Concept explainers

Videos

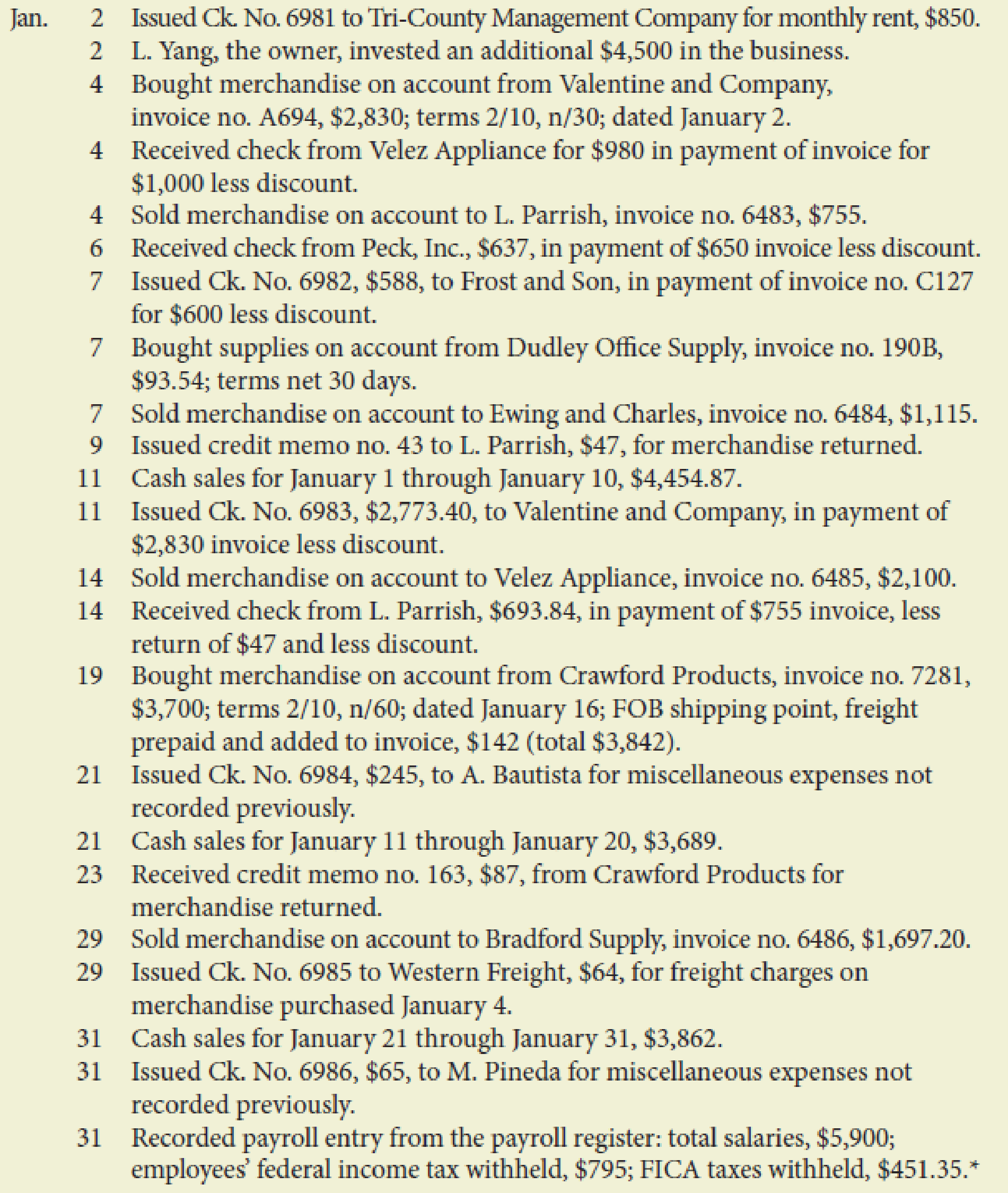

The following transactions were completed by Yang Restaurant Equipment during January, the first month of this fiscal year. Terms of sale are 2/10, n/30. The balances of the accounts as of January 1 have been recorded in the general ledger in your Working Papers or in CengageNow. Yang Restaurant Equipment does not track cash sales by customer. If you are using the form-based approach with QuickBooks or general ledger, select “Cash Sales” as the customer for all cash sales transactions.

Required

- 1. Record the transactions for January using a general journal, page 1. Assume the periodic inventory method is used.*

* If using QuickBooks, record transactions using either the

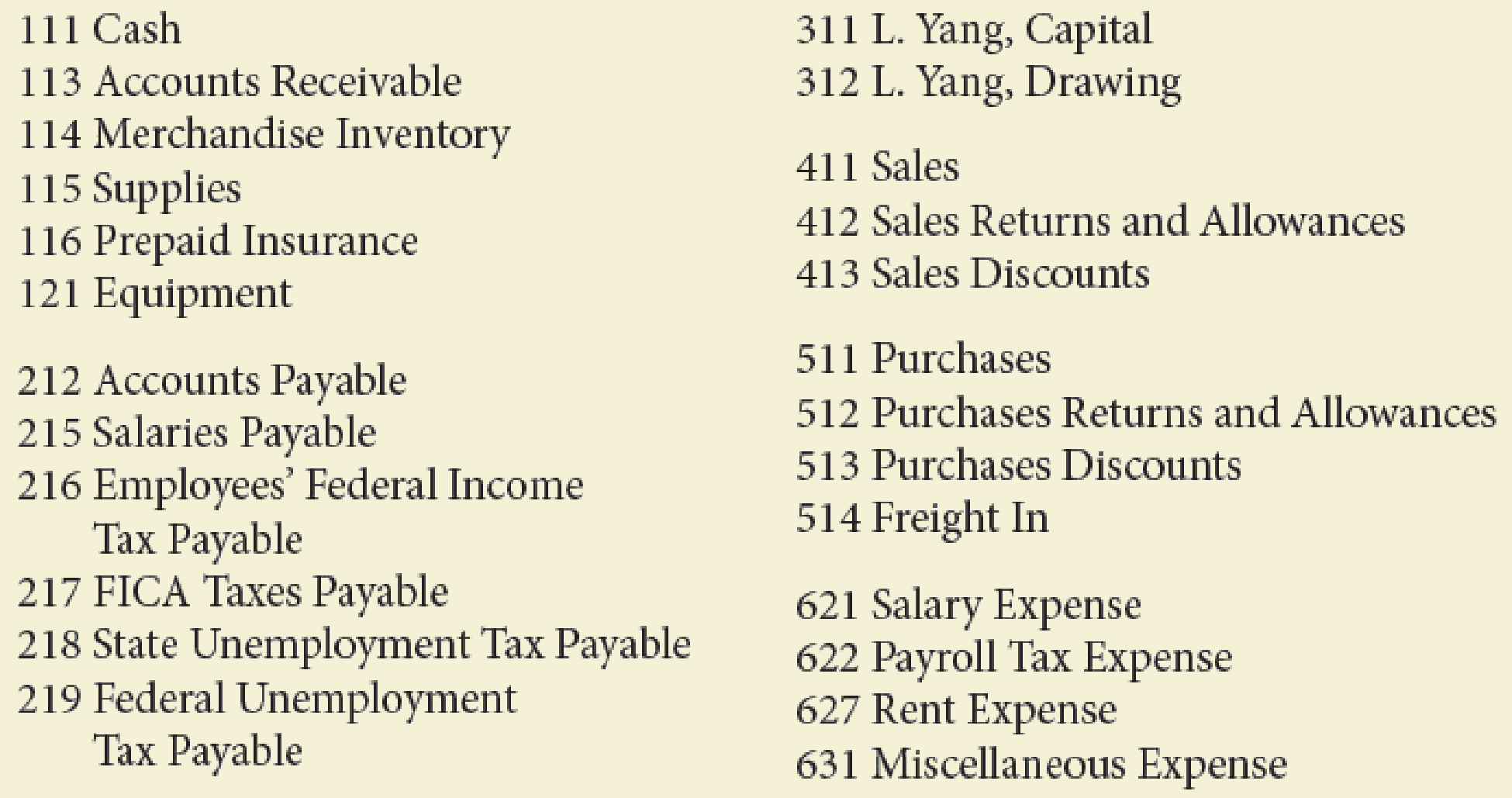

The chart of accounts is as follows:

- 2.

Post daily all entries involving customer accounts to the accounts receivable ledger.* - 3. Post daily all entries involving creditor accounts to the accounts payable ledger.*

- 4. Post daily the general journal entries to the general ledger. Write the owner’s name in the Capital and Drawing accounts.*

- 5. Prepare a

trial balance . - 6. Prepare a schedule of accounts receivable (A/R Aging Detail report in QuickBooks) and a schedule of accounts payable (A/P Aging Detail report in QuickBooks). Do the totals equal the balances of the related controlling accounts?

*If using QuickBooks or general ledger, ignore Steps 2, 3, and 4.

1.

Journalize the transaction in the general journal using periodic inventory method.

Explanation of Solution

General journal is a record of financial transaction. The transactions are recorded in the journal prior to posting them to the accounts in the general ledger.

Periodic inventory system: The method or system of recording the transactions related to inventory occasionally or periodically are referred to as periodic inventory system.

Journalize the transaction in general journal:

| General journal | Page:1 | ||||

| Date | Description | Post ref. | Debit ($) | Credit($) | |

| 20___ | |||||

| Jan. | 2 | Rent expense | 627 | 850 | |

| Cash | 111 | 850 | |||

| (Record rent paid by cash, Ck.no.6981) | |||||

| 2 | Cash | 111 | 4,500 | ||

| Mr. L capital | 311 | 4,500 | |||

| (Record additional capital invested | |||||

| by owner) | |||||

| 4 | Purchases | 212 | 376 | ||

| Accounts payable, V company | 512 | 376 | |||

| (Record purchase of merchandise from | |||||

| V company, invoice no: A694) | |||||

| 4 | Cash | 111 | 980 | ||

| Sales discounts | 413 | 20 | |||

| Accounts receivable, V company | 113 | 1,000 | |||

| (Record received check from V company | |||||

| for $980 in payment of invoice) | |||||

| 4 | Accounts receivable, L company | 113 | 755 | ||

| Sales | 411 | 755 | |||

| (Record merchandise sold on account | |||||

| to L company) | |||||

| 6 | Cash | 111 | 637 | ||

| Sales discount | 413 | 13 | |||

| Accounts receivable, P company | 113 | 650 | |||

| (Record received check from P company | |||||

| for $637 in payment of invoice) | |||||

| 7 | Accounts payable, F and S | 212 | 600 | ||

| Purchase discounts | 513 | 12 | |||

| Cash | 111 | 588 | |||

| (Record issued check to F and S in | |||||

| payment of invoice no: C127) | |||||

| 7 | Supplies | 625 | 93.54 | ||

| Accounts payable, D company | 212 | 93.54 | |||

| (Record purchase of supplies on account | |||||

| from D company) | |||||

| 7 | Accounts receivable, E and C | 113 | 1,115 | ||

| Sales | 411 | 1,115 | |||

| (Record merchandise sold to E and C) | |||||

Table (1)

| General journal | Page:2 | ||||

| Date | Description | Post ref. | Debit ($) | Credit($) | |

| 20___ | 9 | Sales returns and allowances | 412 | 47 | |

| Jan. | Accounts receivable | 113 | 47 | ||

| (Record issued credit memo to E and C for return of merchandise) | |||||

| 11 | Cash | 111 | 4,454.87 | ||

| Sales | 411 | 4,454.87 | |||

| (record cash sales) | |||||

| 11 | Accounts payable, V company | 212 | 2,830 | ||

| Cash | 111 | 2,773.40 | |||

| Purchase discounts | 513 | 56.6 | |||

| (Record issued check to V company for$2,773.40 in payment of invoice) | |||||

| 14 | Accounts receivable, V company | 113 | 2,100 | ||

| Sales | 411 | 2,100 | |||

| (Record merchandise sold to V company) | |||||

| 14 | Cash | 11 | 693.84 | ||

| Sales discount | 413 | 14.16 | |||

| Accounts receivable, L company | 113 | 708 | |||

| (Record received check from L company for $980 in payment of invoice) | |||||

| 19 | Purchases | 511 | 3,700 | ||

| Freight in | 514 | 142 | |||

| Accounts payable, C company | 212 | 3,842 | |||

| (Record purchase of merchandise on account from C company) | |||||

| 21 | Miscellaneous expense | 631 | 245 | ||

| Cash | 111 | 245 | |||

| (Record issued check to A.B company for | |||||

| $245 in payment of invoice) | |||||

| 21 | Cash | 111 | 3,689 | ||

| Sales | 411 | 3,689 | |||

| (Record cash sales) | |||||

| 23 | Accounts payable | 212 | 87 | ||

| Purchase returns and allowances | 512 | 87 | |||

| (Record received credit memo from C company) | |||||

Table (2)

| General journal | Page:3 | ||||

| Date | Description | Post ref. | Debit ($) | Credit($) | |

| 20___ | |||||

| Jan. | 29 | Accounts receivable, B company | 113 | 1,697.2 | |

| Sales | 411 | 1,697.2 | |||

| (Record sale of merchandise to B company) | |||||

| 29 | Freight in | 514 | 64 | ||

| Cash | 111 | 64 | |||

| (Record freight in charges) | |||||

| 31 | Cash | 111 | 3,862 | ||

| Sales | 411 | 3,862 | |||

| (Record cash sales) | |||||

| 31 | Miscellaneous expense | 631 | 65 | ||

| Cash | 111 | 65 | |||

| (Record payment of miscellaneous expense to M company) | |||||

| 31 | Salary expense | 621 | 5,900 | ||

| Employees Federal Income Tax payable | 216 | 795 | |||

| FICA Tax payable | 217 | 451.35 | |||

| Salaries payable | 215 | 4,653.65 | |||

| (Record salaries paid) | |||||

| 31 | Payroll tax expense | 622 | 764.05 | ||

| FICA Tax payable | 217 | 451.35 | |||

| State Unemployment Tax payable | 218 | 265.50 | |||

| Federal Unemployment Tax payable | 219 | 47.20 | |||

| (Record payment of payroll tax expense) | |||||

| 31 | Salaries payable | 215 | 4,653.65 | ||

| Cash | 111 | 4,653.65 | |||

| (Record payment of salaries) | |||||

| 31 | Mr. L , drawing | 312 | 1,000 | ||

| Cash | 111 | 1,000 | |||

| (Record Mr. L withdraw cash for personal use) | |||||

Table (3)

2.

Record the entries from customer accounts to the accounts receivable ledger.

Explanation of Solution

Account receivable: The amount of money to be received by a company for the sale of goods and services to the customers is referred to as account receivable.

Entries from customer accounts to the accounts receivable ledger:

| Accounts receivable ledger | ||||||

| Name: B company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20___ | ||||||

| Jan | 29 | 3 | 1,697.2 | 1,697.2 | ||

| Name: E and C company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20___ | ||||||

| Jan | 7 | 1 | 1,115 | 1,115 | ||

| Name: L company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20___ | ||||||

| Jan | 4 | 1 | 755 | 755 | ||

| 9 | 2 | 47 | 708 | |||

| 14 | 2 | 708 | 0 | |||

| Name: P company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20___ | ||||||

| Jan | 1 | Balance | 650 | |||

| 6 | 1 | 650 | 0 | |||

| Name: V company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20___ | ||||||

| Jan | 1 | Balance | 1,000 | |||

| 4 | 1 | 1,000 | 0 | |||

| 14 | 2 | 2,100 | 2,100 | |||

Table (4)

3.

Record the entries from creditor accounts to the accounts payable ledger.

Explanation of Solution

Account payable: The amount of money to be paid by a company for the purchase of goods and services from the seller is referred to as account payable.

Entries from creditor accounts to the accounts payable ledger:

| Accounts payable ledger | ||||||

| Name: C company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20___ | ||||||

| Jan | 19 | 2 | 3,842 | 3,842 | ||

| 23 | 2 | 87 | 3,755 | |||

| Name: D company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20___ | ||||||

| Jan | 7 | 1 | 93.5 | 93.5 | ||

| Name: F and sons | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20___ | ||||||

| Jan | 1 | Balance | 600 | |||

| 7 | 1 | 600 | 0 | |||

| Name: V company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20___ | ||||||

| Jan | 4 | 1 | 2,830 | 2,830 | ||

| 11 | 2 | 2,830 | 0 | |||

Table (5)

4.

Post the prepared general journal entries to the general ledger.

Explanation of Solution

Posting of transaction: The process of transferring the journalized transactions into the accounts of the ledger is known as posting of transaction.

Posting the transaction from general journal entries to general ledger:

| General ledger | |||||||||||||||||

| Account: Cash | Account No:111 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 1 | Balance | 8,740 | ||||||||||||||

| 2 | 1 | 850 | 7,890.00 | ||||||||||||||

| 2 | 1 | 4,500 | 12,390.00 | ||||||||||||||

| 4 | 1 | 980 | 13,370 | ||||||||||||||

| 6 | 1 | 637 | 14,007 | ||||||||||||||

| 7 | 1 | 588 | 13,419 | ||||||||||||||

| 11 | 2 | 4,454.87 | 17,873.87 | ||||||||||||||

| 11 | 2 | 2,773.40 | 15,100.47 | ||||||||||||||

| 14 | 2 | 693.84 | 15,794.31 | ||||||||||||||

| 21 | 2 | 245 | 15,549.31 | ||||||||||||||

| 21 | 2 | 3,689 | 19,238.31 | ||||||||||||||

| 29 | 3 | 64 | 19,174.31 | ||||||||||||||

| 31 | 3 | 3,862 | 23,036.31 | ||||||||||||||

| 31 | 3 | 65 | 22,971.31 | ||||||||||||||

| 31 | 3 | 4,653.65 | 18,317.66 | ||||||||||||||

| 31 | 3 | 1,000 | 17,317.66 | ||||||||||||||

| Account: Accounts receivable | Account No:113 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 1 | Balance | 1650 | ||||||||||||||

| 4 | 1 | 1000 | 650 | ||||||||||||||

| 4 | 1 | 755 | 1,405 | ||||||||||||||

| 6 | 1 | 650 | 755 | ||||||||||||||

| 7 | 1 | 1,115 | 1,870 | ||||||||||||||

| 9 | 2 | 47 | 1,823 | ||||||||||||||

| 14 | 2 | 2,100 | 3,923 | ||||||||||||||

| 14 | 2 | 708 | 3,215 | ||||||||||||||

| 29 | 3 | 1,697.20 | 4,912.20 | ||||||||||||||

| Account: Merchandise inventory | Account No:114 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 1 | Balance | 20,584 | ||||||||||||||

| Account: Suppliers | Account No:115 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 1 | Balance | 592 | ||||||||||||||

| 7 | 1 | 93.54 | 685.54 | ||||||||||||||

| Account: Prepaid insurance | Account No:116 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 1 | Balance | 390 | ||||||||||||||

| Account: Equipment | Account No:121 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 1 | Balance | 3,644 | ||||||||||||||

| Account: Accounts payable | Account No:212 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 1 | Balance | 600 | ||||||||||||||

| 4 | 1 | 2,830 | 3,430 | ||||||||||||||

| 7 | 1 | 600 | 2,830 | ||||||||||||||

| 7 | 1 | 93.54 | 2,923.54 | ||||||||||||||

| 11 | 2 | 2,830 | 93.54 | ||||||||||||||

| 19 | 2 | 3,842 | 3,935.54 | ||||||||||||||

| 23 | 2 | 87 | 3,848.54 | ||||||||||||||

| Account: Salaries payable | Account No:215 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 31 | 3 | 4,653.65 | 4,653.65 | |||||||||||||

| 31 | 3 | 4,653.65 | 0 | ||||||||||||||

| Account: Employees federal income tax payable | Account No:216 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 31 | 3 | 795 | 795 | |||||||||||||

| Account: FICA tax payable | Account No:217 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 31 | 3 | 451.35 | 451.35 | |||||||||||||

| 31 | 3 | 451.35 | 902.7 | ||||||||||||||

| Account: State unemployment tax payable | Account No:218 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 31 | 3 | 265.5 | 265.5 | |||||||||||||

| Account: Federal unemployment tax payable | Account No:219 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 31 | 3 | 47.2 | 47.2 | |||||||||||||

| Account: Mr. Y capital | Account No:311 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 1 | Balance | 35,000 | ||||||||||||||

| 2 | 1 | 4,500 | 39,500 | ||||||||||||||

| Account: Mr. Y Drawing | Account No:312 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 31 | 3 | 1,000 | 1,000 | |||||||||||||

| Account: Sales | Account No:411 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 4 | 1 | 755 | 755 | |||||||||||||

| 7 | 1 | 1,115 | 1,870 | ||||||||||||||

| 11 | 2 | 4,454.87 | 6,324.87 | ||||||||||||||

| 14 | 2 | 2,100 | 8,424.87 | ||||||||||||||

| 21 | 2 | 3,689 | 12,113.87 | ||||||||||||||

| 29 | 3 | 1,697.20 | 13,811.07 | ||||||||||||||

| 31 | 3 | 3,862 | 17,673.07 | ||||||||||||||

| Account: Sales return and allowance | Account No:412 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 9 | 2 | 47 | 47 | |||||||||||||

| Account: Sales discounts | Account No:413 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 4 | 1 | 20 | 20 | |||||||||||||

| 6 | 1 | 13 | 33 | ||||||||||||||

| 14 | 2 | 14.16 | 47.16 | ||||||||||||||

| Account: Purchases | Account No:511 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 4 | 1 | 2,830 | 2,830 | |||||||||||||

| 19 | 2 | 3,700 | 6,530 | ||||||||||||||

| Account: Purchases returns and allowances | Account No:512 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 23 | 2 | 87 | 87 | |||||||||||||

| Account: Purchase discounts | Account No:513 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 7 | 1 | 12 | 12.0 | |||||||||||||

| 11 | 2 | 56.6 | 68.6 | ||||||||||||||

| Account: Freight in | Account No:514 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 19 | 2 | 142 | 142 | |||||||||||||

| 29 | 3 | 64 | 206 | ||||||||||||||

| Account: Salary expense | Account No:621 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 31 | 3 | 5,900 | 5,900 | |||||||||||||

| Account: Payroll tax expense | Account No:622 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 31 | 3 | 764.05 | 764.05 | |||||||||||||

| Account: Rent expense | Account No:627 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 2 | 1 | 850 | 850 | |||||||||||||

| Account: Miscellaneous expense | Account No:631 | ||||||||||||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||||||||||||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||||||||||||

| Jan | 21 | 2 | 245 | 245 | |||||||||||||

| 31 | 3 | 65 | 310 | ||||||||||||||

Table (6)

5.

Prepare a trail balance for Y Restaurant.

Explanation of Solution

Trial balance: Trial balance is a summary of all the ledger accounts balances presented in a tabular form with two column, debit and credit. It checks the mathematical accuracy of the ledger postings and helps preparing the final accounts.

Preparing the trial balance for Y Company:

| Y Restaurant | ||

| Trail balance | ||

| January 31, 20__ | ||

| Account name | Debit ($) | Credit($) |

| Cash | 17,317.6 | |

| Accounts receivable | 4,912.2 | |

| Merchandise inventory | 20,584 | |

| Supplies | 685.5 | |

| Prepaid insurance | 390 | |

| Equipment | 3,644 | |

| Accounts payable | 3,848.5 | |

| Employee's federal income tax payable | 795 | |

| FICA tax payable | 902.7 | |

| State unemployment tax payable | 265.5 | |

| Federal unemployment tax payable | 47.2 | |

| Mr. L capital | 39,500 | |

| Mr. L drawings | 1,000 | |

| Sales | 17,673.07 | |

| Sales returns and allowances | 47 | |

| Sales discounts | 47.16 | |

| Purchases | 6,530 | |

| Purchases returns and allowances | 87 | |

| Purchases discounts | 68.6 | |

| Freight in | 206 | |

| Salary expense | 5,900 | |

| Payroll tax expense | 764.05 | |

| Rent expense | 850 | |

| Miscellaneous expense | 310 | |

| Total | 63,187.61 | 63,187.61 |

Table (7)

6.

Prepare a schedule for accounts receivable and accounts payable.

Explanation of Solution

Schedule for the accounts receivable:

| Y Restaurant | |

| Schedule of accounts receivable | |

| January 31, 20__ | |

| Particulars | Amount($) |

| B company | 1,697.2 |

| E and C company | 1,115 |

| V company | 2,100 |

| Total accounts receivable | $4,912.2 |

Table (8)

Schedule for the accounts payable:

| Y Restaurant | |

| Schedule of accounts payable | |

| January 31, 20__ | |

| Particulars | Amount($) |

| C company | 3,755 |

| D company | 93.5 |

| Total accounts payable | $3,848.5 |

Table (9)

Want to see more full solutions like this?

Chapter 10 Solutions

College Accounting (Book Only): A Career Approach

- The following transactions were completed by Hammond Auto Supply during January, which is the first month of this fiscal year. Terms of sale are 2/10, n/30. The balances of the accounts as of January 1 have been recorded in the general ledger in your Working Papers or in CengageNow. Hammond Auto Supply does not track cash sales by customer. If you are using the form-based approach with QuickBooks or general ledger, select Cash Sales as the customer for all cash sales transactions. Required 1. Record the transactions for January using a sales journal, page 73; a purchases journal, page 56; a cash receipts journal, page 38; a cash payments journal, page 45; and a general journal, page 100. Assume the periodic inventory method is used. 2. Post daily all entries involving customer accounts to the accounts receivable ledger. 3. Post daily all entries involving creditor accounts to the accounts payable ledger. 4. Post daily those entries involving the Other Accounts columns and the general journal to the general ledger. Write the owners name in the Capital and Drawing accounts. 5. Add the columns of the special journals and prove the equality of the debit and credit totals on scratch paper. 6. Post the appropriate totals of the special journals to the general ledger. 7. Prepare a trial balance. 8. Prepare a schedule of accounts receivable and a schedule of accounts payable. Do the totals equal the balances of the related controlling accounts?arrow_forwardThe following transactions were completed by Yang Restaurant Equipment during January, the first month of this fiscal year. Terms of sale are 2/10, n/30. The balances of the accounts as of January 1 have been recorded in the general ledger in your Working Papers or in CengageNow. Yang Restaurant Equipment does not track cash sales by customer. If you are using the form-based approach with QuickBooks or general ledger, select Cash Sales as the customer for all cash sales transactions. Required 1. Record the transactions for January using a sales journal, page 91; a purchases journal, page 74; a cash receipts journal, page 56; a cash payments journal, page 63; and a general journal, page 119. Assume the periodic inventory method is used. 2. Post daily all entries involving customer accounts to the accounts receivable ledger. 3. Post daily all entries involving creditor accounts to the accounts payable ledger. 4. Post daily those entries involving the Other Accounts columns and the general journal to the general ledger. Write the owners name in the Capital and Drawing accounts. 5. Add the columns of the special journals and prove the equality of the debit and credit totals on scratch paper. 6. Post the appropriate totals of the special journals to the general ledger. 7. Prepare a trial balance. 8. Prepare a schedule of accounts receivable and a schedule of accounts payable. Do the totals equal the balances of the related controlling accounts?arrow_forwardTransactions related to purchases and cash payments completed by Wisk Away Cleaning Services Inc. during the month of May 20Y5 are as follows: Prepare a purchases journal and a cash payments journal to record these transactions. The forms of the journals are similar to those illustrated in the text. Place a check mark () in the Post. Ref. column to indicate when the accounts payable subsidiary ledger should be posted. Wisk Away Cleaning Services Inc. uses the following accounts:arrow_forward

- Happy Tails Inc. has a September 1, 20Y4, accounts payable balance of 620, which consists of 320 due Labradore Inc. and 300 due Meow Mart Inc. Transactions related to purchases and cash payments completed by Happy Tails Inc. during the month of September 20Y4 are as follows: a. Prepare a purchases journal and a cash payments journal to record these transactions. The forms of the journals are similar to those used in the text. Place a check mark () in the Post. Ref. column to indicate when the accounts payable subsidiary ledger should be posted. Happy Tails Inc. uses the following accounts: b. Prepare a listing of accounts payable creditor balances on September 30, 20Y4. Verify that the total of the accounts payable creditor balances equals the balance of the accounts payable controlling account on September 30, 20Y4. c. Why does Happy Tails Inc. use a subsidiary ledger for accounts payable?arrow_forwardTransactions related to revenue and cash receipts completed by Sycamore Inc. during the month of December 2016 are as follows: Prepare a single-column revenue journal and a cash receipts journal to record these transactions. Use the following column headings for the cash receipts journal: Fees Earned Cr., Accounts Receivable Cr., and Cash Dr. Place a check mark () in the Post. Ref. column to indicate when the accounts receivable subsidiary ledger should be posted.arrow_forwardCatherines Cookies has a beginning balance in the Accounts Payable control total account of $8,200. In the cash disbursements journal, the Accounts Payable column has total debits of $6,800 for November. The Accounts Payable credit column in the purchases journal reveals a total of $10,500 for the current month. Based on this information, what is the ending balance in the Accounts Payable account in the general ledger?arrow_forward

- The transactions completed by Revere Courier Company during December, the first month of the fiscal year, were as follows: Instructions 1. Enter the following account balances in the general ledger as of December 1: 2. Journalize the transactions for December, using the following journals similar to those illustrated in this chapter: cash receipts journal (p. 31), purchases journal (p. 37, with columns for Accounts Payable, Maintenance Supplies, Office Supplies, and Other Accounts), single-column revenue journal (p. 35), cash payments journal (p. 34), and two-column general journal (p. 1). Assume that the daily postings to the individual accounts in the accounts payable subsidiary ledger and the accounts receivable subsidiary ledger have been made. 3. Post the appropriate individual entries to the general ledger. 4. Total each of the columns of the special journals and post the appropriate totals to the general ledger; insert the account balances. 5. Prepare a trial balance.arrow_forwardMacDonald Bookshop had the following transactions that occurred during February of this year: Required 1. Journalize the transactions for February in the cash payments journal. Assume the periodic inventory method is used. 2. If you are using Working Papers, total and rule the journal. Prove the equality of the debit and credit totals.arrow_forwardDuring the month of October 20--, The Pink Petal flower shop engaged in the following transactions: Selected account balances as of October 1 were as follows: The Pink Petal also had the following subsidiary ledger balances as of October 1: REQUIRED 1. Record the transactions in a sales journal (page 7), cash receipts journal (page 10), purchases journal (page 6), cash payments journal (page 11), and general journal (page 5). Total, verify, and rule the columns where appropriate at the end of the month. 2. Post from the journals to the general ledger, accounts receivable ledger, and accounts payable ledger accounts. Use account numbers as shown in the chapter.arrow_forward

- Your company paid rent of $1,000 for the month with check number 1245. Which journal would the company use to record this? A. sales journal B. purchases journal C. cash receipts journal D. cash disbursements journal E. general journalarrow_forwardTransactions related to revenue and cash receipts completed by Albany Architects Co. during the period November 230, 2016, are as follows: Instructions 1. Insert the following balances in the general ledger as of November 1: 2. Insert the following balances in the accounts receivable subsidiary ledger as of November 1: 3. Prepare a single-column revenue journal (p. 40) and a cash receipts journal (p. 36). Use the following column headings for the cash receipts journal: Fees Earned Cr., Accounts Receivable Cr., and Cash Dr. The Fees Earned column is used to record cash fees. Insert a check mark () in the Post. Ref. column when recording cash fees. 4. Using the two special journals and the two-column general journal (p. 1), journalize the transactions for November. Post to the accounts receivable subsidiary ledger, and insert the balances at the points indicated in the narrative of transactions. Determine the balance in the customers account before recording a cash receipt. 5. Total each of the columns of the special journals, and post the individual entries and totals to the general ledger. Insert account balances after the last posting. 6. Determine that the sum of the customer balances agrees with the accounts receivable controlling account in the general ledger. 7. Why would an automated system omit postings to a controlling account as performed in step 5 for Accounts Receivable?arrow_forwardRaj Department store has one cash register. On a recent day, the cash register tape reported sales in theamount of $12,675.12. Actual cash in the register (after deducting and removing the opening change of$100) was $12,649.81, which was deposited in the firm’s account.Required:Prepare a journal entry to record these cash sales.arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub