Concept explainers

Videos

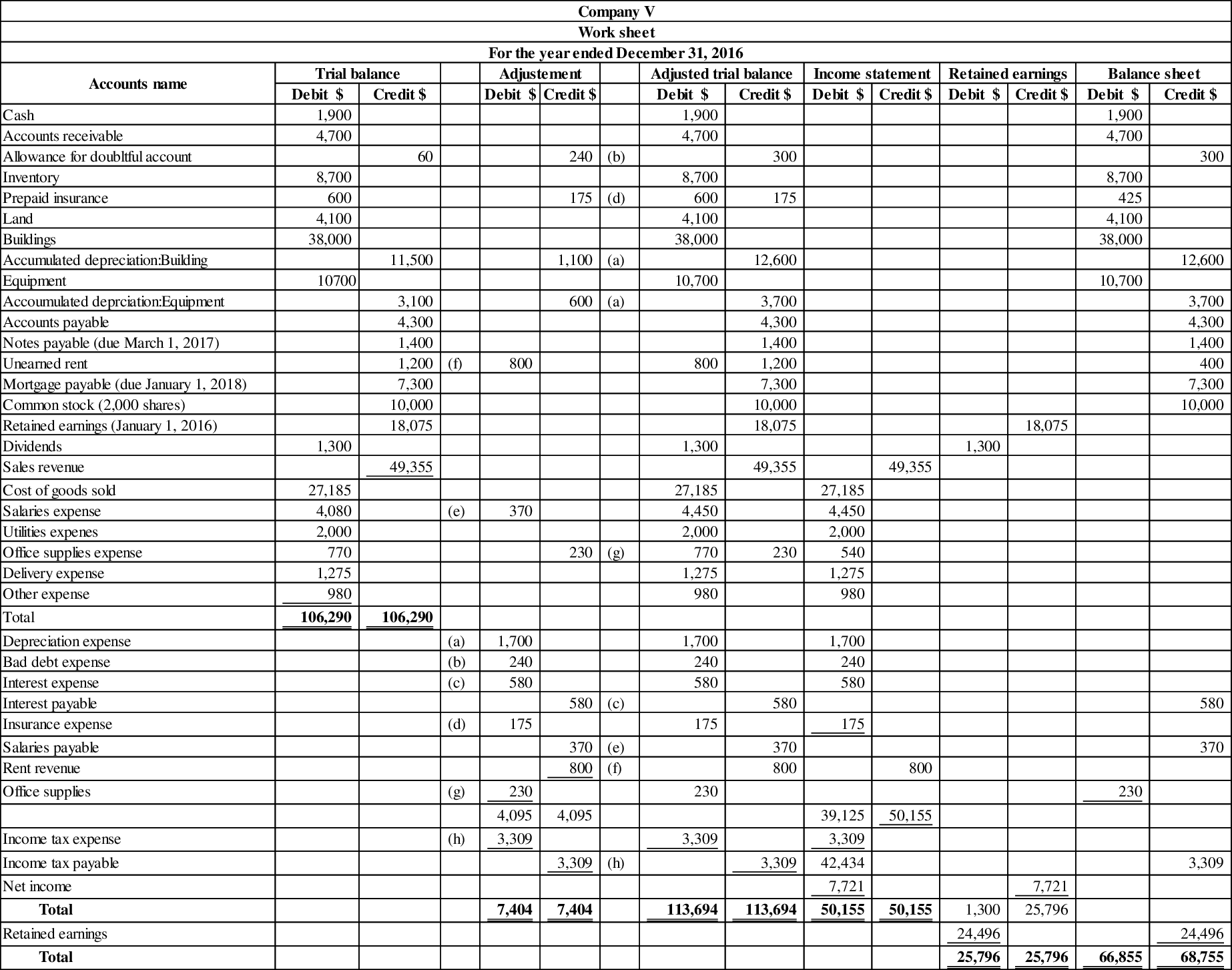

1 and 2

Prepare a 10 column worksheet for the given account balances, and prepare the

1 and 2

Explanation of Solution

Worksheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Prepare 10 column worksheet for the given account balances, and trial balance as follows:

Figure (1)

Adjusting entry:

| Date | Account Title & Explanation | Debit ($) | Credit($) |

| December 31, 2016 | 1,700 | ||

| 1,100 | |||

| Accumulated depreciation - Equipment | 600 | ||

| (To record the depreciation expense incurred at the end of the accounting year) | |||

| December 31, 2016 | 240 | ||

| Allowance for doubtful accounts | 240 | ||

| (To record the bad debts expense estimated at the end of the accounting year) | |||

| December 31, 2016 | Interest expense | 580 | |

| Interest payable | 580 | ||

| (To record the interest expense incurred at the end of the accounting year) | |||

| December 31, 2016 | Insurance expense | 175 | |

| Prepaid insurance | 175 | ||

| (To record the insurance expense incurred at the end of the accounting year) | |||

| December 31, 2016 | Salaries expense | 370 | |

| Salaries payable | 370 | ||

| (To record the salaries expense accrued at the end of the accounting year) | |||

| December 31, 2016 | Unearned rent | 800 | |

| Rent revenue | 800 | ||

| (To record the rent revenue recognized) | |||

| December 31, 2016 | Office supplies expense | 230 | |

| Office supplies | 230 | ||

| (To record the supplies used during the year) | |||

| December 31, 2016 | Income tax expense (1) | 3,309 | |

| Income tax payable | 3,309 | ||

| (To record the income tax expense incurred at the end of the accounting year) |

Table (1)

Working note (1):

Calculate the value of income tax expense.

3.

Prepare income statement, retained earnings, and balance sheet of Company V.

3.

Explanation of Solution

Financial statements: Financial statements are condensed summary of transactions communicated in the form of reports for the purpose of decision making. The financial statements are balance sheet, income statement, statement of retained earnings, and the cash flow statement.

Prepare income statement, retained earnings, and balance sheet of Company V as follows:

| Company V | ||

| Income statement | ||

| For the year ended December 31, 2016 | ||

| Particulars | Amount($) | Amount ($) |

| Service revenue | 49,355 | |

| Less: Cost of goods sold | (27,185) | |

| Gross profit | 22,170 | |

| Less: Operating expense | ||

| Salaries expense | 4,450 | |

| Utilities expense | 2,000 | |

| Office supplies expense | 540 | |

| Delivery expense | 1,275 | |

| Depreciation expense | 1,700 | |

| Bad debt expense | 240 | |

| Insurance expense | 175 | |

| Other expense | 980 | |

| Total operating expense | 11,360 | |

| Income from operations | 10,810 | |

| Other items: | ||

| Rent revenue | 800 | |

| Interest expense | (580) | 220 |

| Income before income taxes | 11,030 | |

| Income tax expense | (3,309) | |

| Net income (A) | 14,339 | |

| Number of shares (B) | 2,000 shares | |

| Earnings per share | $3.86 | |

Table (2)

| Company V | |

| Statement of retained earnings | |

| For the year end December 31, 2016 | |

| Particulars | Amount ($) |

| Retained earnings on January 1, 2016 | 18,075 |

| Add: Net income | 7,721 |

| 25,796 | |

| Less: Dividend for 2016 | (1,300) |

| Retained earnings on December 31, 2016 | 24,496 |

Table (3)

| Company V | ||

| Balance sheet | ||

| As at December 31, 2016 | ||

| Assets | Amount ($) | Amount ($) |

| Current assets: | ||

| Cash | 1,900 | |

| Accounts receivable | 4,700 | |

| Less: Allowance for doubtful accounts | (300) | 4,400 |

| Inventory | 8,700 | |

| Prepaid insurance | 425 | |

| Office supplies | 230 | |

| Total current assets (C) | 15,655 | |

| Property, plant and equipment: | ||

| Land | 4,100 | |

| Buildings | 38,000 | |

| Less: Accumulated depreciation | (12,600) | 25,400 |

| Equipment | 10,700 | |

| Less: Accumulated depreciation | (3,700) | 7,000 |

| Total property, plant and equipment (D) | 36,500 | |

| Total assets | 52,155 | |

| Liabilities | ||

| Current liabilities: | ||

| Accounts payable | 4,300 | |

| Notes payable (due March 1, 2017) | 1,400 | |

| Interest payable | 580 | |

| Salaries payable | 370 | |

| Unearned rent | 400 | |

| Income tax payable | 3,309 | |

| Total current liabilities | 10,359 | |

| Long-term liabilities: | ||

| Mortgage payable (due January 1, 2018) | 7,300 | |

| Total liabilities | 17,659 | |

| Shareholders' equity | ||

| Contributed capital: | ||

| Common stock | 10,000 | |

| Retained earnings | 24,496 | 34,496 |

| Total shareholder's equity | 52,155 | |

Table (4)

4.

Prepare closing entries of Company V for the current year.

4.

Explanation of Solution

Closing

Prepare closing entries of Company V for the current year as follows:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| December 31, 2016 | Sales revenue | 49,355 | |

| Rent revenue | 800 | ||

| Income summary | 50,155 | ||

| (To close the sales revenue and rent revenue account) | |||

| December 31, 2016 | Income summary | 42,434 | |

| Cost of goods sold | 27,185 | ||

| Salaries expense | 4,450 | ||

| Utilities expense | 2,000 | ||

| Office supplies expense | 540 | ||

| Delivery expense | 1,275 | ||

| Other expense | 980 | ||

| Depreciation expense | 1,700 | ||

| Bad debt expense | 240 | ||

| Interest expense | 580 | ||

| Insurance expense | 175 | ||

| Income tax expense | 3,309 | ||

| (To close all expenses account) | |||

| December 31, 2016 | Income summary | 7,721 | |

| Retained earnings (2) | 7,721 | ||

| (To close the income summary account) | |||

| December 31, 2016 | Retained Earnings | 1,300 | |

| Dividends | 1,300 | ||

| (To close the dividends account.) |

Table (5)

Closing entry for revenue account:

In this closing entry, the sales revenue and rent revenue account is closed by transferring the amount of revenue to the income summary account in order to bring the revenue accounts balance to zero. Hence, debit all revenue account for $50,155, and credit the income summary account for $50,155.

Closing entry for expenses account:

In this closing entry, cost of goods sold, operating expense, and income tax expense are closed by transferring the amount of all expenses to the income summary account in order to bring all the expense accounts balance to zero. Hence, debit the income summary account for $42,434, and credit all the expenses account for $42,434.

Closing entry for income summary account:

In this closing entry, the income summary account is closed by transferring the amount of net income to the retained earnings account in order to bring the income summary balance to zero. Hence, debit the income summary account for $7,721, and credit the retained earnings for $7,721.

Closing entry for dividends account:

The dividends are paid to the shareholders out of the retained earnings. Thus, retained earnings are debited since the earnings are decreased on payment of dividend. Dividends are a component of shareholders’ equity account. It is credited because dividends are transferred to retained earnings account.

Working note (2):

Calculate the value of retained earnings.

Want to see more full solutions like this?

Chapter 3 Solutions

Cengagenowv2, 1 Term Printed Access Card For Wahlen/jones/pagach’s Intermediate Accounting: Reporting And Analysis, 2017 Update, 2nd

- Prior to adjustments, Barrett Companys account balances at December 31, 2019, for Accounts Receivable and the related Allowance for Doubtful Accounts were 1,200,000 and 60,000, respectively. An aging of accounts receivable indicated that 106,000 of the December 31, 2019, receivables may be uncollectible. The net realizable value of accounts receivable at December 31, 2019, was: a. 1,034,000 b. 1,094,000 c. 1,140,000 d. 1,154,000arrow_forwardAt December 31, 2022, the records of Kingbird, Inc. contained the following amounts before adjustment. Accounts Receivable Allowance for Doubtful Accounts (a) What amount of bad debt expense will Kingbird, Inc. report if its aging schedule indicates that $12,240 of accounts receivable will be uncollectible. Bad debt expense $ $216,000 1,800 (b) During the next month, January 2023, a $2,520 account receivable is written off as uncollectible. What amount of bad debt expense will Kingbird, Inc. report in January 2023? Bad debt expense $ (c) Repeat part (b), assuming that Kingbird, Inc. uses the direct write-off method instead of the allowance method in accounting for uncollectible accounts receivable. Bad debt expense $arrow_forwardCompany L as a fiscal year-end of 12/31. The Company uses the aging of receivables method to account for bad debts. At the end of the current year, using the aging of receivable method, management estimated that $15,750 of the accounts receivable balance would be uncollectible. Prior to any year-end adjustments, the Allowance for Doubtful Accounts had a DEBIT balance of $375. What adjusting entry should the company make at the end of the current year to record its estimated bad debts expense AND what would be the balance of the Allowance for doubtful accounts after the adjustment is made?arrow_forward

- DI-TWO Corporation had the following accounts and their balances on December 31 before any adjustments: Sales P5,000,000 Accounts Receivable 600,000 Allowance for doubtful accounts 25,000arrow_forwardAt the adjustments: end of the month, you are also required to take into consideration the following (a) Non-current assets are to be depreciated at the rate of 0.5% per month. (b) Allowance for doubtful debt is set at a rate of 1% on accounts receivable balance. (c) Electricity and water bill for the month of January 2020 is still accrued. (d) Insurance for the month of February 2020 is paid in advance. (e) Closing inventory of fuel saving oil amounted to 10% of purchases account balance. On 31 January 2020, you are required to balance all the accounts and prepare the following: (a) Trial Balance as at 31 January 2020 (b) Statement of Profit or Loss for the month ended 31 January 2020 (c) Statement of Financial Position as at 31 January 2020arrow_forwardThe following Is a portion of the current assets section of the balance sheets of Avantl's, Inc., at December 31, 2020 and 2019: 12/31/20 12/31/19 Accounts receivable, less allowance for bad debts of $9,884 and $18,755, respectively $178,387 $223,883 Requlred: a. If $11,579 of accounts recelvable were written off during 2020, what was the amount of bad debts expense recognized for the year? (Hint. Use a T-account model of the Allowance account, plug in the three amounts that you know, and solve for the unknown.) Bad debt expense b. The December 31, 2020, Allowance account balance Includes $3,017 for a past due account that is not likely to be collected. This account has not been written off. |(1) If it had been written off, will there be any effect of the write-off on the working capital at December 31, 2020? Yes No (2) If It had been written off, will there be any effect of the write-off on net Income and ROI for the year ended December 31, 2020? Yes No c. The level of Avantı's sales…arrow_forward

- At December 31, 2022, the trial balance of Concord Corporation contained the following amounts before adjustment. Accounts Receivable Allowance for Doubtful Accounts Sales Revenue Debit (b) (c) $189,800 Credit $ 1,570 871,700 (a) Prepare the adjusting entry at December 31, 2022, to record bad debt expense, assuming that the aging schedule indicates that $11,020 of accounts receivable will be uncollectible. Repeat part (a), assuming that instead of a credit balance there is a $1,570 debit balance in Allowance for Doubtful Accounts. During the next month, January 2023, a $2,050 account receivable is written off as uncollectible. Prepare the journal entry to record the write-off. (d) Repeat part (c), assuming that Concord Corporation uses the direct write-off method instead of the allowance method in accounting for uncollectible accounts receivable. (Credit account titles are automatically indented when amount is entered. Do not indent manually.)arrow_forwardAccounting Gowns, Inc. uses 'the percentage of receivables' basis to estimate its impairment loss. At December 31, 2020, per the accounts receivable aging report, Gowns estimates total uncollectible amounts in the future as $5,500. The beginning balance of allowance for impairment is $1,300. The accounts receivable balance at December 31, 2020 is $100,000. What is the amount of impairment loss for the year? Select one: $4,200 $5,500 $6,800 $1,300arrow_forwardDI-TWO Corporation had the following accounts and their balances on December 31 before any adjustments: Sales P5,000,000 Accounts Receivable 600,000 Allowance for doubtful accounts 25,000arrow_forward

- Spring Garden Flowers had the following balances at December 31, 2024, before the year-end adjustments: E (Click the icon to view the balances.) The aging of accounts receivable yields the following data: E (Click the icon to view the accounts receivable aging schedule.) Requirements Journalize Spring's entry to record bad debts expense for 2024 using the aging-of-receivables method. 1. 2. Prepare a T-account to compute the ending balance of Allowance for Bad Debts. Requirement 1. Journalize Spring's entry to record bad debts expense for 2024 using the aging-of-receivables method. (Record debits first, then credits. Select the explanation on the last line of the journal entry table.) Date Accounts Debit Credit Dec. 31 Data Table Accounts Receivable Allowance for Bad Debts 66,000 1,615 Requirement 2. Prepare a T-account to compute the ending balance of Allowance for Bad Debts. Allowance for Bad Debts Print Done Data Table Age of Accounts Receivable 0-60 Days Over 60 Days Total…arrow_forwardAt December 31, 2017, the trial balance of Windsor, Inc. contained the following amounts before adjustment. Debit Credit Accounts Receivable $178,900 Allowance for Doubtful Accounts $ 1,610 Sales Revenue 915,400 (a) Prepare the adjusting entry at December 31, 2017, to record bad debt expense, assuming that the aging schedule indicates that $10,260 of accounts receivable will be uncollectible. (b) Repeat part (a), assuming that instead of a credit balance there is a $1,610 debit balance in Allowance for Doubtful Accounts. (c) During the next month, January 2018, a $1,940 account receivable is written off as uncollectible. Prepare the journal entry to record the write-off. (d) Repeat part (c), assuming that Windsor, Inc. uses the direct write-off method instead of the allowance method in accounting for uncollectible accounts receivable. (Credit account titles are automatically indented when amount is entered. Do not indent…arrow_forwardOceanside Company uses the balance sheet approach in estimating uncollectible accounts expense. It has just completed an aging analysis of accounts receivable at December 31, 2019. This analysis disclosed the following information: Age Group Total Percentage Considered Uncollectible Not Yet Due 1 - 30 days past due $52,000 $32,000 $13,000 1% 2% 8% 31 - 60 days past due What is the appropriate balance for Oceanside's Allowance for Impairment at December 31, 2019 O A. $1,560 O B. $2,160 O C, 2% of credit sales in 2019 O D. $95,000arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning