Videos

1.

Prepare the

1.

Explanation of Solution

Investment: It refers to the process of using the currently held excess cash to earn profitable returns in future. The investments can be made in equity securities such as shares or debt securities such as bonds.

Prepare the journal entries in the books of Company D for the year 2016.

| Date | Account Title and Explanation | Debit | Credit |

| February 3, 2016 | Investment in Available-for-sale Securities | $36,000 | |

| Cash | $36,000 | ||

| (To record the purchase of Company B's 3000 shares) | |||

| April 1, 2016 | Investment in Available-for-sale Securities | $20,000 | |

| Interest income (1) | $600 | ||

| Cash | $20,600 | ||

| (To record the purchase of Incorporation S's bonds) | |||

| June 30, 2016 | Cash | $1,950 | |

| Dividend income | $750 | ||

| Interest income (2) | $1,200 | ||

| (To record the interest and dividend received) | |||

| September 1, 2016 | Investment in Available-for-sale Securities | $88,000 | |

| Cash | $88,000 | ||

| (To record the purchase of Company W's 4000 shares) | |||

| November 1, 2016 | Investment in Available-for-sale Securities | $30,000 | |

| Interest income (3) | $1,375 | ||

| Cash | $31,375 | ||

| (To record the purchase of Incorporation W's bonds) | |||

| December 1, 2016 | Cash | $1,650 | |

| Interest income (4) | $1,650 | ||

| (To record the interest received from Company E's bond) | |||

| December 1, 2016 | Cash | $30,300 | |

| Investment in Available-for-sale Securities | $30,000 | ||

| Gain on sale of Available-for-sale Securities | $300 | ||

| (To record the sale of Company E's bond on profit) | |||

| December 30, 2016 | Cash | $750 | |

| Dividend income | $750 | ||

| (To record the dividend received for Company B's share) | |||

| December 30, 2016 | Cash | $35,300 | |

| Loss on sale of Available-for-sale Securities | $700 | ||

| Investment in Available-for-sale Securities | $36,000 | ||

| (To record the sale of Company B's share on loss) | |||

| December 31, 2016 | Cash | $1,200 | |

| Interest income (5) | $1,200 | ||

| (To record the interest received from Incorporation S's bond) | |||

| December 31, 2016 | Allowance for change in fair value of investment | $4,200 | |

| Unrealized holding gain/loss: Available-for-sale securities (7) | $4,200 | ||

| (To adjust the allowance and the unrealized gain on holding the Securities) |

Table (1)

Working note (1):

Determine the amount of interest income paid by Company D.

Working note (2):

Calculate the amount of interest income received from Incorporation S’s bond.

Working note (3):

Calculate the amount of interest income paid by Company D.

Working note (4):

Calculate the amount of interest income received from Company E’s bond.

Working note (5):

Calculate the amount of interest income.

Working note (6):

Determine the fair value of investment in Corporation W’s stock.

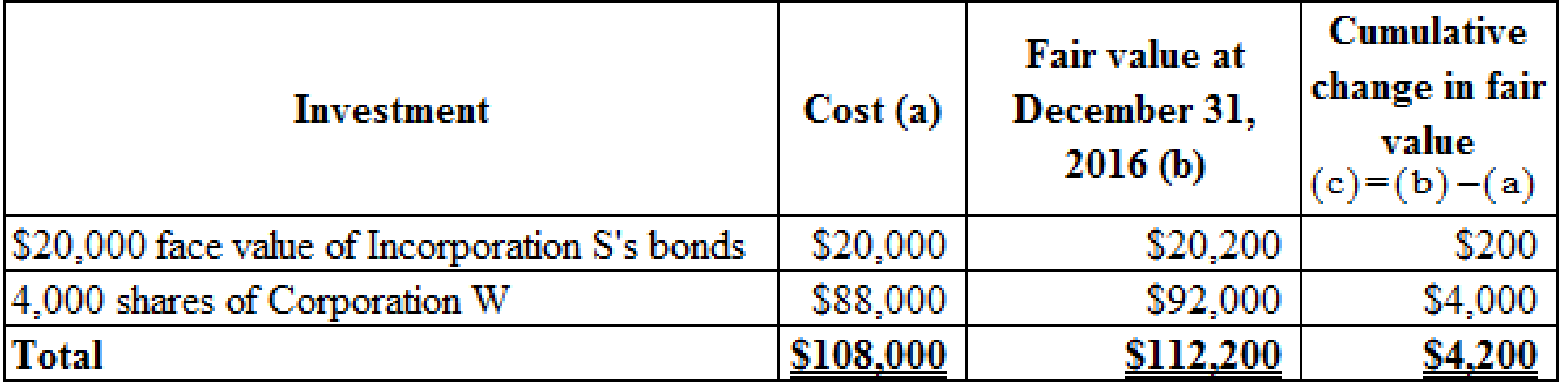

Working note (7):

Determine the net amount of unrealized gain or loss on available-for-sale securities as on December 31, 2016.

Table (2)

2.

Show the items of income or loss of Company D for the year ended December 31, 2016.

2.

Explanation of Solution

Show the items of income or loss of Company D for the year ended December 31, 2016.

| Particulars | Amount |

| Interest income (8) | $2,075 |

| Dividend income (9) | $1,500 |

| Loss on sale of available-for-sale securities | ($ 700) |

| Gain on sale of available-for-sale securities | $300 |

Table (3)

Working note (8):

Calculate the amount of interest income.

Working note (9):

Calculate the amount of dividend income.

3.

Show the carrying value of Company D’s investment in available-for-sale securities at its balance sheet at December 31, 2016.

3.

Explanation of Solution

Show the carrying value of Company D’s investment in available-for-sale securities at its balance sheet at December 31, 2016.

| Company D | |

| Balance sheet Statement (Partial) | |

| As at December 31, 2016 | |

| Assets | Amount |

| Current assets: | |

| Investment in available-for-sale securities (at cost) | $108,000 |

| Add : Allowance for change in fair value of investment | $4,200 |

| Investment in available-for-sale securities (at fair value) | $112,200 |

Table (4)

Want to see more full solutions like this?

Chapter 13 Solutions

EBK INTERMEDIATE ACCOUNTING: REPORTING

- Dunn Company recognized a 5,000 unrealized holding gain on investment in Starbuckss long-term bonds during 2019. The company classified its investment as an available-for-sale security. How would this information be reported on a statement of cash flows prepared using the indirect method?arrow_forwardPROBLEM E: You were engaged by SKT Company for the first time on February 15, 2018, to audit their financial statements as of and for the year ended December 31, 2017. In auditing their investment accounts, you decided to review the transactions and entries related to an investment in debt securities. On January 2, 2016, SKT acquired a 5-year 10% bond with a face value of P5,000,000 for P4,800,000. The entity incurred direct costs for P15,500, resulting to a yield rate of 11%. The business model of the entity for investing in debt securities is to collect contractual cash flows in the form of principal and interest on the outstanding principal, and to sell the financial assets. The bonds are quoted at 101 on December 31, 2016; 97 on December 31, 2017; and 99 on December 31, 2018. By the end of 2017, the balances in the statement of financial position of their Financial Asset – FVOCI and the related unrealized holding gain – OCI are P4,850,000 and P50,000, respectively. The entries…arrow_forwardAssume the following is a portion of the investment footnote from MetLife’s 2016 10-K report. Investment earnings are a crucial component of the financial performance of insurance companies such as MetLife, and investments comprise a large part of Metlife’s assets. MetLife accounts for its bond investments as available-for-sale securities. a. $223,926 million, $8,329 million gainb. $230,050 million, $6,124 million gainc. $223,926 million, $6,124 million gaind. $230,050 million, $2,205 million lossarrow_forward

- The following information is also available: 1. Current assets include cash P3,800, accounts receivables P18,500, note receivables (maturity date is on July 1,2023) P10,000 and land P12,000. 2. Long term investments include a P4,600 investment in fair value though other comprehensive income securitiesthat is expected to be sold in 2022 and a P9,000 investment in AllDay company bonds that are expected to be helduntil their December 31, 2029 maturity date. 3. Property and equipment include buildings costing P63,400, inventories costing P30,500 and equipment costingP29,600. 4. Intangible assets include patents that cost P8,200 and on which P2,300 amortization have accumulated, andtreasury shares that costs P1,800. 5. Other assets include prepaid insurance (which expires on November 30, 2022) P2,900, sinking fund for bondretirement P7,000 and trademarks that cost P5,200 and on which P1,500 amortization has accumulated. 6. Current liabilities include accounts payable P19,400, bonds payable…arrow_forwardThe following information is also available: 1. Current assets include cash P3,800, accounts receivables P18,500, note receivables (maturity date is on July 1,2023) P10,000 and land P12,000. 2. Long term investments include a P4,600 investment in fair value though other comprehensive income securitiesthat is expected to be sold in 2022 and a P9,000 investment in AllDay company bonds that are expected to be helduntil their December 31, 2029 maturity date. 3. Property and equipment include buildings costing P63,400, inventories costing P30,500 and equipment costingP29,600. 4. Intangible assets include patents that cost P8,200 and on which P2,300 amortization have accumulated, andtreasury shares that costs P1,800. 5. Other assets include prepaid insurance (which expires on November 30, 2022) P2,900, sinking fund for bondretirement P7,000 and trademarks that cost P5,200 and on which P1,500 amortization has accumulated. 6. Current liabilities include accounts payable P19,400, bonds payable…arrow_forwardThe following information is also available: 1. Current assets include cash P3,800, accounts receivables P18,500, note receivables (maturity date is on July 1, 2023) P10,000 and land P12,000. 2. Long term investments include a P4,600 investment in fair value though other comprehensive income securities that is expected to be sold in 2022 and a P9,000 investment in AllDay company bonds that are expected to be held until their December 31, 2029 maturity date. 3. Property and equipment include buildings costing P63,400, inventories costing P30,500 and equipment costing P29,600. 4. Intangible assets include patents that cost P8,200 and on which P2,300 amortization have accumulated, and treasury shares that costs P1,800. 5. Other assets include prepaid insurance (which expires on November 30, 2022) P2,900, sinking fund for bond retirement P7,000 and trademarks that cost P5,200 and on which P1,500 amortization has accumulated. 6. Current liabilities include accounts payable P19,400, bonds…arrow_forward

- The following was reported by Church Financial in its December 31, 2024, financial statements: Investments at FVTPL, December 31, 2023 Investments at FVTPL, December 31, 2024. Investment income or (loss) Additional information: 1. 2. 3. $13,400 18,300 (600) The investments at FVTPL are investments in equity securities held for trading purposes. Investment income or loss consists of: holding gain on the FVTPL investments of $3,100, and loss on sale of the FVTPL investments of $3,700. The carrying amount of the FVTPL investment sold was $4,900.arrow_forwardDIRECTION: Use the problem in solving the following requirementsInspiration Company had trading and nontrading investments held throughout 2014 and 2015. The nontrading investments are measured at fair value through other comprehensive income. The investments had a cost of P3,000,000 for trading and P3,000,000 for nontrading. The investments had the following fair value at year-end: December 31, 2014 December 31, 2015Trading 4,000,000 3,800,000Nontrading 3,200,000 3,700,000Prepare all journal entries for 2014 and 2015arrow_forwardData related to available-for sale securities for Aetna Corporation for the Year 2016 is provided below: Mark-to-market value of available-for-sale securities, Ending Amortized cost of available-for-sale securities, Beginning Purchases of available-for-sale securities during the year Amortized cost of available-for-sale securities, Ending $8,000 $1,200 $3,000 $1,550 Mark-to-market value of available-for-sale securities, Beginning $4,500 Additional information: No dividend revenue or interest revenue earned or received during the year. No securities were sold, and no securities were matured during the year. What would be the unrealized gain or loss for the year 2016? a. $500 Unrealized gain b. $1,300 Unrealized loss c. $2,150 Unrealized gain d. $1,800 Unrealized lossarrow_forward

- (a.) Prepare any journal entries you consider necessary, including year end entries (December 31), assuming these investments are managed to profit from changes in market interest rates (held for trading). Mayor Company doesn’t have debt investment before 2020. (b.) Prepare a partial statement of financial position showing the Investment account at December 31, 2020. (c.) If Mayor Company purchase the debt investment to collect the contractual cash flow (held the debt investment to maturity), explain how the journal entries would differ from those in part (a).arrow_forwardHelp Save & Exit Amalgamated General Corporation is a consulting firm that also offers financial services through its credit division. From time to time the company buys and sells securities. The following selected transactions relate to Amalgamated's investment activities during the last quarter of 2021 and the first month of 2022. The only securities held by Amalgamated at October 1, 2021 were $35 million of 10% bonds of Kansas Abstractors, Inc., purchased on May 1, 2021 at face value and held in Amalgamated's trading securities portfolio. The company's fiscal year ends on December 31. 2021 Oct. 18 Purchased 2 million shares of Millwork Ventures Company common stock for $55 million. Millwork has a total of 32 million shares issued. 31 Received semiannual interest of $2.1 million from the Kansas Abstractors bonds. 1 Purchased 10% bonds of Holistic Entertainment Enterprises at their $18 million face value, to be held until they mature in 2031. Semiannual interest is payable April 30…arrow_forward(Debt and Equity Investments) Cardinal Paz Corp. carries an account in its general ledger called Investments, which contained debits for investment purchases, and no credits, with the following descriptions. Feb. 1, 2017 Sharapova Company common stock, $100 par, 200 shares : $ 37,400 April 1 U.S. government bonds, 11%, due April 1, 2027, interest payableApril 1 and October 1, 110 bonds of $1,000 par each : 110,000 July 1 McGrath Company 12% bonds, par $50,000, dated March 1, 2017,purchased at 104 plus accrued interest, interest payable annually on March 1, due March 1, 2037 : 54,000 Instructions(Round all computations to the nearest dollar.)(a) Prepare entries necessary to classify the amounts into proper accounts, assuming that the debt securities are classified as available-for-sale.(b) Prepare the entry to record the accrued interest and the amortization of premium on December 31, 2017, using the straight-line method.(c) The fair values of the investments on December…arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning