Horngren's Accounting (12th Edition)

12th Edition

ISBN: 9780134486444

Author: Tracie L. Miller-Nobles, Brenda L. Mattison, Ella Mae Matsumura

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 12, Problem P12.36BPGB

Accounting for the liquidation of a

Learning Objective 6

2. Loss on Disposal $55,000

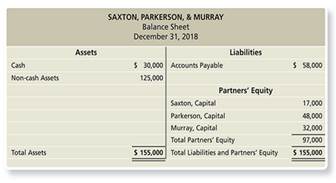

The partnership of Saxton, Parkerson, & Murray has experienced operating losses for three consecutive years. The partners—who have shared profits and losses in the ratio of Saxton, 10%; Parkerson, 65%; and Murray, 25%—are liquidating the business. They ask you to analyze the effects of liquidation. They present the following condensed partnership balance sheet at December 31, 2018:

Requirements

1. Assume the non-cash assets are sold for $170,000. Journalize the liquidation transactions.

2. Assume the non-cash assets are sold for $70,000. Journalize the liquidation transactions.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Can I please get help with this practice question? 6.1

Ries, Bax, and Thomas invested $48,000, $64,000, and $72,000, respectively, in a partnership. During its first calendar year, the firm earned $416,100.

Required:

Prepare the entry to close the firm’s Income Summary account as of its December 31 year-end and to allocate the $416,100 net income under each of the following separate assumptions.

1. The partners did not agree on a plan, and therefore share income equally.

Record the entry to close the income summary account assuming the partners did not agree on a plan, and therefore share income equally.

Note: Enter debits before credits.

Date

General Journal

Debit

Credit

December 31

Can I please get help wtih this question?6.3

Ries, Bax, and Thomas invested $48,000, $64,000, and $72,000, respectively, in a partnership. During its first calendar year, the firm earned $416,100.

Required:

Prepare the entry to close the firm’s Income Summary account as of its December 31 year-end and to allocate the $416,100 net income under each of the following separate assumptions.

1. The partners did not agree on a plan, and therefore share income equally.

Problem Solving :

a. Gulane, Tormis and Sailadin decided to Liquidate their partnership in June 30, 2018.

The partners shared profits and losses in the ratio 2:2:1 respectively. The firms post

closing trial balance follows:

Gulane, Tormis and Sailadin

Post Closing Trial Balance

June 30, 2018

Account Name

Debit

Credit

P 419,170

Cash

Merchandise Inventory

Other Assets

Accounts Payable

Gulane Capital

Tormis Capital

Sailadin, Capital

612,300

472,680

P 131,350

561,600

436.800

374,400

1.504,150

1.504.150

The merchandise inventory and the other assets were sold for P 582,800 and P

550,900 respectively.

Required : Prepare the Liquidation journal entries.

Chapter 12 Solutions

Horngren's Accounting (12th Edition)

Ch. 12 - Prob. 1QCCh. 12 - Prob. 2QCCh. 12 - Prob. 3QCCh. 12 - Which financial statement shows the changes in...Ch. 12 - Prob. 5QCCh. 12 - Prob. 6QCCh. 12 - Prob. 7QCCh. 12 - Peter and Steve admit Meredith to their...Ch. 12 - Prob. 9QCCh. 12 - Prob. 10QC

Ch. 12 - Prob. 1RQCh. 12 - Prob. 2RQCh. 12 - Prob. 3RQCh. 12 - Prob. 4RQCh. 12 - Prob. 5RQCh. 12 - Prob. 6RQCh. 12 - Prob. 7RQCh. 12 - Prob. 8RQCh. 12 - Prob. 9RQCh. 12 - Prob. 10RQCh. 12 - Prob. 11RQCh. 12 - Prob. 12RQCh. 12 - Prob. 13RQCh. 12 - Prob. 14RQCh. 12 - Prob. 15RQCh. 12 - What are the three steps involved in liquidation...Ch. 12 - Prob. 17RQCh. 12 - Prob. S12.1SECh. 12 - Prob. S12.2SECh. 12 - Prob. S12.3SECh. 12 - Prob. S12.4SECh. 12 - Prob. S12.5SECh. 12 - S12-6 Accounting for the admission of a new...Ch. 12 - Accounting for the admission of a new partner...Ch. 12 - Prob. S12.8SECh. 12 - Prob. S12.9SECh. 12 - Prob. S12.10SECh. 12 - Prob. S12.11SECh. 12 - Prob. S12.12SECh. 12 - Prob. E12.13ECh. 12 - Prob. E12.14ECh. 12 - Prob. E12.15ECh. 12 - Prob. E12.16ECh. 12 - Prob. E12.17ECh. 12 - Prob. E12.18ECh. 12 - Prob. E12.19ECh. 12 - Prob. E12.20ECh. 12 - Prob. E12.21ECh. 12 - Prob. E12.22ECh. 12 - Determining characteristics of a partnership and...Ch. 12 - Prob. P12.24APGACh. 12 - Prob. P12.25APGACh. 12 - Prob. P12.26APGACh. 12 - Prob. P12.27APGACh. 12 - Prob. P12.28APGACh. 12 - Prob. P12.29APGACh. 12 - Prob. P12.30APGACh. 12 - Prob. P12.31BPGBCh. 12 - Prob. P12.32BPGBCh. 12 - Prob. P12.33BPGBCh. 12 - Prob. P12.34BPGBCh. 12 - Prob. P12.35BPGBCh. 12 - Accounting for the liquidation of a partnership...Ch. 12 - Prob. P12.37BPGBCh. 12 - Prob. P12.38BPGBCh. 12 - Prob. P12.39CTCh. 12 - P12-40 Accounting for partner contributions,...Ch. 12 - Prob. 12.1TIATCCh. 12 - Prob. 12.1DCCh. 12 - Prob. 12.2DCCh. 12 - Prob. 12.1EICh. 12 - Prob. 12.1FSC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Make-up assignment Partnership Dissolution Instruction: Prepare the answers and solutions in written form using a clean paper (e.g. Yellow pad, bond paper, notebook etc.) and submit a snapshot in CANVAS. Problem 1. A and B are partners in an electrical repair business. Their respective capital balances are P90,000 and P50,000, and they share profits or losses equally. Because the partners are confronted with personal financial problems, they decided to admit a new partner to the partnership. After an extensive interviewing process, they elect to admit C into the partnership. Required: Prepare the journal entry to record the admission of C into the partnership and determine capital balances of A, B and C under each of the following condition: 1. Cacquires one-fourth interest of A's capital interest by paying 30,000 directly to him. 2. Cacquires one-fifth interest of each A and B capital interest. A receives P25,000 and B receives P15,000 directly from C. 3. Cacquires a one-fifth…arrow_forwardSECTION: PROFESSOR: Problem #14 Admission by Investment of Assets On Jan. 31, 2019, Partners Abad, Ramos and Cammayo had the following loan and capital account balances (after closing entries for Jan.): Loan receivable from Abad P 20,000 dr 60,000 cr Abad payable to Cammayo Abad, Capital Ramos, Capital Cammayo, Capital 30,000 dr 120,000 cr 70,000 cr The partnership's income-sharing ratio was Abad, 50%; Ramos, 20%; and Cammayo, 30%. On Jan. 31, 2019, Gonzales was admitted to the partnership for a 20% interest in total capital of the partnership in exchange for an investment of P40,000 cash. Prior to Gonzales's admission, the existing partners agreed to increase the carrying amount of the partnership's inventories to current fair value, a P60,000 increase. Required: Prepare the journal entries the increase in inventories and the admission of Gonzales.arrow_forwardInstruction: Prepare the answers in written form using a clean paper (e.g. Yellow pad, bond paper, notebook etc.) and submit a snapshot in CANVAS. Assume A, B, C and D are partners sharing profits 40%, 20%, 20%, 20%, respectively. On January 1, 2020, they agree to liquidate. A balance sheet prepared on this date is shown as follows: Assets Liabilities and Capital Non- Cash assets P 181,800 Liabilities P 84,000 A, Loan 6,000 D, Loan 3,000 A, Capital 26,400 В, Сapital C, Capital D, Capital 25,800 20,400 16,200 Total P 181,800 P 181,800 Results of liquidation are summarized below: Month Proceeds Book Value Liquidation exp. Cash withheld January P72,000 P90,000 P1,200 P4,800 February 21,600 30,000 1,320 1,800 March 19,200 24,000 1,440 1,200 April 6,000 19,800 4,800 600 May 2,400 18,000 960 Required: Prepare the statement of liquidation and related schedule of safe payment for the month of January to May 2020 and determine payment to partners for every month.arrow_forward

- QUESTION 31. Frame and French are in partnership sharing profits and losses in the ratio 3/5:2/5, respectively. The following is their trial balance as at 30 September 2015. Dr Cr TZS TZS Buildings (cost TZS 210,000) 160,000 Fixtures at cost 8,200 Provision for depreciation: Fixtures 4,200 Debtors 61,400 Creditors 26,590 Cash at bank 6,130 Stock at 30 September 2014 62,740 Sales 363,111 Purchases 210,000 Carriage outwards 3,410 Discounts allowed 620 Loan interest: P Prince 3,900 Office expenses 4,760 Salaries and wages 57,809 Bad debts 1,632 Provision for doubtful debts 1,400 Loan from P Prince 65,000 Capitals: Frame 100,000 French 75,000 Current accounts: Frame 4,100 French 1,200 Drawings: Frame 31,800 French 28,200 640,601 640,601 Avitus Dominick: Msc Finance and Investment, CPA (T ) & BAC (0714-336097)arrow_forwardExercise 3-8. Distribution of Net Income to partners On March 1, 2023 Glenda and Harry formed GH Partnership with initial investment of P800,000 and P1,200,000, respectively. Glenda is appointed as the managing partner. The articles of co-partnership provides that profit or loss shall be distributed accordingly: 10% interest on original capital contribution ratio. Monthly salary of P10,000 and P5,000 respectively for Glenda and Harry. . Glenda shall be entitled to bonus equivalent to 10% of net income after interest, and salary. The remainder shall be distributed in ratio of 4:6 for Glenda and Harry, respectively. ● For the year ended December 31, 2023, the partnership reported net income of P1,000,000. Required: Compute for the share in net income of Glenda for the year ended December 31, 2023.arrow_forwardHomework Activity 1 A, B and C are in Partnership sharing profits and losses in the ratio of 2:1:1. During the year ending 31st Dec 2019, the business made a profit of RO 64,000 before providing Interest on capital : A 2,000, B 1500, C 1000 Interest on drawings: A 200, B 150, C 100 Salary to Partners A 500 B 700 C 600 Commission to Partners A 200 B 300 C 400 Prepare a profit and loss appropriation account to show the distribution of profit among the partners.arrow_forward

- Partnership A, B and C is a law firm. You have been engaged as accountant to prepare financial statements for the year ended Dec. 31, 2019 Partnerships profits are alllocated based fist on salaries,then on interest on opening capital balances then on fixed ratio. Salary allocation amount are A $100000 B $100000 C $160000 Opening capital balances A $70000 B $60000 C $70000 Interest rate is: 5% Fixed ratio is A 3 B 2 C 5 required Prepare year end adjusting entries Allocate partnership profit or loss to each partner Prepare adjusting entry and complete trial balnce Prepare income statement and statement of partners capital for the year ended Dec. 31, 2019 and a balance sheet for Dec.31arrow_forwardProblem #2 (adapted) Lester and Stephen formed a partnership with capital contributions of P300,000 and P700,000, respectively. During its first year of operations, the partnership suffered a loss of P50,000. Prepare a schedule showing the division of profit between the partners under each of the following independent assumptions: 1. Loss is agreed to be divided equally. 2. There is no profit or loss sharing agreement. 3. A monthly salary of P8,000 will be given to Lester and the balance divided in the ratio of their capital balances. 4. A monthly salary of P8,000 will be given to Lester, 6% interest will be allowed on the capital balances of each partner; and the balance divided equally.arrow_forwardThe partnership of Donald, Healey & Jaguar has experienced operating losses. The partners—who have shared profits and losses in the ratio of Donald, 10%; Healey, 30%; and Jaguar, 60%—are liquidating the business. They ask you to analyze the effects of liquidation and present the following partnership balance sheet at December 31, end of the current year: Requirements 1. Prepare a summary of liquidation transactions (as illustrated in Exhibit 12-5). The noncash assets are sold for $192,000. 2. Journalize the liquidation transactions.arrow_forward

- Can I please get help with practice 6.4 Required information Skip to question [The following information applies to the questions displayed below.] Ries, Bax, and Thomas invested $48,000, $64,000, and $72,000, respectively, in a partnership. During its first calendar year, the firm earned $416,100. Required: Prepare the entry to close the firm’s Income Summary account as of its December 31 year-end and to allocate the $416,100 net income under each of the following separate assumptions. Appropriation of profits General Journal Allocate $416,100 net income in the ratio of their beginning capital investments.Note: Do not round intermediate calculations. Round final answers to the nearest whole dollar. Supporting Computations Percentage of Total Equity × Income Summary Allocated Income to Capital Ries × Bax × Thomas × Record the entry to close the income summary account assuming the partners have…arrow_forwardSTATEMENT OF PARTNER SHIP LIQUIDATION WITH LOSS After several years of operations, the partnership of Delco, Smith, and Walker is to be liquidated. After making closing entries on March 31, 20--, the following accounts remain Open. The noncash assets are sold for 165,000. Profits and losses are shared equally. REQUIRED 1. Prepare a statement of partnership liquidation for the period April 115, 20--, showing the following: (a) The sale of noncash assets on April 1 (b) The allocation of any gain or loss to the partners on April 1 (c) The payment of the liabilities on April 12 (d) The distribution of cash to the partners on April 15 2. Journalize these four transactions in a general journal.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:9781337679503

Author:Gilbertson

Publisher:Cengage

College Accounting, Chapters 1-27

Accounting

ISBN:9781337794756

Author:HEINTZ, James A.

Publisher:Cengage Learning,

Financial Accounting: The Impact on Decision Make...

Accounting

ISBN:9781305654174

Author:Gary A. Porter, Curtis L. Norton

Publisher:Cengage Learning

Operating Loss Carryback and Carryforward; Author: SuperfastCPA;https://www.youtube.com/watch?v=XiYhgzSGDAk;License: Standard Youtube License