Videos

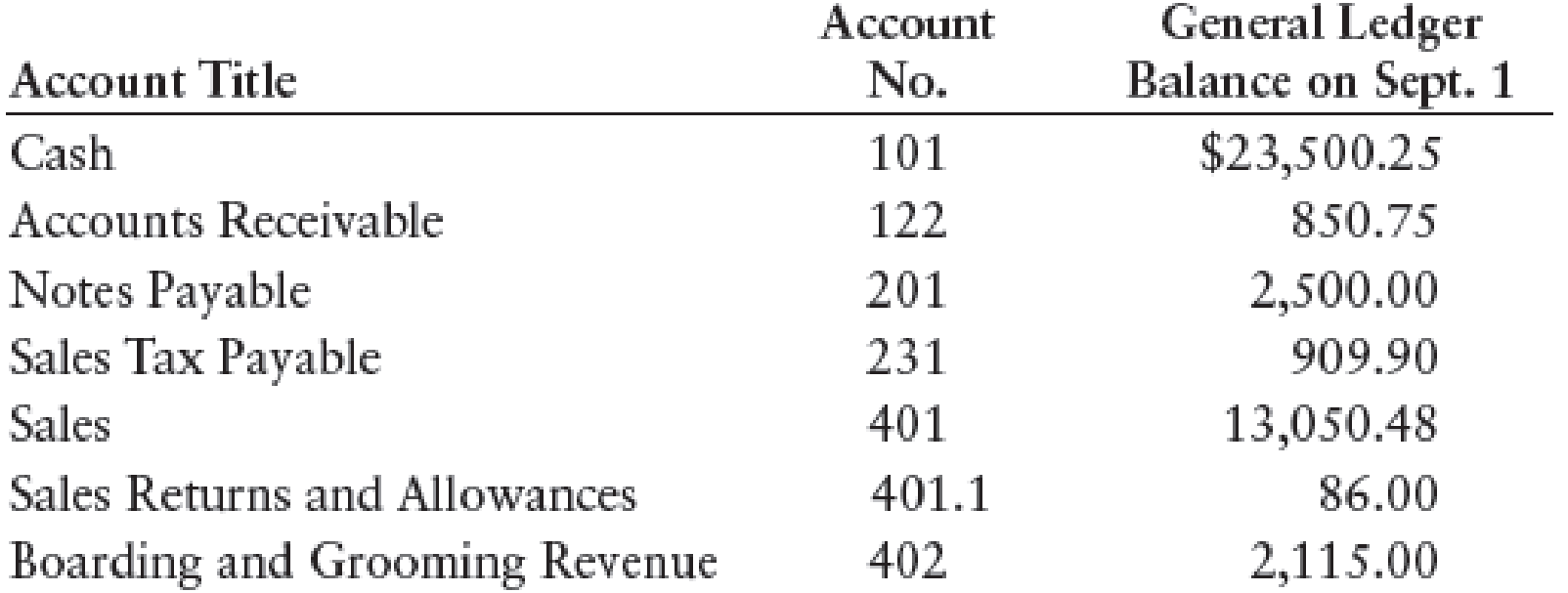

Geoff and Sandy Harland own and operate Wayward Kennel and Pet Supply. Their motto is, “If your pet is not becoming to you, he should be coming to us.” The Harlands maintain a sales tax payable account throughout the month to account for the 6% sales tax. They use a general journal, general ledger, and accounts receivable ledger. The following sales and cash collections took place during the month of September:

Sept. 2 Sold a fish aquarium on account to Ken Shank, $125 plus tax of $7.50, terms n/30. Sale No. 101.

3 Sold dog food on account to Nancy Truelove, $68.25 plus tax of $4.10, terms n/30. Sale No. 102.

5 Sold a bird cage on account to Jean Warkentin, $43.95 plus tax of $2.64, terms n/30. Sale No. 103.

8 Cash sales for the week were $2,332.45 plus tax of $139.95.

10 Received cash for boarding and grooming services, $625 plus tax of $37.50.

11 Jean Warkentin stopped by the store to point out a minor defect in the bird cage purchased in Sale No. 103. The Harlands offered a sales allowance of $10 plus tax on the price of the cage which satisfied Warkentin.

12 Sold a cockatoo on account to Tully Shaw, $1,200 plus tax of $72, terms n/30. Sale No. 104.

14 Received cash on account from Rosa Alanso, $256.

15 Rosa Alanso returned merchandise, $93.28 including tax of $5.28.

15 Cash sales for the week were $2,656.85 plus tax of $159.41.

16 Received cash on account from Nancy Truelove, $58.25.

18 Received cash for boarding and grooming services, $535 plus tax of $32.10.

19 Received cash on account from Ed Cochran, $63.25.

20 Sold pet supplies on account to Susan Hays, $83.33 plus tax of $5, terms n/30. Sale No. 105.

21 Sold three Labrador Retriever puppies to All American Day Camp, $375 plus tax of $22.50, terms n/30. Sale No. 106.

22 Cash sales for the week were $3,122.45 plus tax of $187.35.

23 Received cash for boarding and grooming services, $515 plus tax of $30.90.

25 Received cash on account from Ken Shank, $132.50.

26 Received cash on account from Nancy Truelove, $72.35.

27 Received cash on account from Joe Gloy, $273.25.

28 Borrowed cash to purchase a pet limousine, $11,000.

29 Cash sales for the week were $2,835.45 plus tax of $170.13.

30 Received cash for boarding and grooming services, $488 plus tax of $29.28.

Wayward had the following general ledger account balances as of September 1:

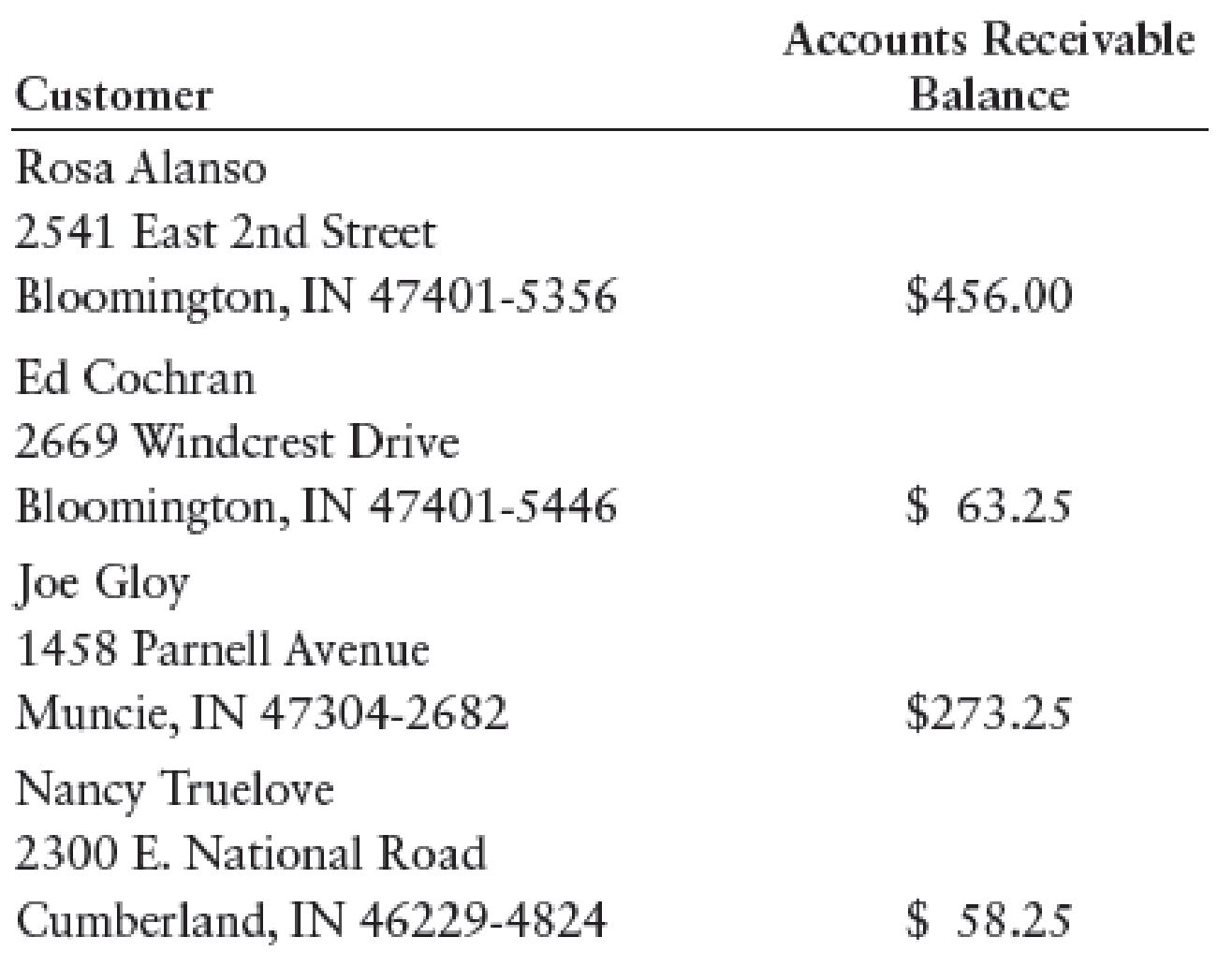

Wayward also had the following accounts receivable ledger balances as of September 1:

New customers opening accounts during September were as follows:

All American Day Camp

3025 Old Mill Run

Bloomington, IN 47408-1080

Tully Shaw

3315 Longview Avenue

Bloomington, IN 47401-7223

Susan Hays

1424 Jackson Creek Road

Nashville, IN 47448-2245

Jean Warkentin

1813 Deep Well Court

Bloomington, IN 47401-5124

Ken Shank

6422 E. Bender Road

Bloomington, IN 47401-7756

REQUIRED

- 1. Enter the transactions for the month of September in a general journal. (Begin with page 7.)

- 2. Post the entries to the general and subsidiary ledgers. Open new accounts for any customers who did not have a balance as of September 1.

- 3. Prepare a schedule of accounts receivable.

- 4. Compute the net sales for the month of September.

1.

Journalize the transactions for the month of September.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Journalize the transactions for the month of September.

Transaction on September 2:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 2 | Accounts Receivable, KS | 122/✓ | 132.50 | ||

| Sales | 401 | 125.00 | ||||

| Sales Tax Payable | 231 | 7.50 | ||||

| (Record credit sale) | ||||||

Table (1)

Description:

- Accounts Receivable, KS is an asset account. Since sales is made on account, the receivables increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 3:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 3 | Accounts Receivable, NT | 122/✓ | 72.35 | ||

| Sales | 401 | 68.25 | ||||

| Sales Tax Payable | 231 | 4.10 | ||||

| (Record credit sale) | ||||||

Table (2)

Description:

- Accounts Receivable, NT is an asset account. Since sales is made on account, the receivables increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 5:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 5 | Accounts Receivable, JW | 122/✓ | 46.59 | ||

| Sales | 401 | 43.95 | ||||

| Sales Tax Payable | 231 | 2.64 | ||||

| (Record credit sale) | ||||||

Table (3)

Description:

- Accounts Receivable, JW is an asset account. Since sales is made on account, the receivables increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 8:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 8 | Cash | 101 | 2,472.40 | ||

| Sales | 401 | 2,332.45 | ||||

| Sales Tax Payable | 231 | 139.95 | ||||

| (Record cash sales) | ||||||

Table (4)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 10:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 10 | Cash | 101 | 662.50 | ||

| Boarding and Grooming Revenue | 402 | 625.00 | ||||

| Sales Tax Payable | 231 | 37.50 | ||||

| (Record cash sales) | ||||||

Table (5)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Boarding and Grooming Revenue is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 11:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 11 | Sales Returns and Allowances | 401.1 | 10.00 | ||

| Sales Tax Payable | 231 | 0.60 | ||||

| Accounts Receivable, JW | 122/✓ | 10.60 | ||||

| (Record grant of sales allowance) | ||||||

Table (6)

Description:

- Sales Returns and Allowances is a contra-revenue account, and contra-revenue accounts decrease the equity value, and a decrease in equity is debited.

- Sales Tax Payable is a liability account. Since the payable decreased due to returns, the liability decreased, and a decrease in liability is debited.

- Accounts Receivable, JW is an asset account. Since sales allowance is granted, amount to be received has decreased, asset account is decreased, and a decrease in asset is credited.

Working Note 1:

Compute sales tax payable amount.

Working Note 2:

Compute accounts receivable amount (Refer to Working Note 1 for value of sales tax payable).

Transaction on September 12:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 12 | Accounts Receivable, TS | 122/✓ | 1,272 | ||

| Sales | 401 | 1,200 | ||||

| Sales Tax Payable | 231 | 72 | ||||

| (Record credit sale) | ||||||

Table (7)

Description:

- Accounts Receivable, TS is an asset account. Since sales is made on account, the receivables increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 14:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post. Ref. | Debit ($) | Credit ($) | ||

| September | 14 | Cash | 101 | 256 | ||

| Accounts Receivable, RA | 122/✓ | 256 | ||||

| (Record cash received for sales on account) | ||||||

Table (8)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accounts Receivable, RA is an asset account. Since amount to be received has decreased, asset account decreased, and a decrease in asset is credited.

Transaction on September 15:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 15 | Sales Returns and Allowances | 401.1 | 88.00 | ||

| Sales Tax Payable | 231 | 5.28 | ||||

| Accounts Receivable, RA | 122/✓ | 93.28 | ||||

| (Record goods returned) | ||||||

Table (9)

Description:

- Sales Returns and Allowances is a contra-revenue account, and contra-revenue accounts decrease the equity value, and a decrease in equity is debited.

- Sales Tax Payable is a liability account. Since the payable decreased due to returns, the liability decreased, and a decrease in liability is debited.

- Accounts Receivable, RA is an asset account. Since inventory is returned, amount to be received has decreased, asset account is decreased, and a decrease in asset is credited.

Transaction on September 15:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 15 | Cash | 101 | 2,816.26 | ||

| Sales | 401 | 2,656.85 | ||||

| Sales Tax Payable | 231 | 159.41 | ||||

| (Record cash sales) | ||||||

Table (10)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 16:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post. Ref. | Debit ($) | Credit ($) | ||

| September | 16 | Cash | 101 | 58.25 | ||

| Accounts Receivable, NT | 122/✓ | 58.25 | ||||

| (Record cash received for sales on account) | ||||||

Table (11)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accounts Receivable, NT is an asset account. Since amount to be received has decreased, asset account decreased, and a decrease in asset is credited.

Transaction on September 18:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 18 | Cash | 101 | 567.10 | ||

| Boarding and Grooming Revenue | 402 | 535.00 | ||||

| Sales Tax Payable | 231 | 32.10 | ||||

| (Record cash sales) | ||||||

Table (12)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Boarding and Grooming Revenue is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 19:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post. Ref. | Debit ($) | Credit ($) | ||

| September | 19 | Cash | 101 | 63.25 | ||

| Accounts Receivable, EC | 122/✓ | 63.25 | ||||

| (Record cash received for sales on account) | ||||||

Table (13)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accounts Receivable, EC is an asset account. Since amount to be received has decreased, asset account decreased, and a decrease in asset is credited.

Transaction on September 20:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 20 | Accounts Receivable, SH | 122/✓ | 88.33 | ||

| Sales | 401 | 83.33 | ||||

| Sales Tax Payable | 231 | 5.00 | ||||

| (Record credit sale) | ||||||

Table (14)

Description:

- Accounts Receivable, SH is an asset account. Since sales is made on account, the receivables increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 21:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 21 | Accounts Receivable, AD Camp | 122/✓ | 397.50 | ||

| Sales | 401 | 375.00 | ||||

| Sales Tax Payable | 231 | 22.50 | ||||

| (Record credit sale) | ||||||

Table (15)

Description:

- Accounts Receivable, AD Camp is an asset account. Since sales is made on account, the receivables increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 22:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 22 | Cash | 101 | 3,309.80 | ||

| Sales | 401 | 3,122.45 | ||||

| Sales Tax Payable | 231 | 187.35 | ||||

| (Record cash sales) | ||||||

Table (16)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 23:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 23 | Cash | 101 | 545.90 | ||

| Boarding and Grooming Revenue | 402 | 515.00 | ||||

| Sales Tax Payable | 231 | 30.90 | ||||

| (Record cash sales) | ||||||

Table (17)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Boarding and Grooming Revenue is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 25:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post. Ref. | Debit ($) | Credit ($) | ||

| September | 25 | Cash | 101 | 132.50 | ||

| Accounts Receivable, KS | 122/✓ | 132.50 | ||||

| (Record cash received for sales on account) | ||||||

Table (18)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accounts Receivable, KS is an asset account. Since amount to be received has decreased, asset account decreased, and a decrease in asset is credited.

Transaction on September 26:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post. Ref. | Debit ($) | Credit ($) | ||

| September | 26 | Cash | 101 | 72.35 | ||

| Accounts Receivable, NT | 122/✓ | 72.35 | ||||

| (Record cash received for sales on account) | ||||||

Table (19)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accounts Receivable, NT is an asset account. Since amount to be received has decreased, asset account decreased, and a decrease in asset is credited.

Transaction on September 27:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post. Ref. | Debit ($) | Credit ($) | ||

| September | 27 | Cash | 101 | 273.25 | ||

| Accounts Receivable, JG | 122/✓ | 273.25 | ||||

| (Record cash received for sales on account) | ||||||

Table (20)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accounts Receivable, JG is an asset account. Since amount to be received has decreased, asset account decreased, and a decrease in asset is credited.

Transaction on September 28:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post. Ref. | Debit ($) | Credit ($) | ||

| September | 28 | Cash | 101 | 11,000 | ||

| Notes Payable | 201 | 11,000 | ||||

| (Record cash borrowed) | ||||||

Table (21)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Notes Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 29:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 29 | Cash | 101 | 3,005.58 | ||

| Sales | 401 | 2,835.45 | ||||

| Sales Tax Payable | 231 | 170.13 | ||||

| (Record cash sales) | ||||||

Table (22)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Sales is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on September 30:

| Page: 7 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| September | 30 | Cash | 101 | 517.28 | ||

| Boarding and Grooming Revenue | 402 | 488.00 | ||||

| Sales Tax Payable | 231 | 29.28 | ||||

| (Record cash sales) | ||||||

Table (23)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Boarding and Grooming Revenue is a revenue account. Since revenues and gains increase equity, equity value is increased, and an increase in equity is credited.

- Sales Tax Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

2.

Post the journalized entries into the accounts of the general ledger, and the customer accounts in accounts receivable ledger.

Explanation of Solution

Posting transactions: The process of transferring the journalized transactions into the accounts of the ledger is known as posting the transactions.

Post the journalized entries into the accounts of the general ledger.

| ACCOUNT Cash ACCOUNT NO. 101 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| September | 1 | Balance | ✓ | 23,500.25 | |||

| 8 | J7 | 2,472.40 | 25,972.65 | ||||

| 10 | J7 | 662.50 | 26,635.15 | ||||

| 14 | J7 | 256.00 | 26,891.15 | ||||

| 15 | J7 | 2,816.26 | 29,707.41 | ||||

| 16 | J7 | 58.25 | 29,765.66 | ||||

| 18 | J7 | 567.10 | 30,332.76 | ||||

| 19 | J7 | 63.25 | 30,396.01 | ||||

| 22 | J7 | 3,309.80 | 33,705.81 | ||||

| 23 | J7 | 545.90 | 34,251.71 | ||||

| 25 | J7 | 132.50 | 34,384.21 | ||||

| 26 | J7 | 72.35 | 34,456.56 | ||||

| 27 | J7 | 273.25 | 34,729.81 | ||||

| 28 | J7 | 11,000.00 | 45,729.81 | ||||

| 29 | J7 | 3,005.58 | 48,735.39 | ||||

| 30 | J7 | 517.28 | 49,252.67 | ||||

Table (24)

| ACCOUNT Accounts Receivable ACCOUNT NO. 122 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| September | 1 | Balance | ✓ | 850.75 | |||

| 2 | J7 | 132.50 | 983.25 | ||||

| 3 | J7 | 72.35 | 1,055.60 | ||||

| 5 | J7 | 46.59 | 1,102.19 | ||||

| 11 | J7 | 10.60 | 1,091.59 | ||||

| 12 | J7 | 1,272.00 | 2,363.59 | ||||

| 14 | J7 | 256.00 | 2,107.59 | ||||

| 15 | J7 | 93.28 | 2,014.31 | ||||

| 16 | J7 | 58.25 | 1,956.06 | ||||

| 19 | J7 | 63.25 | 1,892.81 | ||||

| 20 | J7 | 88.33 | 1,981.14 | ||||

| 21 | J7 | 397.50 | 2,378.64 | ||||

| 25 | J7 | 132.50 | 2,246.14 | ||||

| 26 | J7 | 72.35 | 2,173.79 | ||||

| 27 | J7 | 273.25 | 1,900.54 | ||||

Table (25)

| ACCOUNT Notes Payable ACCOUNT NO. 201 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| September | 1 | Balance | ✓ | 2,500 | |||

| 28 | J7 | 11,000 | 13,500 | ||||

Table (26)

| ACCOUNT Sales Tax Payable ACCOUNT NO. 231 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| September | 1 | Balance | ✓ | 909.90 | |||

| 2 | J7 | 7.50 | 917.40 | ||||

| 3 | J7 | 4.10 | 921.50 | ||||

| 5 | J7 | 2.64 | 924.14 | ||||

| 8 | J7 | 139.95 | 1,064.09 | ||||

| 10 | J7 | 37.50 | 1,101.59 | ||||

| 11 | J7 | 0.60 | 1,100.99 | ||||

| 12 | J7 | 72.00 | 1,172.99 | ||||

| 15 | J7 | 5.28 | 1,167.71 | ||||

| 15 | J7 | 159.41 | 1,327.12 | ||||

| 18 | J7 | 32.10 | 1,359.22 | ||||

| 20 | J7 | 5.00 | 1,364.22 | ||||

| 21 | J7 | 22.50 | 1,386.72 | ||||

| 22 | J7 | 187.35 | 1,574.07 | ||||

| 23 | J7 | 30.90 | 1,604.97 | ||||

| 29 | J7 | 170.13 | 1,775.10 | ||||

| 30 | J7 | 29.28 | 1,804.38 | ||||

Table (27)

| ACCOUNT Sales ACCOUNT NO. 401 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| September | 1 | Balance | ✓ | 13,050.48 | |||

| 2 | J7 | 125.00 | 13,050.48 | ||||

| 3 | J7 | 68.25 | 13,243.73 | ||||

| 5 | J7 | 43.95 | 13,287.68 | ||||

| 8 | J7 | 2,332.45 | 15,620.13 | ||||

| 12 | J7 | 1,200.00 | 16,820.13 | ||||

| 15 | J7 | 2,656.85 | 19,476.98 | ||||

| 20 | J7 | 83.33 | 19,560.31 | ||||

| 21 | J7 | 375.00 | 19,935.31 | ||||

| 22 | J7 | 3,122.45 | 23,057.76 | ||||

| 29 | J7 | 2,835.45 | 25,893.21 | ||||

Table (28)

| ACCOUNT Sales Returns and Allowances ACCOUNT NO. 401.1 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| September | 1 | Balance | ✓ | 86.00 | |||

| 11 | J7 | 10.00 | 96.00 | ||||

| 15 | J7 | 88.00 | 184.00 | ||||

Table (29)

| ACCOUNT Boarding and Grooming Revenue ACCOUNT NO. 402 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| September | 1 | Balance | ✓ | 2,115.00 | |||

| 10 | J7 | 625.00 | 2,740.00 | ||||

| 18 | J7 | 535.00 | 3,275.00 | ||||

| 23 | J7 | 515.00 | 3,790.00 | ||||

| 30 | J7 | 488.00 | 4,278.00 | ||||

Table (30)

Post the journalized entries into the customer accounts in accounts receivable ledger.

| NAME AD Camp | ||||||

| ADDRESS 3025, OM Run, City B, State IN 47408-1080 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| September | 21 | J7 | 397.50 | 397.50 | ||

Table (31)

| NAME RA | ||||||

| ADDRESS 2541, E Street, City B, State IN 47401-5356 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| September | 1 | Balance | ✓ | 456.00 | ||

| 14 | J7 | 256.00 | 200.00 | |||

| 15 | J7 | 93.28 | 106.72 | |||

Table (32)

| NAME EC | ||||||

| ADDRESS 2669, W Drive, City B, State IN 47401-5446 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| September | 1 | Balance | ✓ | 63.25 | ||

| 19 | J7 | 63.25 | 0 | |||

Table (33)

| NAME JG | ||||||

| ADDRESS 1458, P Avenue, City B, State IN 47304-2682 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| September | 1 | Balance | ✓ | 273.25 | ||

| 27 | J7 | 273.25 | 0 | |||

Table (34)

| NAME SH | ||||||

| ADDRESS 1424, JC Road, City N, State IN 47448-2245 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| September | 20 | J7 | 88.33 | 88.33 | ||

Table (35)

| NAME KS | ||||||

| ADDRESS 6422, EB Road, City B, State IN 47401-7756 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| September | 2 | Balance | J7 | 132.50 | 132.50 | |

| 19 | J7 | 132.50 | 0 | |||

Table (36)

| NAME TS | ||||||

| ADDRESS 3315, L Avenue, City N, State IN 47401-7223 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| September | 12 | J7 | 1,272.00 | 1,272.00 | ||

Table (37)

| NAME NT | ||||||

| ADDRESS 2300, EN Road, City C, State IN 46229-4824 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| September | 1 | Balance | ✓ | 58.25 | ||

| 3 | J7 | 72.35 | 130.60 | |||

| 16 | J7 | 58.25 | 72.35 | |||

| 26 | J7 | 72.35 | 0 | |||

Table (38)

| NAME JW | ||||||

| ADDRESS 1813, DP Court, City B, State IN 47401-5124 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| September | 5 | J7 | 46.59 | 46.59 | ||

| 3 | J7 | 10.60 | 35.99 | |||

Table (39)

3.

Prepare the schedule of accounts receivable for W Kennel and P Supply as at September 30, 20--.

Explanation of Solution

Accounts receivable schedule: This is the schedule which is prepared to verify that the total balances of all the customers in the accounts receivable ledger, equals the balance of Accounts Receivable in the general ledger.

Prepare the schedule of accounts receivable for W Kennel and P Supply as at September 30, 20--.

| W Kennel and P Supply | |

| Schedule of Accounts Receivable | |

| September 30, 20-- | |

| AD Camp | $397.50 |

| RA | 106.72 |

| SH | 88.33 |

| TS | 1,272.00 |

| JW | 35.99 |

| Total | $1,900.54 |

Table (40)

Note: Refer to Requirement 2 for the value and computation of customer balances.

Thus, the schedule of accounts receivable of W Kennel and P Supply shows a balance of $1,900.54, as of September 30, 20--.

4.

Ascertain the net sales for W Kennel and P Supply for the month of September.

Explanation of Solution

Net sales: The amount of price of merchandise sold during a certain period is referred to as sales revenue. Net sales is the gross sales, minus sales returns and allowances, and sales discounts.

Formula to compute net sales:

Ascertain the net sales for W Kennel and P Supply for the month of September.

Note: Refer to Requirement 2 for the value and computation of the balances.

Thus, net sales for W Kennel and P Supply for the month of September is $12,744.73.

Want to see more full solutions like this?

Chapter 10 Solutions

College Accounting, Chapters 1-27

- Bell Florists sells flowers on a retail basis. Most of the sales are for cash; however, a few steady customers have credit accounts. Bells sales staff fills out a sales slip for each sale. There is a state retail sales tax of 5 percent, which is collected by the retailer and submitted to the state. The balances of the accounts as of March 1 have been recorded in the general ledger in your Working Papers or in CengageNow. The following represent Bell Florists charge sales for March: Mar. 4Sold potted plant on account to C. Morales, sales slip no. 242, 27, plus sales tax of 1.35, total 28.35. 6Sold floral arrangement on account to R. Dixon, sales slip no. 267, 54, plus sales tax of 2.70, total 56.70. 12Sold corsage on account to B. Cox, sales slip no. 279, 16, plus sales tax of 0.80, total 16.80. 16Sold wreath on account to All-Star Legion, sales slip no. 296, 104, plus sales tax of 5.20, total 109.20. 18Sold floral arrangements on account to Tucker Funeral Home, sales slip no. 314, 260, plus sales tax of 13, total 273. 21Tucker Funeral Home complained about a wrinkled ribbon on the floral arrangement. Bell Florists allowed a 30 credit plus sales tax of 1.50, credit memo no. 27. 23Sold flower arrangements on account to Price Savings and Loan Association for its fifth anniversary, sales slip no. 337, 180, plus sales tax of 9, total 189. 24Allowed Price Savings and Loan Association credit, 25, plus sales tax of 1.25, because of a few withered blossoms in floral arrangements, credit memo no. 28. Required 1. Record these transactions in the general journal. 2. Post the amounts from the general journal to the general ledger and accounts receivable ledger: Accounts Receivable 113, Sales Tax Payable 214, Sales 411, Sales Returns and Allowances 412. 3. Prepare a schedule of accounts receivable and compare its total with the balance of the Accounts Receivable controlling account.arrow_forwardGeorgie is unable to get to her bank to withdrawal cash. Last month she withdrew cash 5 times at an ATM at a gas station, each transaction cost her $4.25. She then I cost of $1.25 per went to the bank closest to work and withdrew cash 6 times at transaction. How much did Georgie spend last month on service fees?arrow_forwardSamantha and Samuel both have student credit cards issued by VISA. Their credit card statements show they are at their credit card limit of $500 this month. Samantha manages her credit well and ensures that her credit card balance is paid off in full each month before the payment deadline while Samuel cannot manage to pay off the minimum amount required each month. Complete the sentence: For Financial Statement reporting purposes, __________________________________________. a) It does not matter where Samantha or Samuel report the$500 as long as it is shown on one of their Financial Statements. b) Both Samantha and Samuel would report their $500 on their Balance Sheet as a current liability. c) Both Samantha and Samuel would report their $500 on their Cash Flow statement as an expense. d) Samantha would report her $500 on her Cash Flow statement as an expense while Samuel would report his credit card debt of $500 on his Balance Sheet as a current liability. e) Samantha would report her…arrow_forward

- Jack owns a shop that sells furniture. He placed an advertisement in the Friday’s edition of the local paper stating: “Sale on all furniture 25% discount. Offer valid for one day only – tomorrow Saturday- Cash Only”. Nick saw previously a dining table with 6 chairs when he visited the shop during the week. However, he could not purchase it at that time because the prices was quite steep. He has in his possession the ID number and details of the dining table. When he saw the advertisement on Local paper, he immediately posted a letter of acceptance, since a 25% discount is a bargain for him. On the Saturday of the sale, Diana saw a wooden stool and made an offer to Jack. Diana then asked Jack if he would take a cheque for her purchase, Jack advised her that he cannot accept any cheque – Cash only. On the following Monday morning, Nick’s letter arrived. In the context of the rules governing the creation of contracts: (a) Describe the precise legal nature of Jack’s advertisement;…arrow_forwardIn early December Alice and Bob decided to open Sample Cafe with $14,000 of their own money and $19,000 borrowed from a friend. They have spent $11,000 on equipment and furniture, and they have purchased $2,800 worth of cups for cash which they expect will be used over the next three months. Having put down a $2,400 deposit for a location on Main St., they will pay the first month’s rent when they open their doors on January 1. In the balance sheet template below, fill in the appropriate values as of December 31.arrow_forwardA sales representative lives in Bloomington and must be in Indianapolis next Thursday. On each of the days Monday, Tuesday, and Wednesday, he can sell his wares in Indianapolis, Bloomington, or Chicago. From past experience, he believes that he can earn $12 from spending a day in Indianapolis, $16 from spending a day in Bloomington, and $17 from spending a day in Chicago. Where should he spend the first three days and nights of the week to maximize his sales income less travel costs? Travel costs are shown in Table 2. TABLE 2 From To Indianapolis Bloomington Chicago Indianapolis 5 2 | Bloomington 5 7 Chicago 7 -arrow_forward

- June Xu is a registered nurse who earns $3,250 per month after taxes. She has been reviewing her savings strategies and current banking arrangements to determine if she should make any changes. June has a regular checking account that charges her a flat fee per month, writes an average of 18 checks a month, and carries an average balance of $795 (although it has fallen below $750 during 3 months of the past year). Her only other account is a money market deposit account with a balance of $4,250. She tries to make regular monthly deposits of $50–$100 into her money market account but has done so only about every other month. Of the many checking accounts June’s bank offers, here are the three that best suit her needs.• Regular checking, per-item plan: Service charge of $3 per month plus 35 cents per check.• Regular checking, flat-fee plan (the one June currently has): Monthly fee of $7 regardless of how many checks written. With either of these regular checking accounts, she can avoid…arrow_forwardOn December 1, 2019, AwakcAllNight Inc. sells 5,000 super caffeinated candy bars to Campus Grocers. The candy bars sell for 3 per bar. In addition, AwakcAllNight pays Campus Grocers a 900placement fee to ensure that its candy bars are always stocked prominently by the cash register. The 900 is paid at the end of each month based on the results of random inspections of Campus Grocers by AwakcAllNight to ensure that the terms of the contract are being followed. Required: 1. Determine the transaction price for Awake AllNights revenue contract. 2. Prepare AwakeAllNights journal entries to recognize sales revenue and pay Campus Grocers the placement fee.arrow_forwardErnie Bilko has a business idea. He wants to rent an abandoned gas station for just the months of November and December. He will convert the gas station into a drive-through Christmas wrapping station. Customers will drive in, drop off their gifts, return the next day, and pick up their wrapped gifts. He needs $338,500 to rent the gas station, purchase wrapping paper, hire workers, and advertise. If he borrows this amount at 6 and 1/2% interest for those two months, what size lump sum payment will he have to make to pay off the loan? (Round your answer to the nearest cent.)arrow_forward

- ) Samantha and Samuel both have student credit cards issued by VISA. Their credit card statements show they are at their credit card limit of $500 this month. Samantha manages her credit well and ensures that her credit card balance is paid off in full each month before the payment deadline while Samuel cannot manage to pay off the minimum amount required each month. Complete the senterice: For Financial Statement reporting purposes, a) It does not matter where Samantha or Samuel report the $500 as long as it is shown on one of their Financial Statements. b) Both Samantha and Samuel would report their $500 on their Balance Sheet as a current liability. c) Both Samantha and Samuel would report their $500 on their Cash Flow statement as an expense. d) Samantha would report her $500 on her Cash Flow statement as an expense while Samuel would report his credit card debt of 5500 on his Balance Sheet as a current liability. e) Samantha would report her $500 on her Balance Sheet as a…arrow_forwardWhile she was travelling, Kadijah took advantage of the convenience of cash withdrawals on her credit card since her Canadian debit card wasn't accepted in the country she was in. According to her travel budget she withdrew $150 every day for food, activities and shopping for 21 days. When she got home, on the 21st day, she checked her credit card bill on-line and it showed that she had been charged interest already even though her payment wasn't past due. It turns out that interest is compounded daily on cash withdrawals, from the day the cash is withdrawn. If the interest rate on cash withdrawals is 28%, what was her total bill when she got home? What would be the total interest paid?arrow_forwardSue is a small business owner who often gives gifts to clients. She gives a $40 gift to her client, Mr. Smith, and his wife. Sue spent $6 to wrap the gift. She also gave out 400 calendars with her company name on them. Each calendar cost $1. Sue also gave her secretary a $370 watch for his 10 years of service. How much of the above expenses may she duduct?arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning