Concept explainers

Videos

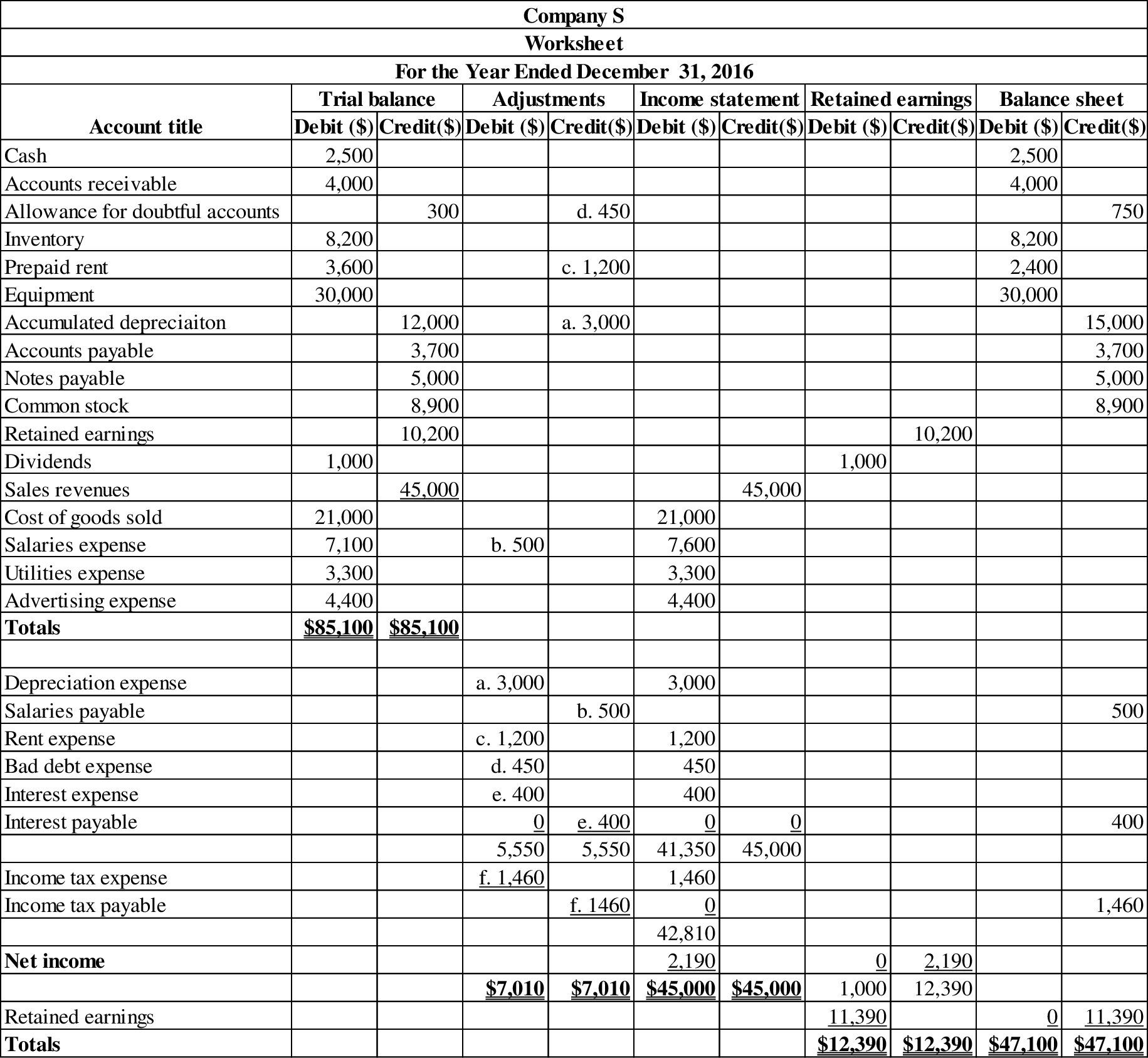

1.

Prepare the worksheet for the year ended December 31, 2016.

1.

Explanation of Solution

Worksheet: A worksheet is a tool that is used while preparing a financial statement. It is a type of form, having multiple columns and it is used in the adjustment process.

Prepare the worksheet for the year ended December 31, 2016:

Table (1)

2.

Prepare the financial statements of Company S for the year ended December 31, 2016.

2.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare income statement of Company S for the year ended December 31, 2016:

| Company S | ||

| Income statement | ||

| For the Year Ended December 31, 2016 | ||

| Particulars | Amount($) | Amount($) |

| Sales revenue | 45,000 | |

| Less: Cost of goods sold | (21,000) | |

| Gross profit | 24,000 | |

| Less: Operating expenses: | ||

| Salaries expense | 7,600 | |

| Utilities expense | 3,300 | |

| Advertising expense | 4,400 | |

| 3,000 | ||

| Rent expense | 1,200 | |

| 450 | ||

| Total operating expense | (19,950) | |

| Income from operations | 4,050 | |

| Other items: | ||

| Interest expense | (400) | |

| Income before income taxes | 3,650 | |

| Less: Income tax expense | (1,460) | |

| Net income | $2,190 | |

| Earnings per share (1,000 shares) | $2.19 | |

Table (2)

Working notes 1: Calculate the amount of salaries expense.

Working note 2: Calculate the amount of rent expense.

Working note 3: Calculate the amount of depreciation expense.

Working note 4: Calculate the amount of income tax expense.

Working note 5: Calculate the amount of bad debt expense.

Working note 6: Calculate earnings per share.

Statement of Retained Earnings: Statement of retained earnings shows, the changes in the retained earnings, and the income left in the company after payment of the dividends, for the accounting period.

Prepare statement of retained earnings of Company S for the year ended December 31, 2016:

| Company S | ||

| Statement of Retained Earnings | ||

| For the Year Ended December 31, 2016 | ||

| Particulars | Amount ($) | Amount ($) |

| Retained earnings, January 1, 2016 | 10,200 | |

| Add: Net income | 2,190 | |

| Subtotal | 12,390 | |

| Less: Dividends | (1,000) | |

| Retained earnings at December 31, 2016 | $11,390 | |

Table (3)

Balance Sheet: Balance Sheet is one of the financial statements which summarize the assets, the liabilities, and the Shareholder’s equity of a company at a given date. It is also known as the statement of financial status of the business.

Prepare the balance sheet of Company S for the year ended December 31, 2016:

| Company S | ||

| Balance Sheet | ||

| As on December 31, 2016 | ||

| Assets | ||

| Current assets: | Amount ($) | Amount ($) |

| Cash | 2,500 | |

| Accounts receivable | 4,000 | |

| Less: Allowance for doubt accounts | (750) | 3,250 |

| Inventory | 8,200 | |

| Prepaid rent | 2,400 | |

| Total current assets | ||

| Property, plant and equipment: | ||

| Equipment | 30,000 | |

| Less: Accumulated depreciation | (15,000) | |

| Net property, plant and equipment | 15,000 | |

| Total assets | $31,350 | |

| Liabilities and Equity | ||

| Liabilities: | ||

| Current liabilities: | ||

| Accounts payable | 3,700 | |

| Notes payable | 5,000 | |

| Salaries payable | 500 | |

| Interest payable | 400 | |

| Income taxes payable | 1,460 | |

| Total liabilities | 11,060 | |

| Shareholders’ Equity | ||

| Contributed Capital: | ||

| Common stock | 8,900 | |

| Retained earnings | 11,390 | |

| Total shareholders’ equity | 20,290 | |

| Total liabilities and shareholders’ equity | $31,350 | |

Table (4)

3.

Prepare the closing entries for the year ended December 31, 2016 in the general journal.

3.

Explanation of Solution

Prepare the closing entries:

| Date | Accounts title and explanation | Post Ref. | Debit | Credit |

| ($) | ($) | |||

| December 31, 2016 | Sales Revenue | 45,000 | ||

| Income Summary | 45,000 | |||

| (To close the revenue accounts) | ||||

| December 31, 2016 | Income Summary | 42,810 | ||

| Cost of Goods Sold | 21,000 | |||

| Salaries Expense | 7,600 | |||

| Utilities Expense | 3,300 | |||

| Advertising Expense | 4,400 | |||

| Depreciation Expense | 3,000 | |||

| Rent Expense | 1,200 | |||

| Bad Debt Expense | 450 | |||

| Interest Expense | 400 | |||

| Income Tax Expense | 1,460 | |||

| (To close the expense accounts) | ||||

| December 31, 2016 | Income Summary | 2,190 | ||

| Retained Earnings | 2,190 | |||

| (To close the income summary account) | ||||

| December 31, 2016 | Retained Earnings | 1,000 | ||

| Dividends | 1,000 | |||

| (To close the dividends account) | ||||

Table (5)

Want to see more full solutions like this?

Chapter 3 Solutions

EBK INTERMEDIATE ACCOUNTING: REPORTING

- On July 31, 2018, Choice Landscapes discarded equipment that had a cost of $17,680. Accumulated Depreciation as of December 31, 2017, was $16,000. Assume annual depreciation on the equipment is $1,680. Journalize the partial-year depreciation expense and disposal of the equipment. (Record debits first, then credits Select the explanation on the last line of the journal entry table.) Journalize the partial-year depreciation expense. Date Accounts and Explanation Debit Credit Jul. 31arrow_forwardOn August 31, 2018, Option Landscapes discarded equipment that had a cost of $16,500. Accumulated Depreciation as of December 31, 2017, was $15,000. Assume annual depreciation on the equipment is $1,500. Journalize the partial-year depreciation expense and disposal of the equipment. (Record debits first, then credits. Select the explanation on the last line of the journal entry table.)arrow_forwardPrepare the necessary journal entries to record the following transactions in 2013 for the Hoover Company. April 13 - Sold a delivery truck for $7,000. The delivery truck originally cost $45,000 and had accumulated depreciation of $41,000 on the date of sale. Assume the depreciation on the truck has already been recorded for the current year. May 13 - Discarded old mixing equipment that originally cost $100,000 and had a book value of $14,000 on the date of disposal. Assume depreciation on the equipment has already been recorded for the current year. Oct. 13 - Sold a toaster for $5,000. The toaster originally cost $30,000 and had accumulated depreciation of $22,000 on the date of sale. Assume the depreciation on the toaster has already been recorded for the current year.arrow_forward

- Swifty Corporation owns equipment that cost $70,800 when purchased on April 1, 2013. Depreciation has been recorded at a rate of $11,800 per year, resulting in a balance in accumulated depreciation of $56,050 at December 31, 2017. The equipment is sold on July 1, 2018, for $14,160. Prepare journal entries to (a) update depreciation for 2018 and (b) record the sale. (Credit account titles are automatically indented when amount is entered. Do not indent manually.) No. Account Titles and Explanation Debit Credit (a) (b)arrow_forwardBlue Company shows the following entries in its Equipment account for 2021. All amounts are based on historical cost. Equipment 2021 2021 Jan. 1 Balance 126,630 June 30 Cost of equipment sold Aug. 10 Purchases 31,540 (purchased prior to 2021) 21,250 12 Freight on equipment purchased 820 25 Installation costs 2,510 Nov. 10 Repairs 450 Assuming that company policy is to charge a full year depreciation in the year of purchase and the year of sale, compute the proper depreciation charge for 2021 under each of the methods listed below. Assume an estimated life of 10 years, with no salvage value. The machinery included in the January 1, 2021, balance was purchased in 2019. (Round answers to 0 decimal places, e.g. 45,892.) (1) Straight-line $ (2) Sum-of-the-years'-digitsarrow_forwardLMN Company purchased factory equipment for $64,000 on January 1, 2016. The equipment is estimated to have a useful life of 12 years, at which point it will have a residual value of $4,000. LMN Company uses the straight-line method to account for depreciation. What is the journal entry on December 31, 2016 to record the yearly depreciation? Select one: a. Debit depreciation expense $5,000; Credit Equipment $5,000 b. Debit depreciation expense $5,333; Credit Accumulated depreciation: $5,333 c. Debit depreciation expense $5,000; Debit accumulated depreciation: $5,000 d. Debit depreciation expense $5,000; Credit Accumulated depreciation: $5,000arrow_forward

- Recording Errors and Changes in Accounting Estimates On January 1, 2018, Zale Company purchased a building for $560,000. The building was estimated to have a useful life of 30 years and no residual value and was depreciated using the straight-line method. In 2020, the company revised the estimated total useful life to 25 years and adjusted the residual to $7,000. In addition, in 2020, the company discovered that building improvements of $8,400 made in early 2019 were incorrectly expensed as repair expense. Disregard income tax considerations. a. Provide the journal entry to record the adjustment for the error discovered in 2020. Assume that the error is material to the company. b. Provide the journal entry in 2020 to record depreciation expense. Note: Round your final answer to the nearest whole dollar. For example, enter 502 for 502.4 and enter 503 for 502.5.Note: Record your credit accounts in alphabetical order using the first letter of the account name. Date Account Name Dr.…arrow_forwardShannon Company began operations on January 1, 2020. The financial statement contained the following errors: YEAR 2020- Ending inventory 160,000 understated; Depreciation expense 60,000 understated; Insurance expense 100,000 overstated; Prepaid insurance 100,000 understated; YEAR 2021 - Ending inventory 150,000 overstated; Insurance expense 100,000 understated. On December 31, 2021, fully depreciation machinery was sold for P110,000 cash but the sale was not reported until 2022. No corrections have been made for any of the errors. Ignoring income tax, what amount should be reported as net effect of the errors on Net Income for 2020? a. 200,000 over b. 200,000 under c. 260,000 under d. 0arrow_forwardWillow Creek Company purchased and installed carpet in its new general offices on April 30 for a total cost of $36,288. The carpet is estimated to have a 16-year useful life and no residual value. A. Prepare the journal entry necessary for recording the purchase of the new carpet. Refer to the Chart of Accounts for exact wording of account titles. B. Record the December 31 adjusting entry for the partial-year depreciation expense for the carpet, assuming that Willow Creek Company uses the straight-line method. Refer to the Chart of Accounts for exact wording of account titles. CHART OF ACCOUNTS Willow Creek Company General Ledger ASSETS 110 Cash 111 Petty Cash 112 Accounts Receivable 114 Interest Receivable 115 Notes Receivable 116 Merchandise Inventory 117 Supplies 119 Prepaid Insurance 120 Land 123 Carpet 124 Accumulated Depreciation-Carpet 125 Equipment 126 Accumulated Depreciation-Equipment 130 Mineral Rights 131…arrow_forward

- For financial reporting, Clinton Poultry Farms has used the declining-balance method of depreciation for conveyor equipment acquire at the beginning of 2015 for $2,736,000. Its useful life was estimated to be six years with a $204,000 residual value. At the beginning of 2018, Clinton decides to change to the straight-line method. The effect of this change on depreciation for each year is as follows (S In 000s): Year Straight-Line Declining Balance 2015 $ 422 2016 422 2017 422 $1,266 No 1 $912 608 405 $1,925 Required: 2. Prepare any 2018 Journal entry related to the change. (Enter your answers in dollars rounded to the nearest thousand. If no entry Is required for a transaction/event, select "No Journal entry required" In the first account field.) Event 1 Difference $490 186 (17) Depreciation expense $659 Answer is complete but not entirely correct. General Journal Accumulated depreciation Debit 211,333 X Credit 211,333arrow_forwardI) ABC Ltd purchases a factory machine at $210,000 on January 1, 2018. ABC Ltd expects the machine to have a salvage value of $30,000 at the end of its 5-year useful life. Requirement: Prepare depreciation schedules for the declining balance using double the straight-line rate. ii) ABC Company has the following inventory, purchases, and sales data for August 2019. Inventory: August 1 200 units @ 4.00 Purchases: August 10 500 units @ 4.30 August 18 400 units @ 4.75 August 27 300 units @ 5.00 Sales: August 15 700 units August 25 300 units August 29 400 units Requirement: Under a perpetual inventory system, determine the cost of inventory on hand on August 31 and the cost of goods sold for August under the Average-cost method.arrow_forwardWolfpack Corp. has determined it should record depreciation expense of $40,000 for the year ending 12/31/X7. Required: In the general journal below, complete the year-end entry to record depreciation. Debit Credit Dec 31 ? 40,000 ? 40,000arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning