1.

To analyze: The effects of the January transaction on the

1.

Explanation of Solution

The accounting equation implies the relationship between the assets, liabilities, and the

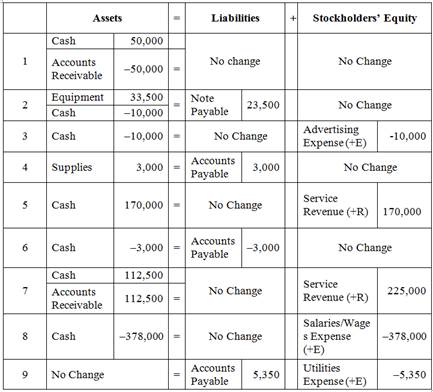

The effects of the accounting equation for the September events using a table are indicated as follows:

Table (1)

Note:

SE refers to Stockholder’s equity.

E refers to Expenses.

R refers to Revenues.

2.

To prepare:

2.

Explanation of Solution

Journal:

Journal is the book of original entry. Journal consists of the day today financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

Journal entries for September events are prepared as follows:

|

Date |

Account Title and Explanation | Debit ($) | Credit ($) | |

| 1. | Cash (A+) | 50,000 | ||

| Accounts Receivable (A–) | 50,000 | |||

| (To record the cash receipt from customer for the service rendered already) | ||||

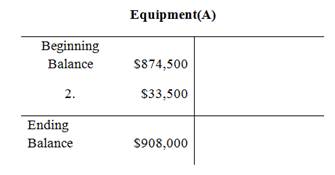

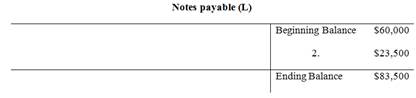

| 2. | Equipment (A+) | 33,500 | ||

| Cash (A–) | 10,000 | |||

| Notes Payable (L+) | 23,500 | |||

| (To record the purchase of equipment partly for cash and partly by signing a note) | ||||

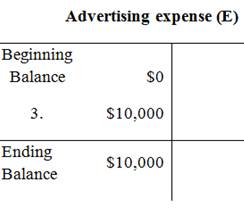

| 3. | Advertising Expense | 10,000 | ||

| Cash (A–) | 10,000 | |||

| (To record the payment made for advertising expenses) | ||||

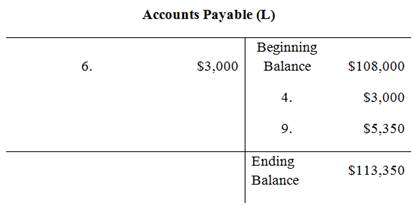

| 4. | Supplies (A+) | 3,000 | ||

| Accounts Payable (L+) | 3,000 | |||

| (To record the supplies purchased on accounts) | ||||

| 5. | Cash (A+) | 170,000 | ||

| Service Revenue (R+, SE+) | 170,000 | |||

| (To record cash received for the service provided on account ) | ||||

| 6. | Accounts Payable (L–) | 3,000 | ||

| Cash (A–) | 3,000 | |||

| (To record the payment made for the supplies purchased on account) | ||||

| 7. | Cash (A+) | 112,500 | ||

| Accounts Receivable (A+) | 112,500 | |||

| Service Revenue (R+, SE+) | 225,000 | |||

| (To record the sales made partly for cash and partly on account ) | ||||

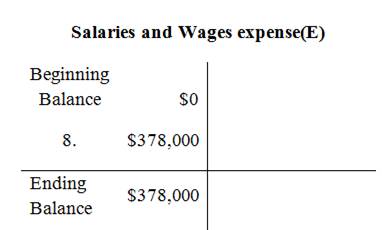

| 8. | Salaries and Wages Expense (E+, SE–) | 378,000 | ||

| Cash (A–) | 378,000 | |||

| (To record the payment of wages expenses to employees) | ||||

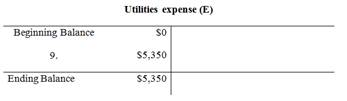

| 9. | Utilities Expense (E+, SE–) | 5.350 | ||

| Accounts Payable (L+) | 5.350 | |||

| (To record the utilities expenses incurred which are to be paid later) | ||||

Table (2)

3.

To create: The T accounts for the

3.

Explanation of Solution

T-account:

An account is referred to as a T-account, because the alignment of the components of the account resembles the capital letter ‘T’. An account consists of the three main components which are as follows:

- The title of the account

- The left or debit side

- The right or credit side

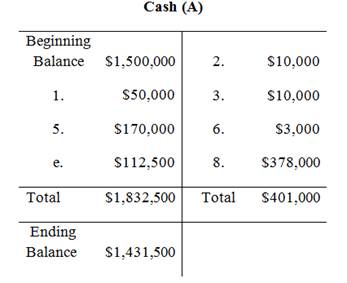

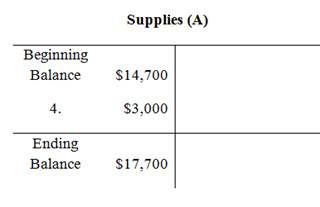

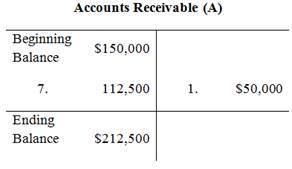

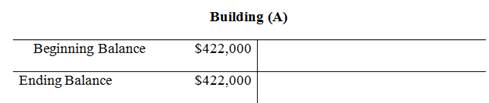

The posting of the journal entries to the T accounts are as follows:

4.

To prepare: An unadjusted

4.

Explanation of Solution

Unadjusted trial balance:

Unadjusted trial balance is that statement which contains complete list of accounts with their unadjusted balances. This statement is prepared at the end of every financial period.

An unadjusted trial balance of corporation V for the month ended January 31, 2015 is prepared as follows:

| Corporation V | ||

| Unadjusted Trial Balance | ||

| At January 31, 2015 | ||

| Particulars | Debit ($) | Credit ($) |

| Cash | $1,431,500 | |

| Accounts Receivable | 212,500 | |

| Supplies | 17,700 | |

| Equipment | 908,000 | |

| Building | 422,000 | |

| Land | 1,200,000 | |

| Accounts Payable | $113,350 | |

| Unearned Revenue | 73,500 | |

| Notes Payable | 83,500 | |

| Common Stock | 2,500,000 | |

| Retained Earnings | 1,419,700 | |

| Service Revenue | 395,000 | |

| Salaries and Wages Expense | 378,000 | |

| Advertising Expense | 10,000 | |

| Utilities Expense | 5,350 | |

| Total | $4,585,050 | $4,585,050 |

Table (3)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $4,585,050.

5.

To prepare: An income statement of corporation V for the year ended January 31, 2015.

5.

Explanation of Solution

Income statement:

The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

An income statement of corporation V for the year ended December 31is prepared as follows:

|

Corporation V Income Statement For the yearEnded January 31, 2015 |

||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Service Revenue | $395,000 | |

| Total Revenues | 395,000 | |

|

Less: Expenses: |

||

| Salaries and Wages Expense | 378,000 | |

| Advertising Expense | 10,000 | |

| Utilities Expense | 5,350 | |

| Total Expenses | 393,350 | |

| Net Loss | $1,650 | |

Table (4)

6.

To prepare: The statement of retained earnings of Corporation Vfor the year ended January 31, 2015.

6.

Explanation of Solution

Statement of Retained Earnings:

Statement of retained earnings shows, the changes in the retained earnings, and the income left in the company after payment of the dividends, for the accounting period.

The statement of retained earnings of Corporation Vfor the year ended January 31, 2015 is prepared as follows.

| Corporation V | |

| Statement of Retained Earnings | |

| For the Year Ended January 31, 2015 | |

| Particulars | $ |

| Retained Earnings, January 1, 2015 | 1,419,700 |

| Less: Net Loss | 1,650 |

| Dividends | 0 |

| Retained Earnings, December 31 | 1,421,350 |

Table (5)

7.

To create: A classified balance sheet of Corporation V for the year ended January 31, 2015.

7.

Explanation of Solution

Classified balance sheet:

This is the financial statement of a company which shows the grouping of similar assets and liabilities under subheadings.

A classified balance sheet of Corporation V for the year ended January 31, 2015 is prepared as follows:

| Corporation V | ||

| Balance Sheet | ||

| At January 31, 2015 | ||

| Assets: | $ | $ |

| Current Assets | ||

| Cash | $1,431,500 | |

| Accounts Receivable | 212,500 | |

| Supplies | 17,700 | |

| Total Current Assets | 1,661,700 | |

| Equipment | 908,000 | |

| Building | 422,000 | |

| Land | 1,200,000 | |

| Total Assets | $4,191,700 | |

| Liabilities: | ||

| Current Liabilities | ||

| Accounts Payable | $113,350 | |

| Unearned Revenue | 73,500 | |

| Total Current Liabilities | 186,850 | |

| Notes Payable | 83,500 | |

| Total Liabilities | 270,350 | |

| Stockholders’ Equity | ||

| Common Stock | 2,500,000 | |

| Retained Earnings | 1,421,350 | |

| Total Stockholders’ Equity | 3,921,350 | |

| Total Liabilities and Stockholders’ Equity | $4,191,700 | |

Table (6)

8.

To calculate: The net profit margin of the company.

8.

Explanation of Solution

The net profit margin of the Company is determined as follows:

Want to see more full solutions like this?

Chapter 3 Solutions

Fundamentals of Financial Accounting

- Megasoft Corporation develops, produces, and markets a wide range of computer software including the Windows operating system. Megasoft reported the following information about Net Sales Revenue and Accounts Receivable (all amounts in millions). June 30, 2016 June 30, 2015 Accounts Receivable, Net of Allowance for Doubtful Accounts of $300 and $350 $16,850 67,000 $15,600 61,000 Net Revenues According to its Form 10-K, Megasoft recorded Bad Debt Expense of $21 and did not recover any previously written-off accounts during the year ended June 30, 2016. Required: 1. What amount of accounts receivable was written off during the year ended June 30, 2016? (Enter your answer in millions.) 2. What was Megasoft's receivables turnover ratio in 2016? (Round your answer to 1 decimal place.) 1. Accounts Receivable Written-Off 2. Receivables Turnover Ratio million timesarrow_forwardRequired Information [The following information applies to the questions displayed below.] Web Wizard, Incorporated, has provided information technology services for several years. For the first two months of the current year, the company has used the percentage of credit sales method to estimate bad debts. At the end of the first quarter, the company switched to the aging of accounts receivable method. The company entered into the following partial list of transactions during the first quarter. a. During January, the company provided services for $40,000 on credit. b. On January 31, the company estimated bad debts using 1 percent of credit sales. c. On February 4, the company collected $20,000 of accounts receivable. d. On February 15, the company wrote off $100 account receivable. e. During February, the company provided services for $30,000 on credit. f. On February 28, the company estimated bad debts using 1 percent of credit sales. g. On March 1, the company loaned $2,400 to an…arrow_forwardRequired information [The following information applies to the questions displayed below.] Web Wizard, Incorporated, has provided information technology services for several years. For the first two months of the current year, the company has used the percentage of credit sales method to estimate bad debts. At the end of the first quarter, the company switched to the aging of accounts receivable method. The company entered into the following partial list of transactions during the first quarter. a. During January, the company provided services for $44,000 on credit. b. On January 31, the company estimated bad debts using 1 percent of credit sales. c. On February 4, the company collected $22,000 of accounts receivable. d. On February 15, the company wrote off $150 account receivable. e. During February, the company provided services for $34,000 on credit. f. On February 28, the company estimated bad debts using 1 percent of credit sales. g. On March 1, the company loaned $2,200 to an…arrow_forward

- Required information [The following information applies to the questions displayed below.] Web Wizard, Incorporated, has provided information technology services for several years. For the first two months of the current year, the company has used the percentage of credit sales method to estimate bad debts. At the end of the first quarter, the company switched to the aging of accounts receivable method. The company entered into the following partial list of transactions during the first quarter. a. During January, the company provided services for $46,000 on credit. b. On January 31, the company estimated bad debts using 1 percent of credit sales. c. On February 4, the company collected $23,000 of accounts receivable. d. On February 15, the company wrote off $100 account receivable. e. During February, the company provided services for $36,000 on credit. f. On February 28, the company estimated bad debts using 1 percent of credit sales. g. On March 1, the company loaned $2,400 to an…arrow_forwardThe following are excerpts from the financial statements of 2018 and 2019 of Mandela Corporation. 2019 2018 Sales $187,600 $195,000 Accounts Receivable (net): Beginning of Year 68,100 66,500 End of Year 60,200 68,100 A newly hired manager has started implementing new credit policies. Required: a. As a consultant, you are contracted to analyze Accounts Receivable Turnover and Number of Days’ Sales in Receivable and provide opinion as to whether Mandela’s credit policy changes are working b. What conclusions does your analysis suggest. Are the new credit policies working?arrow_forwardThe following are excerpts from the financial statements of 2018 and 2019 of Mandela Corporation. 2019 2018 Sales $187,600 $195,000 Accounts Receivable (net): Beginning of Year 68,100 66,500 End of Year 60,200 68,100 A newly hired manager has started implementing new credit policies. Required: As a consultant, you are contracted to analyze Accounts Receivable Turnover and Number of Days’ Sales in Receivable and provide opinion as to whether Mandela’s credit policy changes are working What conclusions does your analysis suggest. Are the new credit policies working ?arrow_forward

- Johnson company’s financial year ended on December 31, 2010. All the transactions related to the company’s uncollectible accounts are can be found below: The accounts receivable account had a balance of $114,630 and the beginning balance in the allowance for uncollectible accounts was $6,200. Prepare journal entries for each transaction. Prepare the Allowance for Uncollectible and the Accounts Receivable accounts based on the information presented and balance off each account.arrow_forwardCredit department of the Starlight Inc. estimates uncollectible accounts while analyzing various receivables. By the end of year 2017, credit manager collects following information relating to receivables and uncollectible accounts.Gross accounts receivable at the end of year as presented in balance sheet of company $520000. On the basis of past experience, company estimates that 2.5 percent of gross accounts receivable are uncollectible. During 2017, an amount of $1500 receivable from specific customer is expected to be written off as uncollectible. However, of these accounts written off, total receivables of $500 were subsequently collected. Required: a. Prepare all necessary journal entries and calculate amount of accounts receivable in the balance sheet of Starlight Inc. before and after write-off of uncollectible accounts as at December 31, 2017. b. Further, Company comes to know that a customer whose receivables were due on December 1, 2017, could not pay due amount of $50000.…arrow_forwardRequired information [The following information applies to the questions displayed below.] Web Wizard, Inc., has provided information technology services for several years. For the first two months of the current year, the company has used the percentage of credit sales method to estimate bad debts. At the end of the first quarter, the company switched to the aging of accounts receivable method. The company entered into the following partial list of transactions during the first quarter. a. During January, the company provided services for $44,000 on credit. b. On January 31, the company estimated bad debts using 1 percent of credit sales. c. On February 4, the company collected $22,000 of accounts receivable. d. On February 15, the company wrote off a $150 account receivable. e. During February, the company provided services for $34,000 on credit. f. On February 28, the company estimated bad debts using 1 percent of credit sales. g. On March 1, the company loaned $2,200 to an…arrow_forward

- The Accounts Receivable balance and Allowance for Bad Debts for Turning Leaves Furniture Restoration at December 31, 2015, was $10,800 and $2,000 (credit balance). During 2016, Turning Leaves completed the following transactions: i (Click the icon to view the transactions.) Read the requirements. 1925 a. Requirement 1. Journalize Turning Leaves's transactions for 2016 assuming Turning Leaves uses the allowance method. (Record debits first, then credits. Select the explanation on the last line of the journal entry table.) a. Sales revenue on account, $265,800 (ignore Cost of Goods Sold). Accounts and Explanation Debit .. Creditarrow_forwardI'm studying for a test and I want to know how to do each question for it, can you walk me through step by step how to solve this one? The following data concern XYZ Corporation for 2018:Bad debts expense for the year 11,000Accounts receivable—December 31, 2018 235,000Credit sales during the yearAllowance for doubtful accounts—December 31, 20181,600,00018,000 Calculate the net realizable value of the accounts receivable.arrow_forwardCHECK OUT: 1. At December 31, 2013, XYZ Co. reported the following information on its balance sheet: Accounts receivable $960,000 Less: Allowance for doubtful accounts 80,000 During 2014, the company had the following transactions related to receivables. 1. Sales on account of $3,700,000 2. Sales returns and allowances 50,000 3. Collections of accounts receivable 2,810,000 4. Write-offs of accounts receivable deemed uncollectible 90,000 5. Recovery of bad debts previously written off as uncollectible 29,000 Instructions: A. Prepare the journal entries to record each of these five transactions. Assume that no cash discounts were taken on the collections of accounts receivable. B. Enter January 1, 2014, balances in Accounts Receivable and Allowance for Doubtful Accounts, post the entries to the two accounts (use T-accounts), and determine the balances. C. Prepare the journal entry to record bad debt expense for 2014, if the aging of accounts receivable indicates that expected bad debts…arrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning