Videos

(a)

Balance Sheet

This is a financial statement that shows the assets owned, and the liabilities owed to the creditors and the owners (

To Prepare: The

(a)

Explanation of Solution

Figure (1)

Description:

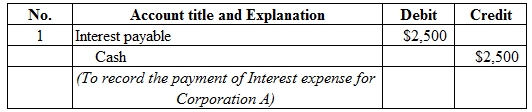

- Interest payable is a current liability, and decreased. Therefore, debit interest payable account for $2,500.

- Cash is a current asset, and decreased. Therefore, credit cash account for $2,500.

Figure (2)

Description:

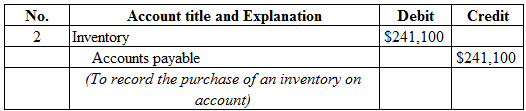

- Inventory is a current asset, and increased. Therefore, debit inventory account for $241,100.

- Accounts payable is a current liability, and increased. Therefore, credit accounts payable account for $241,100.

Figure (3)

Description:

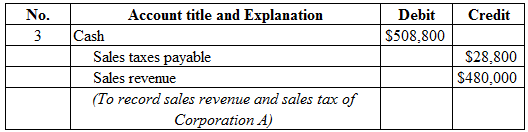

- Cash is a current asset, and increased. Therefore, debit cash is a current asset account for $508,800.

- Sales taxes payable is a current liability, and increased. Therefore, credit sales taxes payable account for $28,800.

- Sales revenue is a component of stockholders’ equity, and increased it. Therefore, credit sales revenue account for $480,000.

Figure (4)

Description:

- Cost of goods sold is a component of stockholders’ equity, and decreased it. Therefore, debit cost of goods sold account for $265,000.

- Inventory is a current asset, and decreased. Therefore, credit inventory account for $265,000.

Figure (5)

Description:

- Accounts payable is a current liability, and decreased. Therefore, debit accounts payable account for $230,000.

- Cash is a current asset, and decreased. Therefore, credit cash account for $230,000.

Figure (6)

Description:

- Interest expense is a component of stockholders’ equity, and decreased it. Therefore, debit interest expense account for $2,500.

- Cash is a current asset, and decreased. Therefore, credit cash account for $2,500.

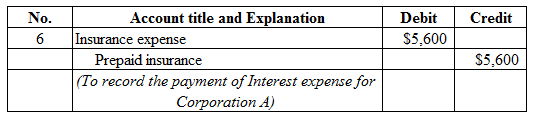

Figure (7)

Description:

- Insurance expense is a component of stockholders’ equity, and decreased it. Therefore, debit insurance expense account for $5,600.

- Cash is a current asset, and decreased. Therefore, credit cash account for $5,600.

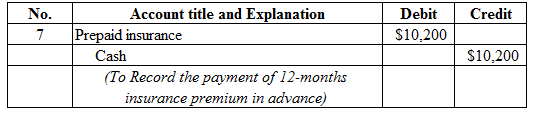

Figure (8)

Description:

- Prepaid insurance is a current asset, and increased. Therefore, debit prepaid insurance account for $10,200.

- Cash is a current asset, and decreased. Therefore, credit cash account for $10,200.

Figure (9)

Description:

- Sales taxes payable is a current liability, and decreased. Therefore, debit sales taxes payable account for $17,000.

- Cash is a current asset, and decreased. Therefore, credit cash account for $17,000.

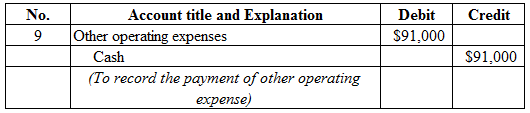

Figure (10)

Description:

- Other operating expenses are a component of stockholders’ equity, and decreased it. Therefore, debit other operating expenses account for $91,000.

- Cash is a current asset, and decreased. Therefore, credit cash account for $91,000.

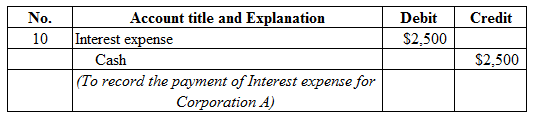

Figure (11)

Description:

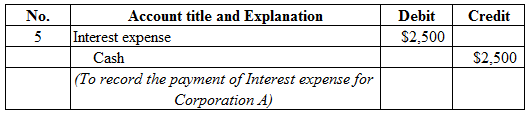

- Interest expense is a component of stockholders’ equity, and decreased it. Therefore, debit interest expense account for $2,500.

- Cash is a current asset, and decreased. Therefore, credit cash account for $2,500.

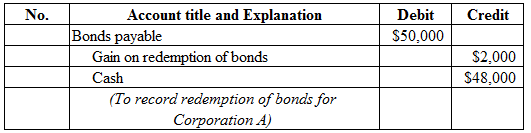

Figure (12)

Description:

- Bonds payable is a liability, and decreased. Therefore, debit bonds payable account for $50,000.

- Gain on redemption of bonds is a component of stockholders’ equity, and increased it. Therefore, credit gain on redemption of bonds account for $2,000.

- Cash is a current asset, and decreased. Therefore, credit cash account for $48,000.

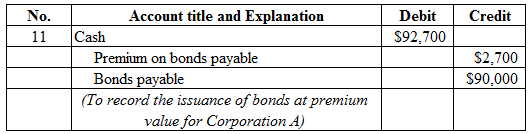

Figure (13)

Description:

- Cash is a current asset, and increased. Therefore, debit cash account for $92,700.

- Premium on bonds payable is a contra liability, and increased. Therefore, credit premium on bonds payable for $2,700.

- Bonds payable is a long-term liability, and increased. Therefore, credit bonds payable account for $90,000.

To Prepare: The

Explanation of Solution

Prepare the adjustment entries of Corporation as shown below:

Figure (14)

Working note:

Calculate interest expense as shown below:

Description:

Insurance expense is a component of stockholders’ equity, and decreased it. Therefore, debit insurance expense account for $4,250.

Prepaid insurance is a current asset, and decreased. Therefore, credit cash account for $4,250.

Figure (15)

Description:

Depreciation expense is a component of stockholders’ equity, and decreased it. Therefore, debit depreciation expense account for $7,000.Accumulated depreciation – equipment is a contra asset, and increased. Therefore, credit accumulated depreciation - equipment account for $7,000.

Figure (16)

Working note:

Calculate income tax expense as shown below:

Description:

- Income tax expense is a component of stockholders’ equity, and decreased it. Therefore, debit income tax expense account for $31,245.

- Income taxes payable is a current liability, and increased. Therefore, credit income taxes payable account for $31,245.

To Prepare: The T-Accounts of Corporation A.

Answer to Problem 10.1CACR

| Cash | |||

| Bal. | $30,000 | $2,500 | |

| $508,800 | $230,000 | ||

| $92,700 | $2,500 | ||

| $10,200 | |||

| $17,000 | |||

| $91,000 | |||

| $2,500 | |||

| $48,000 | |||

| Bal. | $227,800 | ||

Table (1)

| Inventory | |||

| Bal. | $30,750 | $265,000 | |

| $241,100 | |||

| Bal. | $6,850 | ||

Table (2)

| Prepaid Insurance | |||

| Bal. | $5,600 | $5,600 | |

| $10,200 | $4,250 | ||

| Bal. | $5,950 | ||

Table (3)

| Equipment | |||

| Bal. | $38,000 | ||

Table (4)

| Accumulated Depreciation - Equipment | |||

| $7,000 | |||

Table (5)

| Accounts Payable | |||

| $230,000 | Bal. | $13,750 | |

| $241,100 | |||

| Bal. | $24,850 | ||

Table (6)

| Other Operating Expenses | |||

| $91,000 | |||

Table (7)

| Interest Expense | |||

| $2,500 | |||

| $2,500 | |||

| Bal. | $5,000 | ||

Table (8)

| Income Tax Expense | |||

| $31,245 | |||

Table (9)

| Interest Payable | |||

| $2,500 | Bal. | $2,500 | |

| Bal. | $0 | ||

Table (10)

| Sales Taxes Payable | |||

| $17,000 | $28,800 | ||

| Bal. | $11,800 | ||

Table (11)

| Income Taxes Payable | |||

| $31,245 | |||

Table (12)

| Bonds Payable | |||

| $50,000 | Bal. | $50,000 | |

| $90,000 | |||

| Bal. | $90,000 | ||

Table (13)

| Premium on Bonds Payable | |||

| $2,700 | |||

Table (14)

| Common Stock | |||

| Bal. | $25,000 | ||

Table (15)

| Retained Earnings | |||

| Bal. | $13,100 | ||

Table (16)

| Sales Revenue | |||

| $480,000 | |||

Table (17)

| Cost of Goods sold | |||

| $265,000 | |||

Table (18)

| Depreciation Expense | |||

| $7,000 | |||

Table (19)

| Insurance Expense | |||

| $5,600 | |||

| $4,250 | |||

| Bal. | $9,850 | ||

Table (20)

| Gain on Redemption of Bonds | |||

| Bal. | $2,000 | ||

Table (21)

Explanation of Solution

Normal balance of assets account, expenses, losses account is debit balance. Hence, a debit increases these accounts and credit decreases these accounts.

Normal balance of liabilities account, capital account, revenue account and gains is credit balance. Hence, a debit decreases these accounts and credit increases these accounts.

(b)

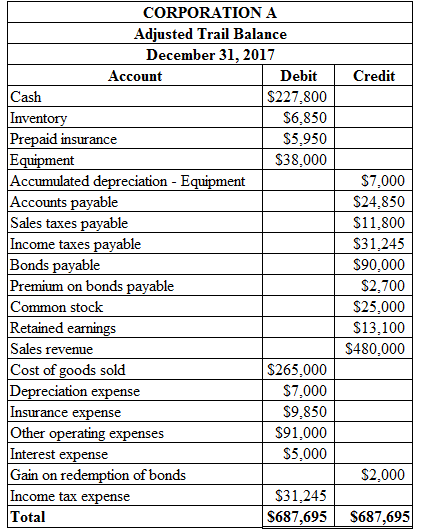

To Prepare: The adjusted trail balance of Corporation A on December 31, 2017.

(b)

Explanation of Solution

Prepare the adjusted trail balance of Corporation A on December 31, 2017 as shown below:

Figure (17)

(c)

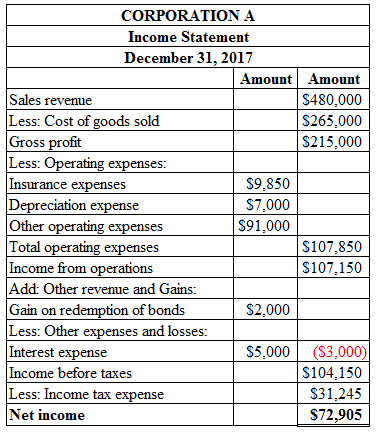

To Prepare: The income statement of Corporation A on December 31, 2017.

(c)

Answer to Problem 10.1CACR

Prepare the income statement of Corporation A on December 31, 2017 as shown below:

Figure (18)

Explanation of Solution

Gross profit is calculated by deducting cost of goods sold from sales revenue. Total operating expenses are calculated by adding insurance expense, depreciation expense, and other operating expenses. Income from operations is calculated by deducting total operating expenses from gross profit. Income before taxes is calculated by deducting interest expenses and adding gain on redemption of bonds from income from operations. Income tax expense is calculated by multiplying income from operations with tax rate. Net income is calculated by deducting income tax expense from income before taxes.

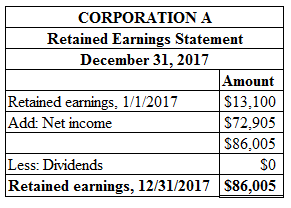

To Prepare: The retained earnings statement of Corporation A on December 31, 2017.

Answer to Problem 10.1CACR

Prepare retained earnings statement of Corporation A on December 31, 2017 as shown below:

Figure (19)

Explanation of Solution

Ending retained earnings is calculated by adding opening retained earnings and net income and then deducting the dividends. Therefore, ending retained earnings is $86,005.

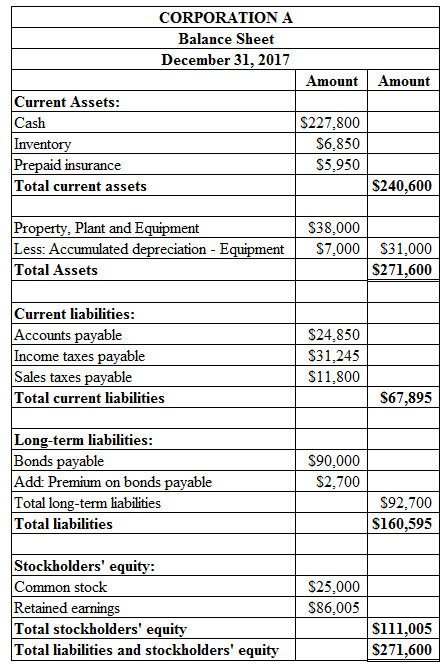

To Prepare: The classified balance sheet statement of Corporation A on December 31, 2017.

Explanation of Solution

Prepare classified balance sheet statement of Corporation A on December 31, 2017 as shown below:

Figure (20)

Want to see more full solutions like this?

Chapter 10 Solutions

Financial Accounting: Tools for Business Decision Making, 8th Edition

- Limited Review of the Akins Income Statement shows 100,000 of Net Sales for the Year 2017 and Net Income of 12,000. The terms for Sales and Purchases are 2/10, n/30. Partial Comparative Balance Sheets for the Akins Corporation appear below: (In Thousands) (In Thousands) 2017 2016 $ 3,000 $15,000 5,000 Cash Marketable Securities 9,000 Accounts Receivable 25,000 15,000 23,000 17,000 Inventory Equipment (At Book Value) 60,000 55,000 Land 20,000 15,000 Patents 50.000 50,000 Total Assets $190,000 $172,000 Current Liabilities 10,000 30,000 Long Term Liabilities Total Liabilities 70.000 100,000 75,000 85,000 a) Compute the current ratio for 2017 b) Compute the accounts receivable turnover ratio for 2017 c) Compute the average days uncollected for 2017 and provide observation.arrow_forwardTyrell Co. entered into the following transactions involving short-term liabilities in 2016 and 2017. 2016 Apr. 20 Purchased $40,250 of merchandise on credit from Locust, terms n/30. Tyrell uses the perpetual inventory system. May 19 Replaced the April 20 account payable to Locust with a 90-day, $35,000 note bearing 10% annual interest along with paying $5,250 in cash. July 8 Borrowed $80,000 cash from NBR Bank by signing a 120-day, 9% interest-bearing note with a face value of $80,000. ___?___ Paid the amount due on the note to Locust at the maturity date. ___?___ Paid the amount due on the note to NBR Bank at the maturity date. Nov. 28 Borrowed $42,000 cash from Fargo Bank by signing a 60-day, 8% interest-bearing note with a face value of $42,000. Dec. 31 Recorded an adjusting entry for accrued interest on the note to Fargo Bank. 2017 __?__ Paid the amount due on the note to Fargo Bank at the maturity date. 3. Determine the…arrow_forwardTyrell Co. entered into the following transactions involving short-term liabilities in 2016 and 2017. 2016 Apr. 20 Purchased $40,250 of merchandise on credit from Locust, terms n/30. Tyrell uses the perpetual inventory system. May 19 Replaced the April 20 account payable to Locust with a 90-day, $35,000 note bearing 10% annual interest along with paying $5,250 in cash. July 8 Borrowed $80,000 cash from NBR Bank by signing a 120-day, 9% interest-bearing note with a face value of $80,000. ___?___ Paid the amount due on the note to Locust at the maturity date. ___?___ Paid the amount due on the note to NBR Bank at the maturity date. Nov. 28 Borrowed $42,000 cash from Fargo Bank by signing a 60-day, 8% interest-bearing note with a face value of $42,000. Dec. 31 Recorded an adjusting entry for accrued interest on the note to Fargo Bank. 2017 __?__ Paid the amount due on the note to Fargo Bank at the maturity date. 5.1 Prepare…arrow_forward

- Use the following information to prepare a classified balance sheet for Alpha Co. at the end of 2016. $26,500 Accounts receivable Accounts payable 12,200 Cash 20,500 Common stock 30,000 Land 10,000 Long-term notes payable 17,500 26,300 Merchandise inventory Retained earnings 23,600arrow_forwardTyrell Co. entered into the following transactions involving short-term liabilities in 2014 and 2015. 2014 Apr. 20 Purchased $36,500 of merchandise on credit from Locust, terms are 1/10, n/30. Tyrell uses the perpetual inventory system. May 19 Replaced the April 20 account payable to Locust with a 90-day, $35,000 note bearing 8% annual interest along with paying $1,500 in cash. July 8 Borrowed $51,000 cash from National Bank by signing a 120-day, 12% interest-bearing note with a face value of $51,000. __?__ Paid the amount due on the note to Locust at the maturity date. __?__ Paid the amount due on the note to National Bank at the maturity date. Nov. 28 Borrowed $27,000 cash from Fargo Bank by signing a 60-day, 6% interest-bearing note with a face value of $27,000. Dec. 31 Recorded an adjusting entry for accrued interest on the note to Fargo Bank. 2015 __?__ Paid the amount due on the note to Fargo Bank at the maturity…arrow_forwardTyrell Co. entered into the following transactions involving short-term liabilities in 2014 and 2015. 2014 Apr. 20 Purchased $36,500 of merchandise on credit from Locust, terms are 1/10, n/30. Tyrell uses the perpetual inventory system. May 19 Replaced the April 20 account payable to Locust with a 90-day, $35,000 note bearing 8% annual interest along with paying $1,500 in cash. July 8 Borrowed $51,000 cash from National Bank by signing a 120-day, 12% interest-bearing note with a face value of $51,000. __?__ Paid the amount due on the note to Locust at the maturity date. __?__ Paid the amount due on the note to National Bank at the maturity date. Nov. 28 Borrowed $27,000 cash from Fargo Bank by signing a 60-day, 6% interest-bearing note with a face value of $27,000. Dec. 31 Recorded an adjusting entry for accrued interest on the note to Fargo Bank. 2015 __?__ Paid the amount due on the note to Fargo Bank at the maturity…arrow_forward

- Tyrell Co. entered into the following transactions involving short-term liabilities in 2014 and 2015. 2014 Apr. 20 Purchased $36,500 of merchandise on credit from Locust, terms are 1/10, n/30. Tyrell uses the perpetual inventory system. May 19 Replaced the April 20 account payable to Locust with a 90-day, $35,000 note bearing 8% annual interest along with paying $1,500 in cash. July 8 Borrowed $51,000 cash from National Bank by signing a 120-day, 12% interest-bearing note with a face value of $51,000. __?__ Paid the amount due on the note to Locust at the maturity date. __?__ Paid the amount due on the note to National Bank at the maturity date. Nov. 28 Borrowed $27,000 cash from Fargo Bank by signing a 60-day, 6% interest-bearing note with a face value of $27,000. Dec. 31 Recorded an adjusting entry for accrued interest on the note to Fargo Bank. 2015 __?__ Paid the amount due on the note to Fargo Bank at the maturity…arrow_forwardThe current sections of Bridgeport Corp.'s balance sheets at December 31, 2016 and 2017, are presented here. Bridgeport Corp.'s net income for 2017 was $153,459. Depreciation expense was $27,081. 2017 2016 Current assets Cash $105,315 $ 99,297 Accounts receivable 80,240 89,267 Inventory 168,504 172,516 Prepaid expenses 27,081 22,066 Total current assets $381,140 $383,146 Current liabilities Accrued expenses payable $ 15,045 $ 5,015 Accounts payable 85,255 92,276 Total current liabilities $100,300 $ 97,291 ember 31, 2017, using Prepare the net cash provided (used) by operating activities section of the company's statement (15,000).) cash flows or the year ende indirect ethod. (Show am that decrease cash flow with either a - sign e.g. -15,000 or in parenthesis e.g. Bridgeport Corp. Partial Statement of Cash Flows $ Adjustments to reconcile net income to $ $1arrow_forwardTyrell Co. entered into the following transactions involving short-term liabilities in 2014 and 2015. 2014 Apr. 20 Purchased $36,500 of merchandise on credit from Locust, terms are 1/10, n/30. Tyrell uses the perpetual inventory system. May 19 Replaced the April 20 account payable to Locust with a 90-day, $35,000 note bearing 8% annual interest along with paying $1,500 in cash. July 8 Borrowed $51,000 cash from National Bank by signing a 120-day, 12% interest-bearing note with a face value of $51,000. _?_ Paid the amount due on the note to Locust at the maturity date. _?_ Paid the amount due on the note to National Bank at the maturity date. Nov. 28 Borrowed $27,000 cash from Fargo Bank by signing a 60-day, 6% interest-bearing note with a face value of $27,000. Dec. 31 Recorded an adjusting entry for accrued interest on the note to Fargo Bank. 2015 _? Paid the amount due on the note to Fargo Bank at the maturity date.…arrow_forward

- The following information is available for Bridgeport Corp. for three recent fiscal years. 2015 $325.447 1,285,838 965,338 2017 Inventory $554,103 Net sales - 1,965,543 Cost of goods sold 1.572,196 Calculate the inventory turnover, days in inventory, and gross profit rate for 2017 and 2016. (Round Inventory turnover to 1 decimal place, e.g. 5.2, days in inventory to O decimal places, eg. 125 and gross profit rate to 1 decimal place, e.g. 5.2%) Inventory Turnover Days in Inventory 2016 $572,288 1.739,520 1.307,512 Gross Profit Rate 2017 times days 2016 times daysarrow_forwardThe following information is taken Aiello Corporation's fiscal 2016 annual report. Selected Balance Sheet Data 2016 2015 Inventories........................ $221,418 $226,893 Accounts Receivable........... $121,333 $122,087 Assume that Aiello Corporation had $1,003,881 sales on credit during fiscal year 2016. What amount did the company collect from credit customers during the year? a. $1,003,881 b. $1,004,635 c. $1,003,127 d. $1,247,301arrow_forwardUsing these data from the comparative balance sheet of Sheridan Company, perform vertical analysis. (Round percentages to 1 decimal place, e.g. 12.5%.) Dec. 31, 2017Dec. 31, 2016AmountPercentageAmountPercentageAccounts receivable$ 540,000 Enter percentages % $ 363,000 Enter percentages %Inventory$ 783,000 Enter percentages % $ 642,000 Enter percentages %Total assets$3,120,000 Enter percentages % $2,704,000 Enter percentages %arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education