Concept explainers

1. and 2.

Prepare a schedule to show the impact of the assumed conversion of each convertible security on diluted earnings per share and also show the manner by which the securities that are included in the diluted earnings per share are ranked.

1. and 2.

Explanation of Solution

Earnings per share (EPS): The amount of net income available to each shareholder per common share outstanding is referred to as earnings per share (EPS).

Prepare a schedule to show the impact of the assumed conversion of each convertible security on diluted earnings per share.

| Convertible security | Impact in ($) | Ranking |

| 10.2% bonds (1) | $2.55 | 5 |

| 12.0% bonds (3) | $1.71 | 3 |

| 9.0% bonds (5) | $1.51 | 2 |

| 8.3% | $2.13 | 4 |

| 7.5% preferred stock (7) | $1.25 | 1 |

(Table 1)

Working notes:

(1) Calculate the impact of the 10.2% bonds on diluted earnings per share.

(2) Calculate the Premium on amortized bond for 20 year life:

(3) Calculate the impact of the 12.0% bonds on diluted earnings per share.

(4) Calculate the discount on amortized bond for 10 year life:

(5) Calculate the impact of the 9.0% bonds on diluted earnings per share.

(6) Calculate the impact of the 8.3% preferred stock on diluted earnings per share.

(7) Calculate the impact of the 7.5% preferred stock on diluted earnings per share.

3. and 4.

Calculate the basic earnings per share and diluted earnings per share.

3. and 4.

Explanation of Solution

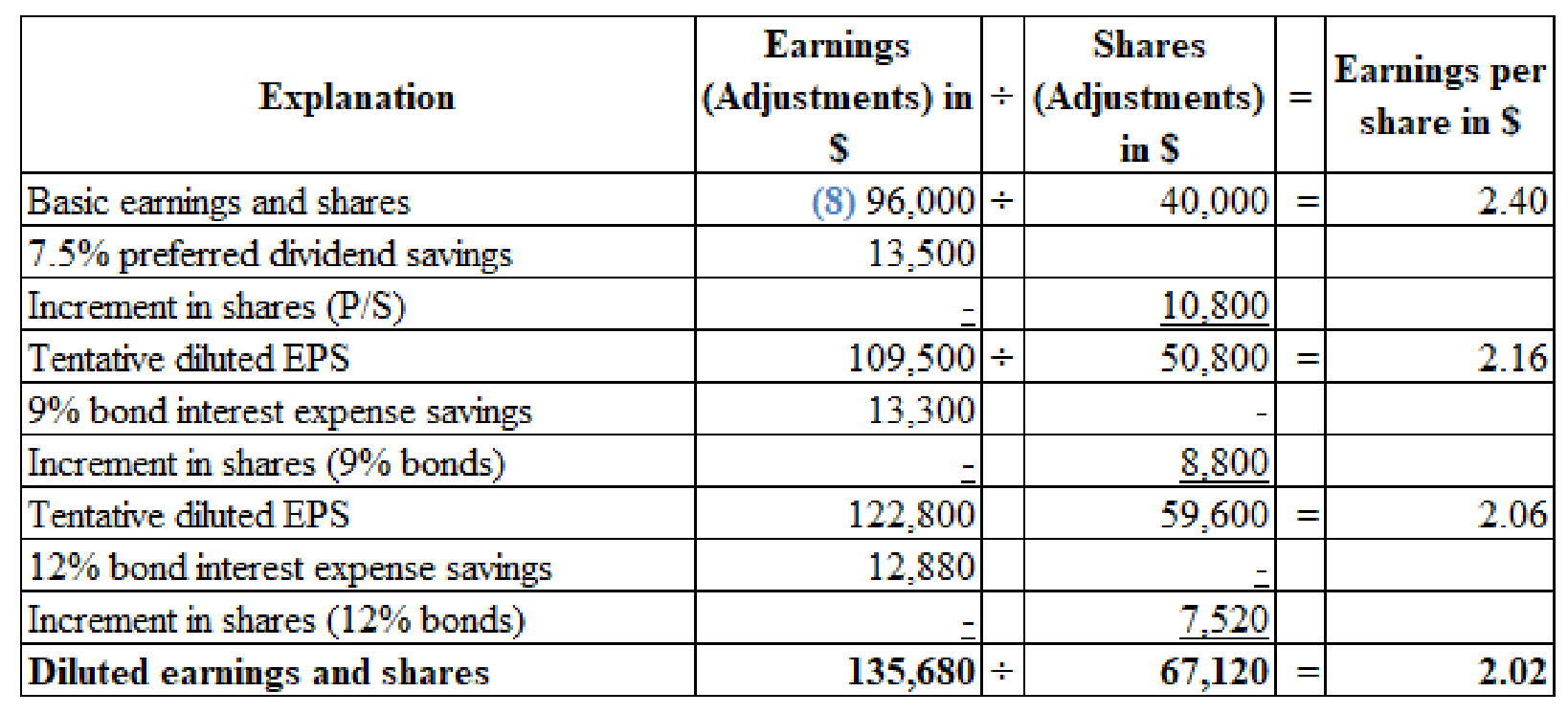

Calculate the basic earnings per share and diluted earnings per share.

(Figure 1)

Working notes:

(8) Calculate the numerator for the basic earnings per share:

5.

Identify the amount that will be reported as basic and diluted earnings per share for the year 2016.

5.

Explanation of Solution

The Company W must report an amount of $2.40 as basic earnings per share and $2.20 as diluted earnings per share in its 2016 income statement.

Want to see more full solutions like this?

Chapter 16 Solutions

EBK INTERMEDIATE ACCOUNTING: REPORTING

- Suppose Google, Inc. called its convertible debt in 2017. Assume the following related to the transaction. The 8%, $3,900,000 par value bonds were converted into 487,500 shares of $1 par value common stock on July 1, 2017. On July 1, there was $24,000 of unamortized discount applicable to the bonds, and the company paid an additional $33,000 to the bondholders to induce conversion of all the bonds. The company records the conversion using the book value method. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.)arrow_forwardOn January 2, 2015, Worth Co. issued at par $1,000,000 of 7% convertible bonds. Each $1,000 bond is convertible into 40 shares of common stock. No bonds were converted during 2015. Worth had 200,000 shares of common stock outstanding during 2015. Worth’s 2015 net income was $450,000 and the income tax rate was 30%. Worth’s earnings per share for 2015 would be (rounded to the nearest penny): A.$2.08.B. $2.25.C. $2.36.arrow_forwardDuring 2016, Oddie Corp. had net income of $300,000. Included in net income was after-tax interest expense of $20,000 on convertible bonds. The $200,000 face value of convertible bonds can be converted into common stock at the rate of 200 shares per $1,000 bond. Prior to the conversion, there were 400,000 shares of common stock outstanding. What is the amount of fully diluted earnings per share? $0.750 $0.636 $0.727 not determinable because the bonds are not dilutivearrow_forward

- (EPS with Convertible Bonds, Various Situations) In 2016, Chirac Enterprises issued, at par, 60 $1,000, 8% bonds, each convertible into 100 shares of common stock. Chirac had revenues of $17,500 and expenses other than interest and taxes of $8,400 for 2017. (Assume that the tax rate is 40%.) Throughout 2017, 2,000 shares of common stock were outstanding; none of the bonds was converted or redeemed.Instructions(a) Compute diluted earnings per share for 2017.(b) Assume the same facts as those assumed for part (a), except that the 60 bonds were issued on September 1, 2017 (rather than in 2016), and none have been converted or redeemed. Compute diluted earnings per share for 2017.(c) Assume the same facts as assumed for part (a), except that 20 of the 60 bonds were actually converted on July 1, 2017. Compute diluted earnings per share for 2017.arrow_forwardDaniel Company had 30,000 shares of common stock outstanding on January 1 and issued an additional 9,000 on August 1 of 2016. The company also has $100,000 of 8% convertible bonds outstanding during the year. Each $1,000 bond is convertible into 5 shares of common stock. Daniel had after-tax net income for the year of $160,000, and the tax rate was 30%. Required: Compute the appropriate earnings per share amount(s) to be reported on Daniel Company's 2016 income statement, and explain your answer.arrow_forwardClay Company had P600,000 convertible 8% bonds payable outstanding on June 30, 2016. Each P1,000 bond was convertible into 10 ordinary shares of P50 par value. On July 1, 2016, the interest was paid to bondholders, and the bonds were converted into ordinary shares, which had a fair value of P75 per share. The unamortized premium on these bonds was P12,000 at the date of conversion. No equity component was recognized when the bonds were originally issued. What is the increase in share capital as a result of the bond conversion? 300,000 306,000 450,000 600,000 What is the increase in share premium as a result of the bond conversion? 312,000 306,000 162,000 12,000arrow_forward

- On January 1, 2016, a company's balance sheet reports its investments in debt securities as follows: Assets Investment in trading securities Investment in AFS securities Investment in HTM securities Equity Accumulated other comprehensive income: Unrealized gains (losses) on AFS securities Additional information: a. The HTM securities are $210,000 face value securities purchased on January 1, 2014, at a yield of 4%. The securities have a 4-year total life and pay interest annually on December 31, at a coupon rate of 6%. $165,000 95,000 217,922 $4,500 b. The trading securities on hand on January 1 were sold in 2016 for $185,000. c. More trading securities were purchased for $105,000. They are still on hand at December 31, 2016, and have a fair value of $120,000. d. AFS securities, originally purchased for $27,000 with a carrying value of $24,000 as of January 1, 2016, were sold for $32,000. e. AFS securities on hand at December 31, 2016, have a fair value of $85,000 $20,000 $15,000…arrow_forwardStave Company invests $10,000,000 in 5% fixed rate corporate bonds on January 1, 2017. All the bonds are classified as available-for-sale and are purchased at par. At year-end, market interest rates have declined, and the fair value of the bonds is now $10,600,000. Interest is paid on January 1. Prepare journal entries for Stave Company to (a) record the transactionsrelated to these bonds in 2017, assuming Stave does not elect the fair option; and (b) record the transactions related to these bonds in 2017, assuming that Stave Company elects the fair value option to account for these bonds.arrow_forwardOriole Corporation earned net income of $235,000 in 2023 and had 100,000 common shares outstanding throughout the year. Also outstanding all year was $850,000 of 10% bonds that are convertible into 10,000 common shares. Oriole's tax rate is 35%. Calculate Oriole's 2023 diluted earnings per share. For simplicity, ignore the IFRS requirement to record the debt and equity components of the bonds separately. (Round answer to 2 decimal places, e.g. 15.25.) Diluted earnings per share Iarrow_forward

- On January 1, 2015, Glover Corporation issued $2,400,000 of 5-year, 8% bonds at 95. The bonds pay interest annually on January 1. By January 1, 2017, the market rate of interest for bonds of risk similar to those of Glover Corporation had risen. As a result, the market value of these bonds was $2,000,000 on January 1, 2017—below their carrying value. Joanna Glover, president of the company, suggests repurchasing all of these bonds in the open market at the $2,000,000 price. To do so, the company will have to issue $2,000,000 (face value) of new 10-year, 11% bonds at par. The president asks you, as controller, “What is the feasibility of my proposed repurchase plan?” Instructions (a) What is the carrying value of the outstanding Glover Corporation 5-year bonds on January 1, 2017? (Assume straight-line amortization.) (b) Prepare the journal entry to redeem the 5-year bonds on January 1, 2017. Prepare the journal entry to issue the new 10-year bonds. (c) Prepare a short memo to the…arrow_forwardAlciatore Company reported a net income of $150,000 in 2016. The weighted-average number of common shares outstanding for 2016 was 40,000. The average stock price for 2016 was $33. Assume an income tax rate of 40%. Required: For each of the following independent situations, indicate whether the effect of the security is antidilutive for diluted EPS. 1. 10,000 shares of 7.7% of $100 par convertible, cumulative preferred stock. Each share may be converted into two common shares. 2. 8% convertible 10-year, $500,000 of bonds, issued at face value. The bonds are convertible to 5,000 shares of common stock. 3. Stock options exercisable at $30 per share after January 1, 2018. 4. Warrants for 1,000 common shares with an exercise price of $35 per share. 5. A contingent agreement to issue 5,000 shares of stock to the company president if net income is at least $125,000 in 2017.arrow_forwardSunland Corporation earned net income of $340,000 in 2023 and had 100,000 common shares outstanding throughout the year. Also outstanding all year was $800,000 of 10% bonds that are convertible into 10,000 common shares. Sunland's tax rate is 30%. Calculate Sunland's 2023 diluted earnings per share. For simplicity, ignore the IFR$ requirement to record the debt and equity components of the bonds separately. (Round answer to 2 decimal places, e.g. 15.25.) Diluted earnings per share $arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning