepare the adjusting journal entries needed at December 31. If an amount box does not require an entry, leave it blank. Dec. 31 Unearned Service Revenue fill in the blank 02e1a8f7d03afe9_2 fill in the blank 02e1a8f7d03afe9_3 Service Revenue fill in the blank 02e1a8f7d03afe9_5 fill in the blank 02e1a8f7d03afe9_6 Dec. 31 Unearned Service Revenue fill in the blank 02e1a8f7d03afe9_8 fill in the blank 02e1a8f7d03afe9_9 Service Revenue fill in the blank 02e1a8f7d03afe9_11 fill in the blank 02e1a8f7d03afe9_12…arrow_forward

- Queenan Company computes depreciation on delivery equipment at $1,000 for the month of June. The adjusting entry to record this depreciation should be reflected as:arrow_forwardRequired 1. Prepare and complete a 10-column work sheet for fiscal year 2019, starting with the unadjusted trial balance and including adjustments based on these additional facts. a. The supplies available at the end of fiscal year 2019 had a cost of $7,900. b. The cost of expired insurance for the fiscal year is $10,600. c. Annual depreciation on equipment is $7,000. d. The April utilities expense of $800 is not included in the unadjusted trial balance because the bill arrived after the trial balance was prepared. The $800 amount owed needs to be recorded. e. The company’s employees have earned $2,000 of accrued and unpaid wages at fiscal year-end. f. The rent expense incurred and not yet paid or recorded at fiscal year-end is $3,000. g. Additional property taxes of $550 have been assessed for this fiscal year but have not been paid or recorded in the accounts. h. The $300 accrued interest for April on the long-term notes payable has not yet been paid or recorded. 2. Using information…arrow_forwardThe unadjusted trial balance of Recessive Interiors at January 31, 2019, the end of the year, follows: The data needed to determine year-end adjustments are as follows:a. Supplies on hand at January 31 are $2,850.b. Insurance premiums expired during the year are $3,150.c. Depreciation of equipment during the year is $5,250.d. Depreciation of trucks during the year is $4,000.e. Wages accrued but not paid at January 31 are $900.Instructions1. For each account listed in the unadjusted trial balance, enter the balance in theappropriate Balance column of a four-column account and place a check mark (✓) inthe Posting Reference column.2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet andcomplete the spreadsheet. Add the accounts listed in part (3) as needed.3. Journalize and post the adjusting entries, inserting balances in the accounts affected.Record the adjusting entries on Page 26 of the journal. The following additional accounts from Recessive Interiors’…arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning